Sleep Disorders Market Size, Share, Trends, Industry Analysis Report: By Disorder (Restless Legs Syndrome, Narcolepsy, Insomnia, and Sleep Apnea), Product, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Jan-2025

- Pages: 118

- Format: PDF

- Report ID: PM1573

- Base Year: 2024

- Historical Data: 2020-2023

Sleep Disorders Market Overview

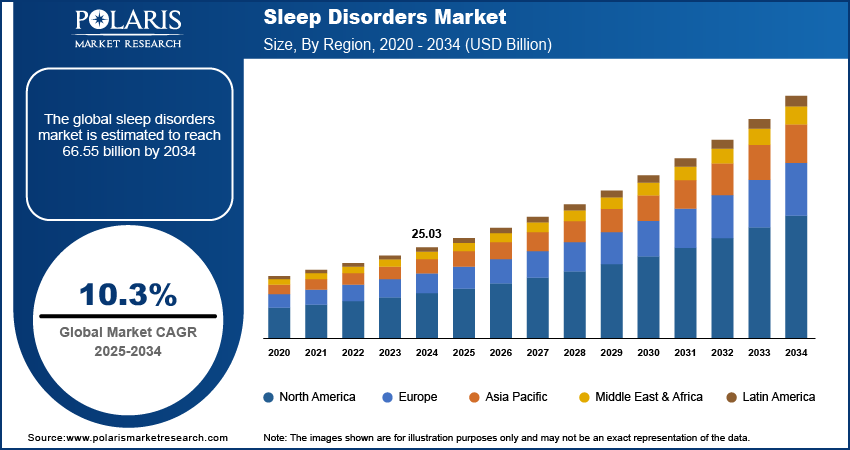

The sleep disorders market size was valued at USD 25.03 billion in 2024. The market is projected to grow from USD 27.54 billion in 2025 to USD 66.55 billion by 2034, exhibiting a CAGR of 10.3% during 2025–2034.

The sleep disorders market focuses on the diagnosis, treatment, and management of various sleep-related conditions such as insomnia, sleep apnea, narcolepsy, and restless leg syndrome. The increasing prevalence of sleep disorders, rising awareness about the importance of sleep for overall health, and increasing technological advancements in diagnostic tools and treatment options drive the market growth. Additionally, the growing adoption of telemedicine and wearable devices for sleep monitoring, along with an aging global population, contributes to market growth. Sleep disorders market trends include the development of non-pharmacological treatments, personalized therapies, and the integration of artificial intelligence (AI) in sleep disorder management.

To Understand More About this Research: Request a Free Sample Report

Sleep Disorders Market Dynamics

Increased Adoption of Telemedicine for Sleep Disorder Diagnosis and Treatment

Telemedicine has become a significant trend in the sleep disorders market, driven by the need for remote healthcare solutions and increasing demand for accessible treatment options. The COVID-19 pandemic accelerated the adoption of virtual healthcare services, including for sleep disorders, as patients sought convenience and safety. This trend continues as healthcare providers leverage telemedicine platforms to offer consultations, remote monitoring, and follow-up care for conditions such as insomnia and sleep apnea. The American Academy of Sleep Medicine (AASM) reported that telemedicine consultations for sleep-related issues grew by over 50% during the pandemic. This trend reduces barriers to care and allows for greater patient access to specialized sleep experts.

Advancements in Wearable Sleep Monitoring Devices

The growing popularity of wearable technology is transforming sleep disorder management. Devices such as smartwatches and dedicated sleep trackers are increasingly being used to monitor sleep patterns, detect sleep apnea, and provide insights into overall sleep quality. These devices use sensors and algorithms to collect data on sleep stages, heart rate, and movement, offering users a more personalized understanding of their sleep health. According to a report by the National Sleep Foundation, nearly 30% of adults in the US use some form of wearable or mobile technology to track their sleep. The continuous improvement in wearable device accuracy and the integration of AI for better data interpretation are expected to enhance early detection and treatment outcomes. Thus, the rising technological advancements in wearable sleep monitoring devices are expected to boost the sleep disorders market development during the forecast period.

Growth of Non-Pharmacological Treatment Options

There is a growing shift toward non-pharmacological treatments for sleep disorders, particularly cognitive behavioral therapy for insomnia (CBT-I), which is considered an effective and long-term solution for sleep issues. Unlike medication, CBT-I focuses on changing behaviors and thought patterns that contribute to insomnia. The American College of Physicians (ACP) recommends CBT-I as the first-line treatment for chronic insomnia. Additionally, other alternative treatments, including mindfulness practices, relaxation techniques, and biofeedback, are gaining traction due to their minimal side effects and efficacy. According to a 2020 study in JAMA Internal Medicine, CBT-I was found to significantly improve sleep outcomes in over 70% of individuals with chronic insomnia, further fueling the demand for non-drug-based solutions. Thus, the increasing preference for non-pharmacological treatments drives the sleep disorders market demand.

Sleep Disorders Market Segment Insights

Sleep Disorders Market Outlook – Disorder-Based Insights

Based on disorders, the sleep disorders market is segmented into insomnia, sleep apnea, restless legs syndrome (RLS), and narcolepsy. The insomnia segment holds the largest market share due to its high prevalence across the global population. It is estimated that ∼30% of adults experience some form of insomnia, contributing significantly to the demand for pharmacological and non-pharmacological treatment options. This segment benefits from widespread recognition of the condition and the increasing awareness of its impact on overall health. Moreover, insomnia's association with comorbidities such as anxiety and depression further drives the demand for effective management solutions.

The sleep apnea segment, particularly obstructive sleep apnea (OSA), is also witnessing significant growth due to the rising incidence of risk factors such as obesity and the aging population. The increasing availability of diagnostic tools, such as home sleep testing devices, and the growing adoption of continuous positive airway pressure (CPAP) therapy contribute to the expansion of this segment. Sleep apnea is expected to register the highest growth, driven by technological advancements in treatment and the increasing focus on early detection. While narcolepsy and RLS remain important segments, their market share and growth rates are comparatively lower due to less widespread awareness and the more complex nature of diagnosis and treatment.

Sleep Disorders Market Assessment – Product-Based Insights

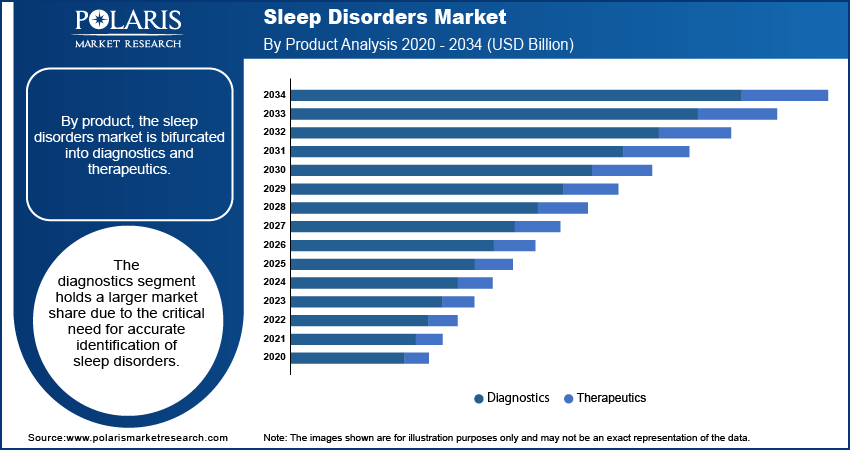

By product, the sleep disorders market is bifurcated into diagnostics and therapeutics. The diagnostics segment holds a larger market share due to the critical need for accurate identification of sleep disorders. Increasing awareness about the importance of sleep health and the availability of advanced diagnostic tools, such as polysomnography, actigraphy, and home sleep apnea tests (HSAT), are major factors contributing to the growth of this segment. The rising adoption of wearable devices for continuous monitoring of sleep patterns has also driven the diagnostic segment. These advancements in diagnostic technologies enable early detection and improved patient outcomes, further driving demand for diagnostic solutions in the sleep disorders market.

The therapeutics segment is expected to register a higher growth rate during the forecast period. The segment focuses on pharmaceutical treatments, devices, and non-pharmacological therapies. The sleep disorders market demand for this segment is attributed to the growing prevalence of sleep disorders and the continuous development of innovative treatment options. The increasing use of CPAP therapy for sleep apnea, the growth of cognitive behavioral therapy for insomnia (CBT-I), and the development of new drug formulations are contributing to the expanding therapeutics segment. Moreover, the shift toward noninvasive treatments and the integration of AI in therapy management are likely to accelerate the segment growth. With a focus on providing more personalized and effective treatment options, the therapeutics segment is experiencing rapid innovation and gaining significant market momentum.

Sleep Disorders Market Evaluation – End User-Based Insights

In terms of end users, the sleep disorders market is segmented into hospitals & sleep laboratories and home care settings. The hospitals & sleep laboratories segment holds a larger market share due to their established infrastructure for diagnosing and treating sleep disorders. These facilities are equipped with advanced diagnostic tools such as polysomnography and offer specialized treatments such as CPAP therapy for sleep apnea, contributing to their dominance in the market. The extensive expertise and resources available in these settings attract patients who require in-depth evaluations and comprehensive treatment plans. Additionally, hospitals and sleep laboratories benefit from the growing demand for sleep studies, which are integral for the diagnosis of complex disorders such as narcolepsy and sleep apnea.

The home care settings segment is registering a higher growth rate, primarily due to the increasing preference for at-home diagnostics and treatments. The rise in the adoption of wearable sleep monitors, portable diagnostic devices, and telemedicine platforms for virtual consultations is driving the expansion of home care settings. This segment is further fueled by the growing focus on patient convenience, cost-effectiveness, and the shift toward remote healthcare solutions. The development of easy-to-use devices, such as CPAP machines and auto-titrating devices, for managing conditions such as sleep apnea at home has made home care a more viable and popular option for many patients. With continuous advancements in technology and the increasing adoption of telemedicine, the home care settings segment is poised for significant growth in the coming years.

Sleep Disorders Market Regional Insights

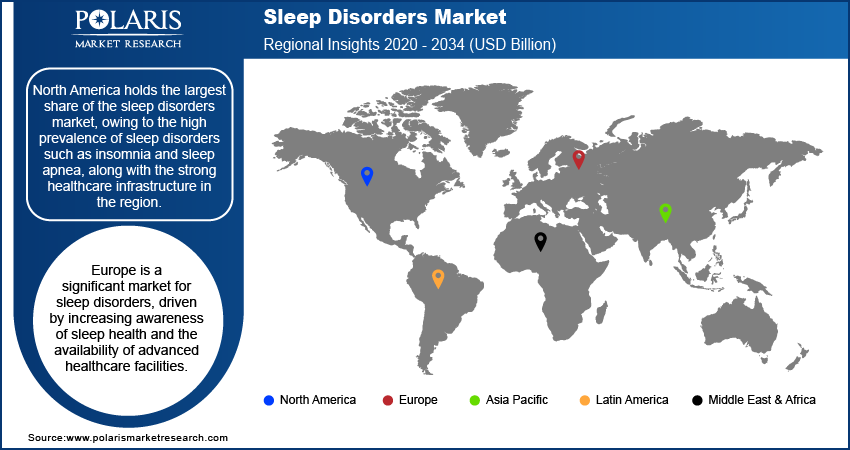

By region, the study provides sleep disorders market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest market share, primarily driven by the high prevalence of sleep disorders such as insomnia and sleep apnea, along with the strong healthcare infrastructure in the region. The US, in particular, has a well-established healthcare system that supports the widespread adoption of advanced diagnostic and therapeutic technologies for sleep disorders. Additionally, the growing awareness about the impact of sleep on overall health, along with increasing healthcare spending and the availability of innovative treatment options, contributes to the region's dominance. The North America market growth is also driven by a higher rate of sleep disorder diagnosis and treatment.

Europe is a significant market for sleep disorders, driven by increasing awareness of sleep health and the availability of advanced healthcare facilities. The region's high healthcare standards, coupled with government initiatives aimed at improving sleep disorder diagnosis and treatment, support the sleep disorders market expansion. Countries such as Germany, the UK, and France are leading the market, with high demand for sleep apnea treatments and insomnia management solutions. The growing adoption of diagnostic tools such as home sleep testing devices and wearable technology, along with a rising preference for non-pharmacological therapies such as cognitive behavioral therapy for insomnia (CBT-I), is further enhancing the market outlook. Europe's aging population, coupled with rising rates of conditions such as obesity, which contribute to sleep disorders, is also a key driver.

The Asia Pacific sleep disorders market is experiencing rapid growth, primarily driven by improving healthcare access, increasing awareness about sleep health, and a rising prevalence of sleep disorders. Countries such as China, Japan, and India are witnessing a surge in sleep disorder diagnoses due to lifestyle changes, growing urbanization, and the aging population. While the market is still developing in some areas, the increasing adoption of diagnostic devices and treatments like CPAP machines for sleep apnea is notable. Moreover, the shift toward telemedicine and wearable sleep monitoring devices is expanding access to care, particularly in rural and underserved areas. The region's growing middle-class population and healthcare investments are expected to drive market expansion in the coming years.

Sleep Disorders Market – Key Players and Competitive Insights

Key players in the sleep disorders market include ResMed, Philips Healthcare, Medtronic, Fisher & Paykel Healthcare, Somnomed, Sleep Number Corporation, Invacare Corporation, Nihon Kohden Corporation, CareFusion, and Becton Dickinson. The companies provide a range of solutions for diagnosing and treating sleep disorders, such as sleep apnea, insomnia, and restless legs syndrome. Other significant players include Circadia, Inogen, Itamar Medical, Chemspec International, and ProTech Sleep Solutions. A few of these companies, such as ResMed and Philips Healthcare, specialize in sleep apnea treatment with devices such as CPAP machines, whereas others focus on diagnostic tools and home sleep testing, such as Medtronic and Nihon Kohden. Invacare Corporation and Sleep Number offer a broader range of therapeutic products, including sleep surfaces and other home care solutions for patients affected by sleep disorders.

The competitive landscape of the sleep disorders market is characterized by a mix of established players and emerging companies focused on innovations in diagnostics and treatments. Many companies are investing in research and development to improve existing devices and create more advanced, user-friendly solutions. Technological advancements in wearable devices and telemedicine are opening new opportunities, with players such as Somnomed and Circadia leveraging these trends. At the same time, established companies such as ResMed and Medtronic continue to dominate the therapeutic segment by providing integrated solutions for sleep apnea management. Market participants are also focusing on expanding their presence in emerging markets such as Asia Pacific and Latin America, where healthcare access and awareness are rapidly improving.

While competition is intense, companies differentiate themselves through product innovation, customer service, and partnerships with healthcare providers. For example, Philips Healthcare emphasizes the integration of AI and cloud-based platforms in sleep disorder management, while ResMed has expanded its offerings to include home sleep testing kits in addition to its therapeutic devices. Moreover, companies are increasingly collaborating with healthcare institutions and investing in telemedicine services to provide remote monitoring and treatment options, responding to the growing demand for convenient care. With the expected market expansion, companies that can effectively integrate technology into their offerings and cater to a broad range of patient needs are likely to gain a competitive advantage.

ResMed specializes in providing products for the treatment of sleep apnea, chronic obstructive pulmonary disease (COPD), and other respiratory conditions. It offers a range of devices, including CPAP machines and associated accessories, as well as software solutions for monitoring and managing sleep disorders. The company focuses on improving the quality of life for individuals affected by sleep disorders through in-hospital and home-care devices.

Philips Healthcare, a division of Royal Philips, is involved in providing a wide variety of health-related products, including those for sleep disorder management. The company manufactures and sells devices such as CPAP machines, sleep monitoring systems, and home diagnostic tools. Philips Healthcare is also known for its efforts in integrating advanced technologies, such as AI and cloud computing, into its sleep disorder solutions.

List of Key Companies in Sleep Disorders Market

- ResMed

- Philips Healthcare

- Medtronic

- Fisher & Paykel Healthcare

- Somnomed

- Sleep Number Corporation

- Invacare Corporation

- Nihon Kohden Corporation

- CareFusion

- Becton Dickinson

- Circadia

- Inogen

- Itamar Medical

- ProTech Sleep Solutions

Sleep Disorders Industry Developments

- In November 2024, ResMed announced the acquisition of InHealthcare specializing in AI-based diagnostic tools, aiming to enhance its offerings in sleep apnea diagnostics and treatment.

- In October 2024, Philips launched a new series of smart sleep devices designed to provide personalized therapy and real-time monitoring aimed at improving sleep quality for users at home.

Sleep Disorders Market Segmentation

By Disorder Outlook

- Restless Legs Syndrome

- Narcolepsy

- Insomnia

- Sleep Apnea

By Product Outlook

- Diagnostics

- Therapeutics

By End User Outlook

- Hospitals & Sleep Laboratories

- Home Care Settings

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Sleep Disorders Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 25.03 billion |

|

Market Size Value in 2025 |

USD 27.54 billion |

|

Revenue Forecast by 2034 |

USD 66.55 billion |

|

CAGR |

10.3% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The sleep disorders market size was valued at USD 25.03 billion in 2024 and is projected to grow to USD 66.55 billion by 2034.

The market is projected to register a CAGR of 10.3% during 2025–2034.

North America accounted for the largest share of the market in 2024.

Key players in the sleep disorders market are ResMed, Philips Healthcare, Medtronic, Fisher & Paykel Healthcare, Somnomed, Sleep Number Corporation, Invacare Corporation, Nihon Kohden Corporation, CareFusion, and Becton Dickinson.

The diagnostics segment accounted for a larger share of the market in 2024.

The insomnia segment accounted for the largest share of the market in 2024.

Sleep disorders are a group of conditions that affect the ability to sleep well on a regular basis. These disorders can disrupt the quality, timing, and duration of sleep, leading to daytime fatigue and other health problems. A few common sleep disorders are insomnia (difficulty falling or staying asleep), sleep apnea (pauses in breathing during sleep), narcolepsy (excessive daytime sleepiness), and restless legs syndrome (an uncontrollable urge to move the legs while resting). Sleep disorders can result from various factors such as stress, medical conditions, lifestyle habits, or genetics, and they can significantly impact an individual's overall health and well-being. Proper diagnosis and treatment are essential for managing these conditions effectively.

A few key trends in the market are described below: Adoption of Telemedicine: Increased use of virtual consultations and remote monitoring for diagnosing and treating sleep disorders, especially during and after the COVID-19 pandemic. Rising Use of Wearable Sleep Monitoring Devices: Growing popularity of smartwatches and other wearable devices to track sleep patterns and detect sleep apnea or other disorders. Increasing Preference for Non-Pharmacological Treatments: Rising demand for non-drug-based therapies, such as cognitive behavioral therapy for insomnia (CBT-I) and relaxation techniques. Technological Advancements: Integration of artificial intelligence (AI) and machine learning (ML) in diagnostic tools and therapy devices to improve personalized treatment.

A new company entering the sleep disorders market must focus on innovative and personalized solutions to differentiate itself from competitors. Investing in advanced wearable devices that offer real-time sleep monitoring, paired with AI-driven insights for personalized treatment, could be a key area. Additionally, expanding into telemedicine for remote consultations and integrating telehealth platforms for continuous patient monitoring would address the growing demand for convenient, at-home care. Offering non-pharmacological treatments such as cognitive behavioral therapy for insomnia (CBT-I) could also provide a competitive edge. Focusing on emerging markets, where healthcare access and awareness are increasing, would further create growth opportunities.

Companies manufacturing, distributing, or purchasing sleep disorders diagnostics, therapeutics, and related products, and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved