Semiconductor Manufacturing Equipment Market Share, Size, Trends, Industry Analysis Report, By Product (Memory, MPU, Foundry, Logic, Discrete, Others); By Front-End Equipment; By Fab Facility Equipment; By Back-End Equipment; By Dimension; By Supply Chain Process; By Region; Segment Forecast, 2024- 2032

- Published Date:Mar-2024

- Pages: 117

- Format: PDF

- Report ID: PM4746

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

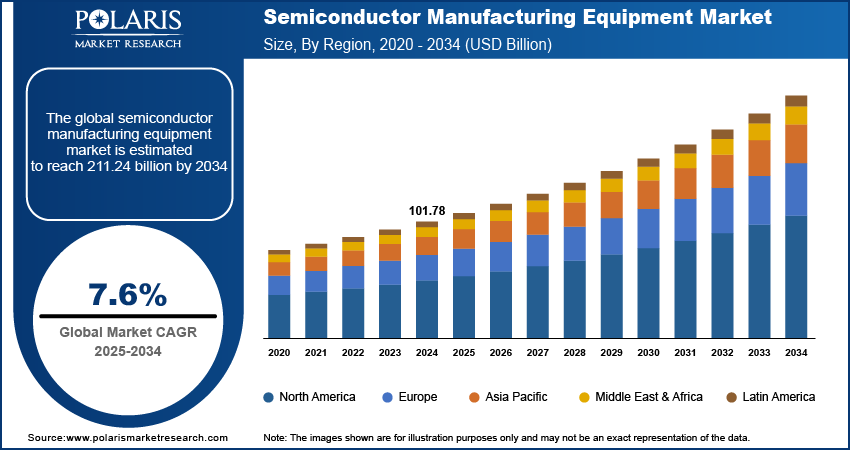

Global semiconductor manufacturing equipment Market size was valued at USD 90.62 billion in 2023. The market is anticipated to grow from USD 100.51 billion in 2024 to USD 233.31 billion by 2032, exhibiting a CAGR of 11.1% during the forecast period

Industry Trend

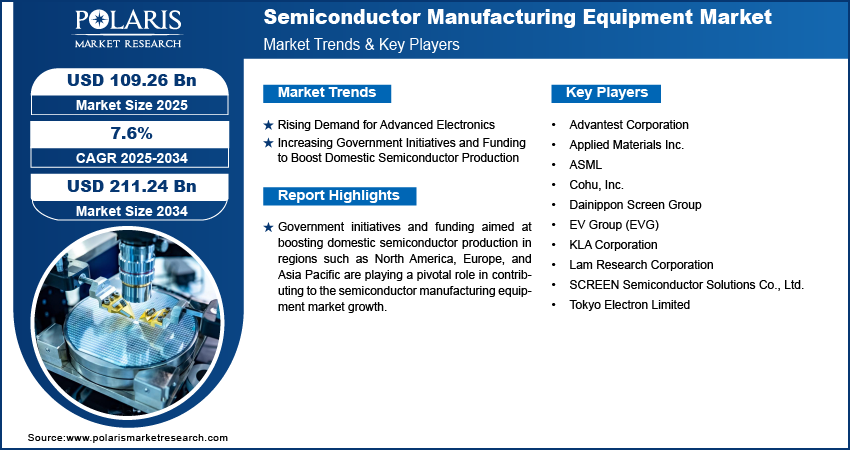

The surge in consumer electronic product demand can be attributed to rising disposable incomes and a growing appetite for cutting-edge technology. This trend extends to workplaces, daily life, and entertainment, fueling a greater need for semiconductors and driving market expansion. Semiconductor manufacturing equipment is poised for growth, buoyed by advancements in cloud technology, the emergence of 5G networks, and the demand for connected vehicles. Consumers are willing to invest more in high-tech gadgets to enhance their lifestyles, fostering further growth in this sector.

Manufacturers of semiconductor manufacturing equipment are diversifying their business models, offering usage-based, subscription, and outcome-based options. These models broaden the customer base, making advanced equipment accessible to medium-scale organizations through rental services. The demand for semiconductor solutions continues to climb across various industries, propelled by the proliferation of smartphones, tablets, smart TVs, and other consumer devices. Consumers seek improved performance, longer battery life, and enhanced features, all requiring semiconductor innovation.

To Understand More About this Research: Request a Free Sample Report

Major players within the semiconductor manufacturing equipment sector frequently forge strategic partnerships with complementary entities to capitalize on mutual strengths. These alliances may encompass technology exchange, collaborative product development, or joint marketing endeavors aimed at broadening market penetration and hastening innovation. Collaboration between equipment manufacturers and semiconductor firms facilitates meticulous synchronization of technology roadmaps, paving the way for customized solutions tailored to meet precise manufacturing needs. Such partnerships frequently yield the co-innovation of cutting-edge equipment, finely tuned for the latest semiconductor fabrication methodologies.

For instance, In January 2023, Shin Puu Technology Co., Ltd., a prominent supplier of printed circuit boards (PCBs) crucial for electronic devices was acquired by Advantest Corporation. Operating from Taiwan, the company specializes in the manufacturing and assembly of these essential components.

Industries are embracing automation and robotics for increased efficiency, relying on specialized semiconductors for process control, equipment monitoring, and safety. These factors, alongside the synergy between 5G and IoT technologies, are driving the demand for semiconductor manufacturing equipment to meet the evolving digital landscape's demands.

Key Takeaway

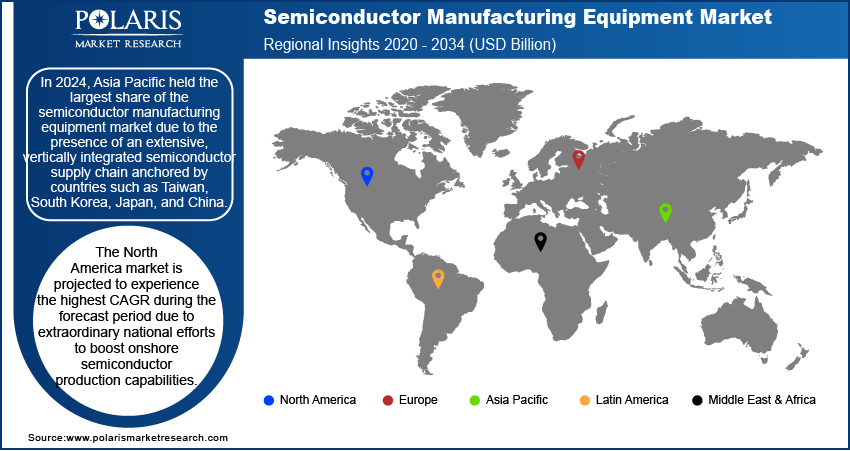

- Asia Pacific dominated the largest market and contributed to more than 38% of share in 2023.

- North America expected to witness the fastest growing CAGR during the forecast period.

- By front-end equipment category, lithography segment accounted for the largest market share in 2023.

- By dimension category, the 3D ICs segment expected to witness the fastest growing CAGR during the forecast period.

What Are the Market Drivers Driving the Demand for the Semiconductor Manufacturing Equipment Market?

Growing Technological Advancements

As technology evolves, the demand for more complex and advanced semiconductor designs rises. These advancements enable the development of smaller, faster, and more powerful chips with enhanced functionalities. Semiconductor manufacturing equipment must keep pace with these advancements to produce chips that meet the requirements of emerging technologies.

Continuous technological progress leads to the miniaturization of semiconductor components and the migration to advanced nodes. For example, moving from larger process nodes (e.g., 28nm) to smaller ones (e.g., 7nm, 5nm) allows for the production of chips with higher performance and energy efficiency. Upgrading manufacturing equipment is essential to handle the intricacies of these advanced nodes.

Technological advancements contribute to innovations in semiconductor manufacturing processes. New techniques and methodologies, such as extreme ultraviolet (EUV) lithography and FinFET technology, enhance the precision and efficiency of semiconductor fabrication. Upgrading equipment to incorporate these innovations becomes necessary for manufacturers to stay competitive.

Which Factor is Restraining the Demand for Semiconductor Manufacturing Equipment?

High Costs Associated with Acquiring and Maintaining Advanced Equipment

Semiconductor manufacturing processes require cutting-edge machinery and technology, which often come with substantial upfront costs. Additionally, ongoing maintenance and upgrades further contribute to the overall expenses for semiconductor manufacturers.

However, the complexity and time-consuming nature of semiconductor manufacturing processes. Developing and implementing new manufacturing techniques or equipment can be challenging and may require extensive testing and optimization. This complexity can lead to longer development cycles and delays in bringing new products to market. Supply chain disruptions and geopolitical tensions can also pose challenges for semiconductor manufacturers. Dependency on specific regions for raw materials, components, or manufacturing facilities can leave companies vulnerable to disruptions caused by factors such as natural disasters, trade disputes, or political instability.

Report Segmentation

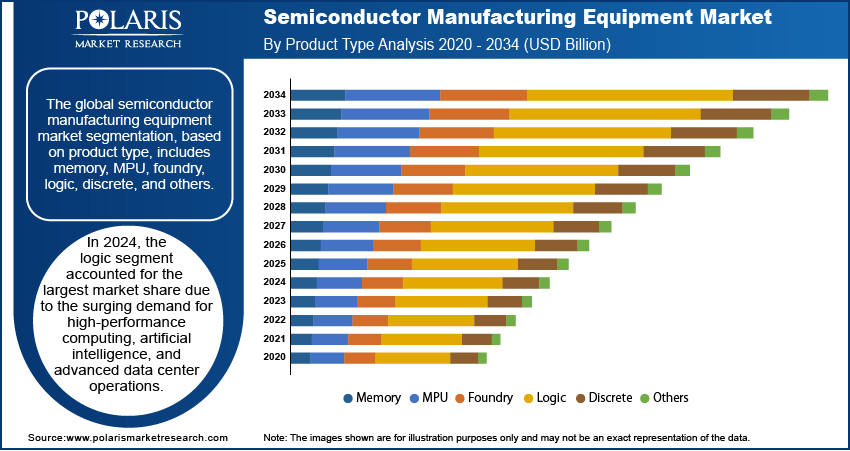

The market is primarily segmented based on product type, front-end equipment, fab facility equipment, back-end equipment, dimension, supply chain process, and region.

|

By Product Type |

By Front-End Equipment |

By Fab Facility Equipment |

By Back-End Equipment |

By Dimension |

By Supply Chain Process |

By Region |

|

|

|

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

Category Wise Insights

By Front-End Equipment Insights

Based on front-end equipment analysis, the market is segmented into lithography, wafer surface conditioning equipment, deposition, cleaning process, and other equipment. The lithography segment accounted for the largest market share in 2023 as it is a fundamental process in semiconductor manufacturing used to transfer circuit patterns onto semiconductor wafers. It plays a crucial role in defining the feature size and layout of integrated circuits (ICs). As semiconductor technology advances towards smaller nodes, the demand for high-resolution lithography equipment increases, driving market growth. Lithography is a fundamental process in semiconductor manufacturing used to transfer circuit patterns onto semiconductor wafers. It plays a crucial role in defining the feature size and layout of integrated circuits (ICs). As semiconductor technology advances towards smaller nodes, the demand for high-resolution lithography equipment increases, driving market growth.

By Dimension Insights

Based on dimension analysis, the market has been segmented based on 2D ICs, 2.5D ICs, and 3D ICs. The 3D ICs segment is expected to witness the fastest-growing CAGR during the forecast period. 3D ICs offer enhanced performance and functionality compared to traditional 2D ICs by vertically stacking multiple layers of integrated circuits. This vertical integration allows for shorter interconnection lengths, reduced signal delay, and improved power efficiency, due to superior overall performance. As a result, there is a growing demand for 3D ICs in various applications, including high-performance computing, artificial intelligence, and advanced consumer electronics. With the continuous miniaturization of electronic devices and the demand for compact form factors, 3D ICs provide a viable solution for achieving higher component density in a smaller footprint. By stacking multiple IC layers vertically, 3D ICs enable the integration of more functionality within limited space, making them attractive for applications where space constraints are critical, such as mobile devices and wearable electronics.

Regional Insights

Asia Pacific

Asia Pacific accounted for the largest market share in 2023. Asia Pacific is home to major semiconductor manufacturing hubs, particularly in countries like China, Taiwan, South Korea, and Japan. These countries host due to semiconductor companies and foundries, driving significant demand for semiconductor manufacturing equipment. The concentration of manufacturing facilities in this region contributes significantly to its market share. The Asia Pacific region has experienced rapid growth in the electronics industry, fueled by factors such as increasing consumer demand for electronic devices, technological advancements, and rising disposable incomes. This growth translates into higher demand for semiconductor chips and, consequently, semiconductor manufacturing equipment.

North America

North America region is expected to grow at the fastest CAGR during the forecast period. Particularly the United States, is a hub for technological advancements and innovation in the semiconductor industry. The region is home to major semiconductor equipment manufacturers, research institutions, and technology companies that continuously invest in research and development to develop cutting-edge semiconductor manufacturing technologies and equipment. This focus on innovation drives demand for advanced semiconductor manufacturing equipment in the region. The demand for advanced semiconductor nodes, such as 7nm, 5nm, and beyond, is growing rapidly due to the increasing complexity and performance requirements of electronic devices. North America-based semiconductor companies and foundries are at the forefront of developing and manufacturing these advanced semiconductor nodes, driving demand for state-of-the-art semiconductor manufacturing equipment.

Competitive Landscape

The Semiconductor Manufacturing Equipment Market displays fragmentation, with competition emerging from numerous players. Key service providers in this sector continually advance their technologies to stay ahead, focusing on efficiency, reliability, and safety. In pursuit of significant market share, these entities underscore the importance of strategic partnerships, continuous product improvements, and collaborative efforts to outperform industry peers.

Some of the major players operating in the global market include:

- ACM Research Inc.

- Advantest Corporation

- Applied Materials Inc.

- ASML

- Cohu, Inc.

- Dainippon Screen Group

- EV Group (EVG)

- Ferrotec Holdings Corporation

- KLA Corporation

- Lam Research Corporation

- Modutek Corporation

- Nordson Corporation

- SCREEN Semiconductor Solutions Co., Ltd.

- Tokyo Electron Limited

- Tokyo Seimitsu Co., Ltd.

Recent Developments

- In March 2023, SCREEN PE Solutions Co., Ltd., a subsidiary of SCREEN Holdings Co., Ltd., launched the Ledia 7F-L direct imaging system. Designed by SCREEN PE, this latest model addresses the rising demand for accurate pattern appearance on large-sized substrates with a particular focus on applications in IoT infrastructure and telecommunications.

- In February 2023, Applied Materials, Inc. launched VeritySEM 10, an innovative eBeam metrology system meticulously developed to specifically estimate the essential dimensions of semiconductor device components patterned with emerging high-NA EUV lithography.

Report Coverage

The semiconductor manufacturing equipment market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, front-end equipment, back-end, fab facility, dimension, supply chain participant, and their futuristic growth opportunities.

Semiconductor Manufacturing Equipment Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 100.51 Billion |

|

Revenue forecast in 2032 |

USD 233.31 billion |

|

CAGR |

11.1% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024 – 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments covered |

By Product Type, By Front-End Equipment, By Fab Facility Equipment, By Back-End Equipment, By Dimension, By Supply Chain Process, And By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region, and segmentation. |

FAQ's

The Semiconductor Manufacturing Equipment Market report covering key segments are product type, front-end equipment, fab facility equipment, back-end equipment, dimension, supply chain process, and region.

Semiconductor Manufacturing Equipment Market Size Worth $233.31 Billion By 2032

Semiconductor Manufacturing Equipment Market exhibiting a CAGR of 11.1% during the forecast period

North America is leading the global market

key driving factors in Semiconductor Manufacturing Equipment Market are 1. Growing Technological Advancements

© 2025 Polaris Market Research and Consulting. All rights reserved