Silicon Carbide Market Size, Share, Trends, Industry Analysis Report: By Device (SiC Discrete Device and SiC Module), Wafer Size, Application, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025 - 2034

- Published Date:Nov-2024

- Pages: 120

- Format: PDF

- Report ID: PM5248

- Base Year: 2024

- Historical Data: 2020-2023

Silicon Carbide Market Overview

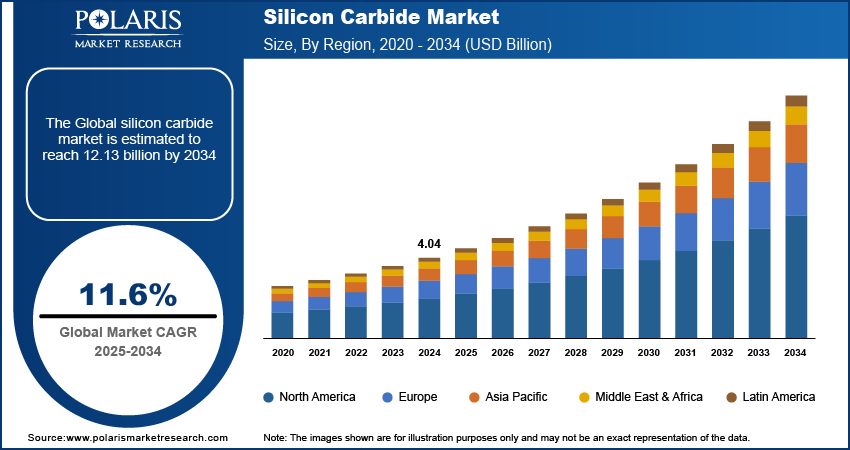

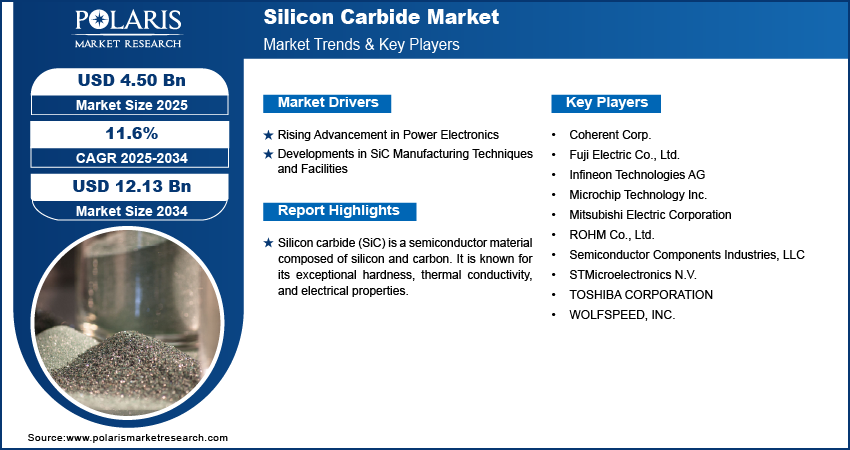

Global silicon carbide market size was valued at USD 4.04 billion in 2024. The market is projected to grow from USD 4.50 billion in 2025 to USD 12.13 billion by 2034, exhibiting a CAGR of 11.6% during the forecast period. Silicon carbide (SiC) is a semiconductor material composed of silicon and carbon. It is known for its exceptional hardness, thermal conductivity, and electrical properties. The silicon carbide market refers to the industry and commercial sector that involves the production, distribution, and consumption of silicon carbide materials and products.

The surge in electric vehicle (EV) adoption is a major driver for the silicon carbide market. According to the International Energy Agency, nearly 14 billion electric cars were registered globally in 2023, marking a 35% increase from 2022 and bringing the total number on the road to 40 billion. Of these new registrations, 95% occurred in China, Europe, and the US.

SiC's superior efficiency and high-temperature tolerance make it an essential material for power electronics in electric vehicles, including inverters and converters. Its ability to handle high voltages and temperatures enhances the performance and range of EVs while also improving energy efficiency.

SiC is also vital for fast-charging systems, which are crucial for reducing charging times and enhancing the overall EV experience. Also, the automotive industry continues to shift towards electric mobility, and the demand for SiC components is expected to grow significantly, driven by the need for advanced power electronics that can deliver higher performance and efficiency.

To Understand More About this Research: Request a Free Sample Report

Beyond electric vehicles, SiC is increasingly being used in traditional automotive systems, such as advanced driver-assistance systems (ADAS) and other high-performance electronics. Its ability to operate efficiently under high temperatures and voltages enhances the reliability and performance of these critical automotive technologies. It supports advancements in vehicle safety and functionality which drives the silicon carbide market growth.

Silicon Carbide Market Growth Factors and Trends Analysis

Rising Advancement in Power Electronics

Advancements in power electronics are significantly boosting the demand for silicon carbide due to its exceptional performance in high-power and high-frequency applications. SiCs are a critical component in modern power systems, enhancing energy conversion and reducing losses in various electronic devices. For instance, In July 2024, onsemi introduced EliteSiC M3e MOSFETs to enhance energy efficiency by reducing turn-off losses by up to 50%, driving innovations in electrification and supporting global climate goals.

This efficiency improves overall system performance and also contributes to the miniaturization and reliability of power electronics. Further, industries increasingly seek solutions that offer better energy management and operational reliability. SiC's role in advancing power electronics continues to grow, driving its adoption across diverse applications and sectors.

Developments in SiC Manufacturing Techniques and Facilities

Innovations in silicon carbide manufacturing, including advancements in crystal growth techniques and wafer fabrication, are markedly improving the quality and performance of SiC materials. These enhancements are leading to higher efficiency and reliability in SiC devices while also significantly reducing production costs.

Key market players are investing in the development of new manufacturing facilities to scale up production and meet the growing demand for SiC technology. For instance, in May 2024, STMicroelectronics built the world's first fully integrated silicon carbide facility in Catania, Italy, with a €5 billion investment, including €2 billion from the State of Italy, to advance high-volume SiC production and support the shift to electrification.

Similarly, in April 2024, Wolfspeed announced its $5 billion silicon carbide facility, along with global investments by major players such as Mitsubishi Electric; Mersen; SICC; TANKEBLUE; Ascen Power; and San’an, which highlights the booming demand and rapid expansion in the silicon carbide market.

These expanded capabilities not only boost the supply chain but also accelerate the commercialization of advanced SiC solutions, further driving innovation and adoption across various high-performance applications.

Silicon Carbide Market Segment Analysis

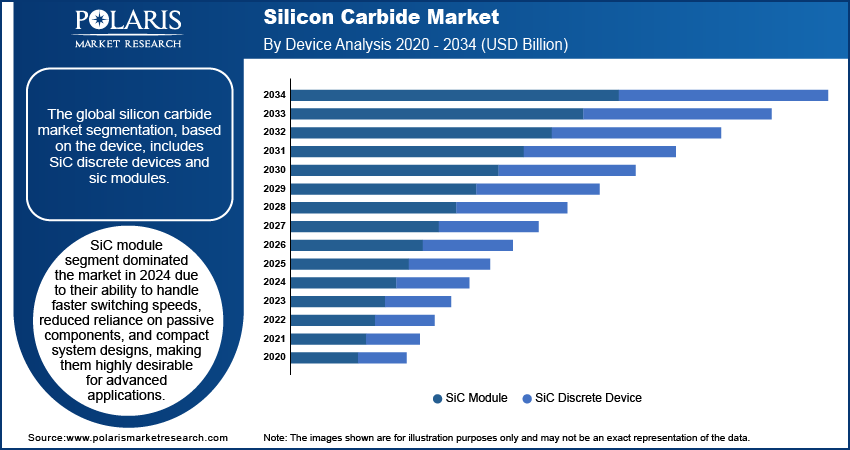

Silicon Carbide Market Assessment by Device

The global silicon carbide market segmentation, based on the device, includes SiC discrete devices and sic modules. SiC module segment dominated the market in 2024 due to their superior performance characteristics. Their ability to handle faster switching speeds, reduced reliance on passive components, and compact system designs make them highly desirable for advanced applications. Additionally, SiC modules excel in high-frequency operations, offer high blocking voltage, and can tolerate elevated junction temperatures, which further enhances their appeal.

These attributes contribute to a significant increase in power density and compactness, driving the demand for SiC modules across various industries. For instance, in January 2024, Mitsubishi Electric introduced six J3-Series SiC and Si power modules for electric vehicles, with sample shipment starting from March 25, 2024, showcasing at NEPCON JAPAN 2024 and other global exhibitions.

As technology advances and the demand for efficient, high-performance components grows, the SiC module's advanced features position it as the leading choice in the silicon carbide market in the foreseeable future.

Silicon Carbide Market Evaluation by Application

The global silicon carbide market segmentation, based on application, includes automotive, energy & power, industrial, transportation, telecommunication, and others. The automotive segment held a significant share of the silicon carbide (SiC) market due to the increasing demand for high-performance power and opto-semiconductor devices. The need for energy-efficient and high-performance electronic systems in the automotive industry drives this demand. SiC-based devices offer superior performance, including higher efficiency, faster switching speeds, and better thermal conductivity, compared to traditional silicon-based components.

This is particularly driven by the growing adoption of SiC-based power electronics in EVs for improved energy efficiency, faster charging, and increased range. Additionally, the development of advanced driver assistance systems (ADAS) and the electrification of vehicles further contribute to the growth of the SiC market in the automotive sector.

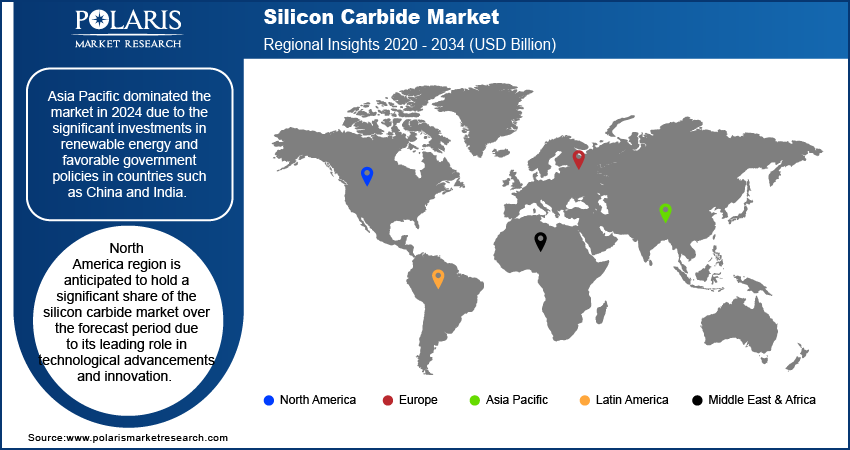

Silicon Carbide Market Analysis by Regional Insights

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominated the market in 2024 due to the significant investments in renewable energy and favorable government policies in countries such as China and India. For instance, in June 2024, The Asian Development Bank (ADB) invested $50 billion in the Actis Asia Climate Transition Fund to support renewable energy, sustainable transportation, and climate-resilient infrastructure in Asia and the Pacific.

Technological advancements in SiC production have also contributed to lower costs and increased availability, reinforcing the region's dominance in the global market.

North America region is anticipated to hold a significant share of the silicon carbide market over the forecast period due to its leading role in technological advancements and innovation. The region's strong automotive sector, particularly with the rise of EVs, has driven up the demand for SiC due to its efficiency and performance benefits in power electronics.

Supportive government policies promoting green technologies and substantial investments in research and development have bolstered the adoption of SiC in North America. The presence of major semiconductor companies and research institutions has also facilitated technological breakthroughs and cost reductions, further fueling the growth of the silicon carbide market in the region.

Silicon Carbide Key Market Players & Competitive Analysis Report

Major market players are investing heavily in research and development in order to expand their product lines, which will help the silicon carbide market grow even more. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, the silicon carbide industry must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the global silicon carbide market to benefit clients and increase the market sector. In recent years, the market has offered some technological advancements. Major players in the silicon carbide market include Coherent Corp.; Fuji Electric Co., Ltd.; Infineon Technologies AG; Microchip Technology Inc.; Mitsubishi Electric Corporation; ROHM Co., Ltd.; Semiconductor Components Industries, LLC; STMicroelectronics N.V.; TOSHIBA CORPORATION; and WOLFSPEED, INC.

Infineon Technologies AG specializes in semiconductor solutions for power systems and the Internet of Things (IoT). The company is advancing decarbonization and digitalization through its products and solutions. The company has 58,600 employees worldwide, and it achieved a revenue of around €16.3 billion for the fiscal year ending September 2023. In March 2024, Infineon Technologies AG unveiled its next-generation CoolSiC MOSFET G2, enhancing energy efficiency and decarbonization in power systems with up to 20% improved performance over previous SiC MOSFETs.

Mitsubishi Electric Corp develops, manufactures, and markets a wide range of electrical and electronic products, including air conditioning systems, factory automation, automotive equipment, and semiconductors. Serving various sectors such as residential, commercial, and industrial, the company also provides maintenance, IT infrastructure, and network services. Headquartered in Tokyo, Japan, Mitsubishi Electric operates globally across the Americas, Asia Pacific, Europe, the Middle East, and Africa. In March 2023, Mitsubishi Electric invested around 260 billion yen to build a new wafer plant and expand SiC power semiconductor production to meet growing demand and support energy efficiency and decarbonization.

Key Companies in Silicon Carbide Market

- Coherent Corp.

- Fuji Electric Co., Ltd.

- Infineon Technologies AG

- Microchip Technology Inc.

- Mitsubishi Electric Corporation

- ROHM Co., Ltd.

- Semiconductor Components Industries, LLC

- STMicroelectronics N.V.

- TOSHIBA CORPORATION

- WOLFSPEED, INC.

Silicon Carbide Market Developments

June 2024: ROHM introduced the EcoSiC brand to enhance the performance and sustainability of its silicon carbide products, aiming to improve efficiency, support eco-friendly technologies, and solidify its leadership in SiC innovation.

December 2023: Coherent Corp. secured a $1 billion investment from DENSO and Mitsubishi Electric, each acquiring a 12.5% stake in Coherent's silicon carbide semiconductor business to support growth and enhance supply for SiC substrates and wafers.

November 2023: Mitsubishi Electric and Nexperia partnered to develop silicon carbide (SiC) power semiconductors, combining Mitsubishi's SiC MOSFET technologies with Nexperia's expertise in discrete devices to advance energy efficiency and support decarbonization.

Silicon Carbide Market Segmentation

By Device Outlook (Volume - Kilotons, Revenue - USD Billion, 2020 - 2034)

- SiC Discrete Device

- SiC MOSFETs

- SiC Diodes

- SiC Module

By Wafer Size Outlook (Volume - Kilotons, Revenue - USD Billion, 2020 - 2034)

- Up to 150 mm

- >150 mm

By Application Outlook (Volume - Kilotons, Revenue - USD Billion, 2020 - 2034)

- Automotive

- Energy & Power

- Industrial

- Transportation

- Telecommunication

- Others

By Regional Outlook (Volume - Kilotons, Revenue - USD Billion, 2020 - 2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Silicon Carbide Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 4.04 billion |

|

Market Size Value in 2025 |

USD 4.50 billion |

|

Revenue Forecast in 2034 |

USD 12.13 billion |

|

CAGR |

11.6% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020– 2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Volume in KiloTons, Revenue in USD billion, and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global silicon carbide market size was valued at USD 4.04 billion in 2024 and is anticipated to reach USD 12.13 billion in 2034.

The global market registers a CAGR of 11.6% during the forecast period, 2025-2034.

Asia Pacific had the largest share of the global market.

The key players in the market are Coherent Corp.; Fuji Electric Co., Ltd.; Infineon Technologies AG; Microchip Technology Inc.; Mitsubishi Electric Corporation; ROHM Co., Ltd.; Semiconductor Components Industries, LLC; STMicroelectronics N.V.; TOSHIBA CORPORATION; and WOLFSPEED, INC.

The SiC module category dominated the market in 2024.

The automotive had the largest share of the global market.

© 2025 Polaris Market Research and Consulting. All rights reserved