Semiconductor Fabless Market Size, Share, Trends, Industry Analysis Report: By Type, End Use, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Jan-2025

- Pages: 129

- Format: PDF

- Report ID: PM5349

- Base Year: 2024

- Historical Data: 2020-2023

Semiconductor Fabless Market Overview

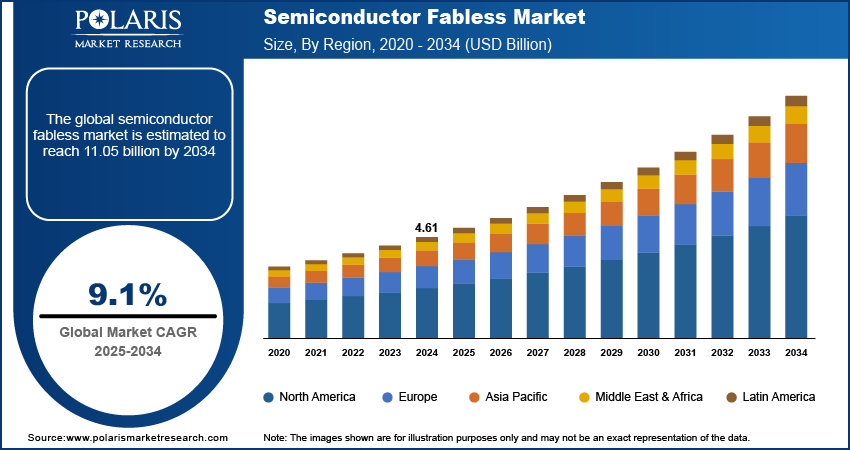

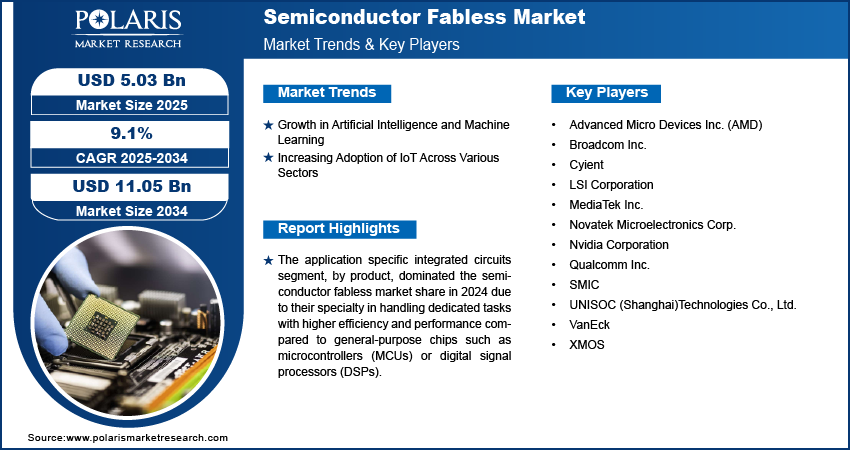

The global semiconductor fabless market size was valued at USD 4.61 billion in 2024. The market is projected to grow from USD 5.03 billion in 2025 to USD 11.05 billion by 2034, exhibiting a CAGR of 9.1% during 2025–2034.

Fabless semiconductor companies concentrate on designing and developing semiconductor chips while outsourcing their manufacturing from third-party foundries such as TSMC and GlobalFoundries. This model allows them to focus on innovation, research, and design without investing in expensive manufacturing infrastructure. Moreover, fabless companies are instrumental in driving advancements in critical technologies, including artificial intelligence (AI), 5G, and the Internet of Things (IoT), by producing highly specialized chip designs. Furthermore, companies such as NVIDIA, AMD, Qualcomm, and MediaTek are dominating the semiconductor fabless market, supplying chips for diverse applications from data centers and smartphones to automotive systems and consumer electronics. The outsourcing strategy also enhances agility and cost-efficiency, enabling these companies to quickly scale and adapt to changing market demands.

To Understand More About this Research: Request a Free Sample Report

Continuous advancements in the fabless semiconductor market are driven by the relentless pursuit of innovation, which is fueled by emerging technologies and shifting consumer demands. As applications for AI, machine learning, 5G, and IoT proliferate, fabless companies are increasingly focusing on creating specialized chips that enhance performance, efficiency, and functionality. This has led to significant investments in research and development, enabling the creation of more sophisticated architectures, such as application-specific integrated circuits (ASICs) and system-on-chip (SoC) designs.

Semiconductor Fabless Market Trends

Growth in Artificial Intelligence and Machine Learning

The integration of Artificial Intelligence (AI) and Machine Learning (ML) across various sectors is driving demand for specialized semiconductors, such as GPUs and AI accelerators. The GPU chips provide the computational power required for real-time data processing and are essential for efficiently training and running AI models in cloud computing. Furthermore, there is a growing demand for advanced AI accelerators in applications such as autonomous vehicles, healthcare, manufacturing, and finance. As fabless semiconductor companies innovate to meet the increasing need for powerful and efficient AI and ML chips, the demand for semiconductors continues to rise. This competitive landscape includes established players such as NVIDIA and AMD, alongside emerging companies racing to develop the next generation of AI chips. Consequently, the fabless semiconductor market is expected to experience substantial growth in the coming years, fueled by the widespread adoption of AI and ML technologies across both consumer and enterprise applications.

Increasing Adoption of IoT Across Various Sectors

The widespread adoption of the Internet of Things (IoT) in industries such as healthcare, smart homes, and manufacturing is significantly increasing the demand for low-power, high-performance semiconductors. In healthcare, IoT devices such as wearables and remote monitoring systems rely on specialized chips that can process real-time data, ensure secure data transmission, and consume minimal power. Fabless companies design custom SoCs (System-on-Chips) to meet these needs. In the smart home sector, devices such as smart thermostats and security systems depend on semiconductors optimized for energy efficiency and seamless wireless connectivity. Leading fabless semiconductor manufacturers, such as Qualcomm and MediaTek, develop chips that power these smart home solutions.

In manufacturing, IoT is essential for smart factories that rely on interconnected machines and sensors to optimize production. Fabless companies are responsible for creating durable, scalable chips that can operate reliably in harsh industrial environments. Key players such as NXP Semiconductors and STMicroelectronics develop custom IoT solutions to meet the demands of the manufacturing industry. Since the adoption of IoT continues to grow, the need for specialized semiconductors that provide efficiency, connectivity, and real-time data processing is expected to rise, which would drive the fabless semiconductor market growth during the forecast period.

Semiconductor Fabless Market Segment Outlook

Semiconductor Fabless Market Evaluation, by Type Outlook

The global semiconductor fabless market segmentation, based on type, includes microcontrollers (MCUs), digital signal processors (DSP), graphic processing units (GPUs), application specific integrated circuits (ASIC), power management ICs (PMICs), and others. In 2024, the application specific integrated circuits segment dominated the market due to their specialty in handling dedicated tasks with higher efficiency and performance compared to general-purpose chips such as microcontrollers (MCUs) or digital signal processors (DSPs). ASICs are specifically designed to meet the requirements of industries such as cryptocurrency mining, autonomous vehicles, and networking infrastructure, where customized performance, power efficiency, and speed are critical.

The ASIC’s significance is amplified by growing demand in various sectors such as AI, 5G, and automotive electronics, where ASICs play a pivotal role in efficiently managing complex processing tasks. For example, Nvidia designs custom ASICs to optimize AI models and deep learning tasks, making these chips essential for data centers and AI applications. As the demand for specialized applications such as machine learning and autonomous systems continues to grow, ASICs are expected to remain dominant, fueling the fabless semiconductor market expansion. Thus, this trend underscores the increasing role of custom chips in meeting the evolving requirements of advanced technologies.

Semiconductor Fabless Market Assessment, by End Use Outlook

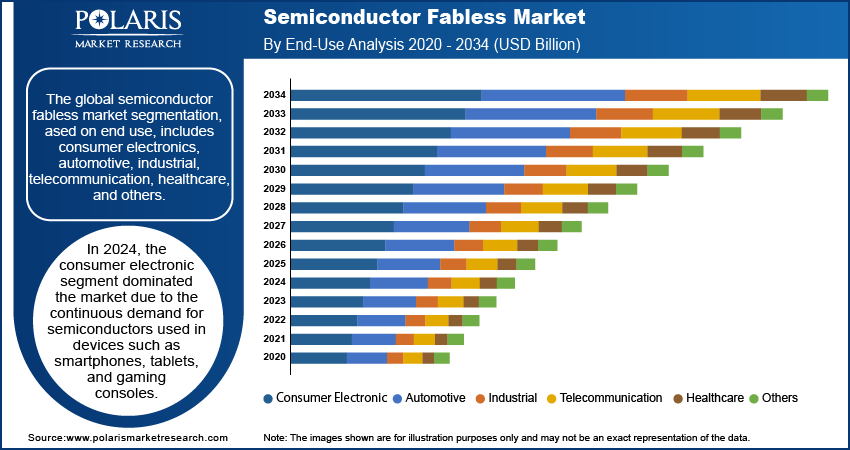

The global semiconductor fabless market segmentation, based on end use, includes consumer electronics, automotive, industrial, telecommunication, healthcare, and others. In 2024, the consumer electronics segment dominated the market due to the continuous demand for semiconductors used in devices such as smartphones, tablets, and gaming consoles. Companies such as Apple, Samsung, and Sony depend on high-performance, energy-efficient chips designed by fabless semiconductor firms to meet growing consumer demand. The increasing popularity of smartphones and smart devices has significantly boosted the demand for System-On-Chip (SoC) designs. Leading companies such as Qualcomm and MediaTek dominate this segment by delivering innovative chip solutions. Furthermore, the ongoing shift toward 5G connectivity and IoT devices continues to drive demand in the market, requiring advanced semiconductor technologies. As consumer interest in AI-powered devices, smart homes, and wearables expands, the consumer electronics sector remains the primary revenue driver for fabless semiconductor manufacturers.

The automotive sector is emerging as an essential revenue stream for fabless semiconductor manufacturers as vehicles become increasingly intelligent and electrified. Additionally, companies such as Tesla and General Motors depend on fabless firms to supply reliable, high-performance chips that support advanced features such as autonomous driving, electric vehicle powertrains, and in-car AI systems. Thus, this dependence highlights the growing role of fabless semiconductors in shaping the future of automotive technology.

Semiconductor Fabless Market Regional Insights

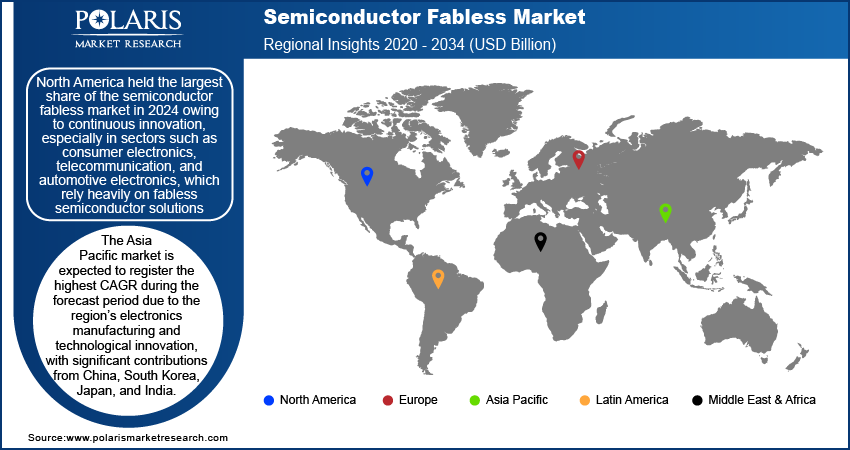

By region, the study provides semiconductor fabless market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America accounted for the largest market share in 2024 due to its robust infrastructure and strong presence of leading semiconductor companies. The region benefits from significant R&D investments and a well-established tech ecosystem. The demand for advanced semiconductors in areas such as AI, cloud computing, and automotive also contributes to this growth. Furthermore, the expansion of manufacturing facilities and increased investments in fabless semiconductor technology solidifies North America’s leadership. Companies in the region are increasingly focusing on next-generation chip designs and AI-driven semiconductors. North America’s dominance is reinforced by continuous innovation, especially in sectors such as consumer electronics, telecommunication, and automotive electronics, which are dependent on fabless semiconductor solutions.

The Asia Pacific semiconductor fabless market is expected to register the highest CAGR during the forecast period due to the region’s electronics manufacturing and technological innovation, with significant contributions from China, South Korea, Japan, and India. The growing consumer electronics industry, expanding IoT applications, and advancements in 5G technology are driving demand for innovative semiconductor components. In May 2024, Mindgrove Technologies, a fabless semiconductor startup backed by Peak XV Partners, introduced India’s first commercial high-performance system on chip (SoC), named Secure IoT. This RISC-V-based chip enables Indian OEMs to integrate a locally developed SoC into their products, helping to lower the cost of their feature-rich devices without sacrificing advanced capabilities. The Secure IoT chip is expected to be 30% more affordable than comparable chips in its segment.

Semiconductor Fabless Market Key Players and Competitive Insights

The competitive landscape of the semiconductor fabless market is characterized by a diverse array of global and regional players striving to capture market share through innovation, strategic partnerships, and geographic expansion. Major players in the industry, including AMD, NVIDIA Corporation, and Qualcomm, leverage their extensive R&D capabilities and broad distribution networks to offer a wide range of advanced semiconductor fabless products. These companies focus on product innovation, including improvements in safety, functionality, and cost-efficiency, to meet the evolving needs of healthcare providers. Additionally, smaller and regional companies are increasingly entering the market, offering specialized and niche products that cater to specific technology needs or local market demands. Competitive strategies often include mergers and acquisitions, partnerships with institutions, and investments in emerging markets to expand reach and enhance market presence. A few major semiconductor fabless market players are Broadcom Inc., Qualcomm Inc., NVIDIA Corporation, Advanced Micro Devices Inc. (AMD), MediaTek Inc., Novatek Microelectronics Corp, UNISOC (Shanghai) Technologies Co. Ltd, XMOS, LSI Corporation, SMIC, and Cyient.

Cyient is an Indian multinational technology company focused on engineering, manufacturing, data analytics, networks, and operations. The company announced a strategic expansion of its semiconductor business with the establishment of a fully owned subsidiary in July 2024. The subsidiary will focus on designing and selling specialized chips using a fabless model for analog mixed-signal chips. Cyient has been active in semiconductors for many years, offering services such as chip design consulting, in-house IC development, and post-silicon validation. The subsidiary will also help Cyient adapt to market cycles and address the technology and capital requirements of the industry more effectively.

VanEck, a global investment management firm based in New York, announced the launch of VanEck Fabless Semiconductor ETF (SMHX) in August 2024, the latest addition to its range of thematic equity ETFs. SMHX focuses on fabless semiconductor companies that prioritize design and R&D over manufacturing.

List of Key Companies in Semiconductor Fabless Market

- Advanced Micro Devices Inc. (AMD)

- Broadcom Inc.

- Cyient

- LSI Corporation

- MediaTek Inc.

- Novatek Microelectronics Corp.

- Nvidia Corporation

- Qualcomm Inc.

- SMIC

- UNISOC (Shanghai)Technologies Co., Ltd.

- VanEck

- XMOS

Semiconductor Fabless Industry Developments

In November 2023, Broadcom Inc., a global technology leader that designs, develops, and supplies semiconductor and infrastructure software solutions, completed its acquisition of VMware, Inc. aiming to enhance its software and cloud infrastructure capabilities, which complement its semiconductor business.

In September 2024, Tata Electronics signed an MoU with Tokyo Electron (TEL) to purchase equipment and services for its semiconductor facilities in Gujarat and Assam. The partnership will focus on workforce training, R&D, and enhancing semiconductor infrastructure.

In September 2024, The US Department of State announced that they will partner with the India Semiconductor Mission, Ministry of Electronics and IT, and Government of India to explore opportunities to grow and diversify the global semiconductor ecosystem under the International Technology Security and Innovation (ITSI) Fund, created by the CHIPS Act of 2022 (CHIPS Act). This partnership will help create a more resilient, secure, and sustainable global semiconductor value chain.

Semiconductor Fabless Market Segmentation

By Type Outlook

- Microcontrollers (MCUs)

- Digital Signal Processors (DSPs)

- Graphic Processing Units (GPUs)

- Application Specific Integrated Circuits (ASICs)

- Power Management ICs (PMICs)

- Others

By End Use Outlook

- Consumer Electronics

- Automotive

- Industrial

- Telecommunication

- Healthcare

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Semiconductor Fabless Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 4.61 billion |

|

Market Size Value in 2025 |

USD 5.03 billion |

|

Revenue Forecast By 2034 |

USD 11.05 billion |

|

CAGR |

9.1% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global semiconductor fabless market size was valued at USD 4.61 billion in 2024 and is projected to grow to USD 11.05 billion by 2034.

The global market is projected to exhibit a CAGR of 9.1% during the forecast period.

North America held the largest market share owing to continuous innovation, especially in sectors such as consumer electronics, telecommunication, and automotive electronics, which rely heavily on fabless semiconductor solutions

A few key players in the market are Broadcom Inc., Qualcomm Inc., NVIDIA Corporation, Advanced Micro Devices Inc. (AMD), MediaTek Inc., Novatek Microelectronics Corp, UNISOC (Shanghai) Technologies Co. Ltd, XMOS, LSI Corporation, SMIC, and Cyient.

In 2024, the consumer electronic segment dominated the market due to the continuous demand for semiconductors used in devices such as smartphones, tablets, and gaming consoles.

© 2025 Polaris Market Research and Consulting. All rights reserved