Sternal Closure Systems Market Share, Size, Trends, Industry Analysis Report, By Product (Closure Devices, Bone Cement), By Material (Titanium, PEEK, Stainless Steel), By Procedure (Median Sternotomy, Hemisternotomy, Bilateral Thoracosternotomy), By Region; Segment Forecast, 2021 - 2028

- Published Date:May-2021

- Pages: 126

- Format: PDF

- Report ID: PM1910

- Base Year: 2020

- Historical Data: 2016-2019

Report Outlook

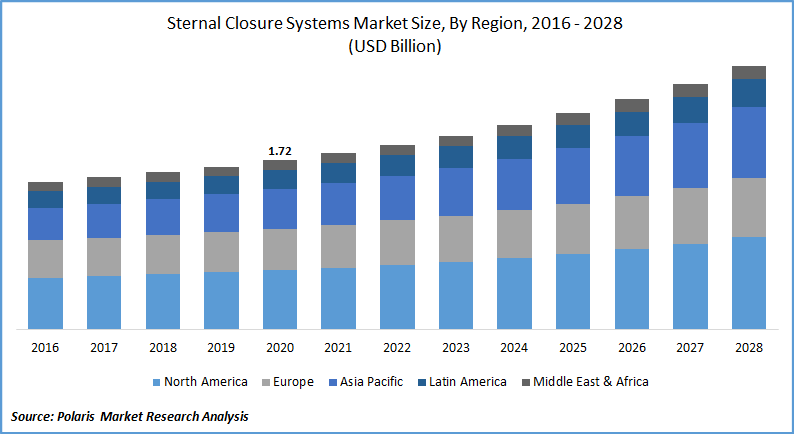

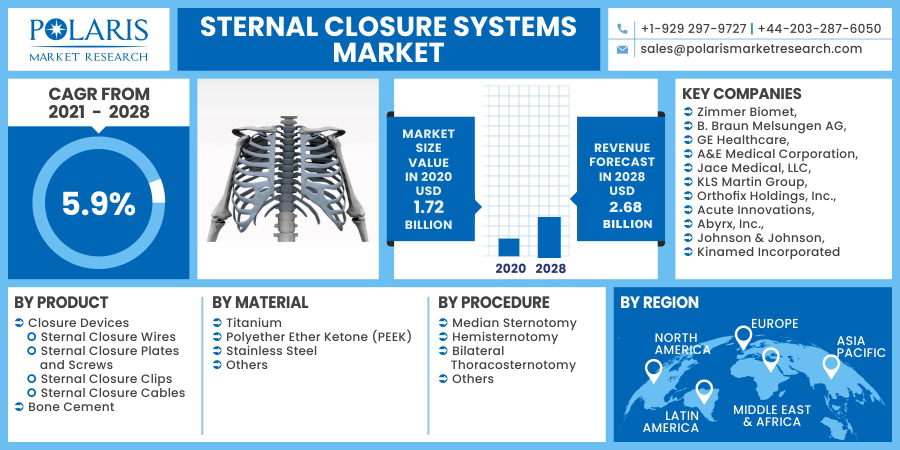

The global sternal closure systems market was valued at USD 1.72 billion in 2020 and is expected to grow at a CAGR of 5.9% during the forecast period. The key factors responsible for the market growth include the growing geriatric population performing open-heart surgery via median sternotomy and the rise in cardiac surgeries across the globe. Due to simple and fast access to heart valves and vessels, the median sternotomy is the most common method for cardiac operations. Before and after cardiac surgery, sternotomies, and sternal closure are performed.

Know more about this report: request for sample pages

Know more about this report: request for sample pages

Industry Dynamics

Growth Drivers

An increase in the number of surgeries performed around the world has fueled the demand for these systems, propelling the market. According to the OECD, surgeries in the United Kingdom totaled about 399,952 in 2012, increasing to 491,604, in 2016.

Furthermore, in the older population, lack of exercise and inadequate diet raises the risk of cardiovascular disease. Besides, the increasing geriatric population, which is more vulnerable to chronic CVDs, is contributing to a rise in the number of heart surgeries, which is driving up demand for sternal closure systems around the world.

In addition, due to the rise in non - communicable morbidity and mortality, and accidents, developed countries are concentrating on investing in healthcare infrastructure. This would boost the number of surgeries in emerging economies driving the sternal closure systems market.

China's per capita health spending in 2015 was USD 425.6, making for 5.3 percent of GDP, as per World Bank statistics. Moreover, according to China's Health 2030 Plan, health spending will reach 6.5% to 7% of the nation's total GDP, by 2020.

Unhealthy lifestyles, excessive smoking, and alcohol consumption, and a poor diet are all contributing to an increase in the prevalence of heart diseases around the world. This is leading to an increase in surgeries, which will undoubtedly boost the implementation of sternal closure systems shortly.

Know more about this report: request for sample pages

Sternal Closure Systems Market Report Scope

The market is primarily segmented based on product, material, procedure, and geographic region.

|

By Product |

By Material |

By Procedure |

By Region |

|

|

|

|

Know more about this report: request for sample pages

Insight by Product

Closure devices market segment dominated the market in 2020, accounting for the majority of the share. The dominant share of the market segment for sternal closure systems is attributed to factors such as product launches combined with increasing per capita expenditure in both developed and emerging economies.

In contrast to bone cement, these devices have shown benefits such as a reduction in postoperative complications and infections, as well as a quicker recovery period. Furthermore, market players for sternal closure systems are increasing their efforts to implement new techniques and product lines, which is expected to fuel the segment's market growth sternal closure systems over the coming years.

Insight by Material

In 2020, the titanium material dominated the demand for sternal closure systems, accounting for the majority of sales. Titanium's superiority can be attributed to its corrosion resistance, ability to efficiently enter human bones, and biocompatibility. Furthermore, titanium's non-ferromagnetic property, which enables patients with titanium implants to be examined safely under an MRI scan, is boosting the material's market penetration.

Besides that, the high effectiveness, non-toxic quality, and reliability of titanium materials, and enhanced economic viability and profitability for innovative titanium clips and plates in both emerging and developed countries, are expected to boost the adoption of titanium-based sternal closure systems.

Insight by Procedure

In 2020, the median sternotomies procedure accounted for the majority of sales. The operation allows direct access to the heart, lungs, and associated tissues during coronary artery bypass surgery and heart valve replacement surgery.

Median sternotomies are commonly performed osteotomies around the world. In addition to reducing post-operative infections and complications, median sternotomies are becoming increasingly popular around the world.

Geographic Overview

With a large group of patients and well-established medical insurance programs, North America accounted for the largest significant market share. Additionally, the market for sternal closure systems is being fueled by an increase in joint efforts made by several key players to enhance their product offerings and maintain high-quality standards.

The Asia Pacific sternal closure systems market, on the other hand, is projected to grow at a rapid rate in the coming years, as key players broaden their geographical presence in the world and concentrate on commercializing their products at a low price. Furthermore, a rise in healthcare spending and infrastructure development, as well as increased awareness of the cardiovascular disease, are anticipated to boost the market demand for sternal closure systems in the area.

Competitive Insight

Key market players in the sternal closure systems industry are concentrating their energies on strategic acquisitions to boost their research and development capabilities, which will help them provide creative solutions to users and gain a competitive edge.

Market participants such as Zimmer Biomet, B. Braun Melsungen AG, GE Healthcare, A&E Medical Corporation, Jace Medical, LLC, KLS Martin Group, Orthofix Holdings, Inc., Acute Innovations, Abyrx, Inc., Johnson & Johnson, and Kinamed Incorporated are some of the companies operating in the market for sternal closure systems.

© 2025 Polaris Market Research and Consulting. All rights reserved