Semiconductor Dry Etch System Market Size, Share, Trends, Industry Analysis Report: By Technique, Application (Consumer Electronics and Automotive), and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Nov-2024

- Pages: 125

- Format: PDF

- Report ID: PM5201

- Base Year: 2024

- Historical Data: 2020-2023

Semiconductor Dry Etch Systems Market Overview

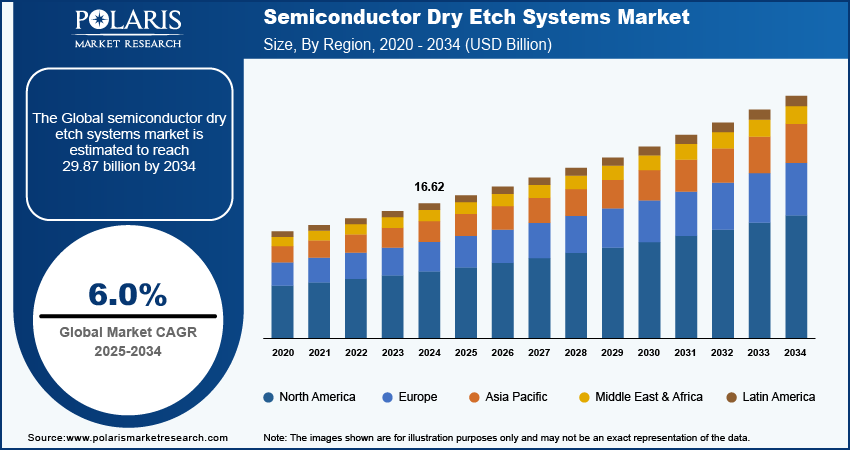

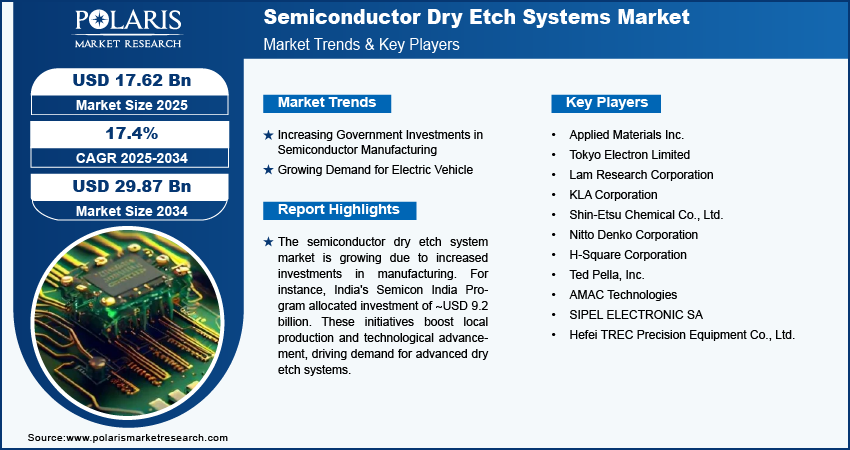

The semiconductor dry etch systems market size was valued at USD 16.62 billion in 2024. The market is projected to grow from USD 17.62 billion in 2025 to USD 29.87 billion by 2034, exhibiting a CAGR of 6.0% during 2025–2034.

A semiconductor dry etch system is a critical piece of equipment used in the fabrication of semiconductor devices. It utilizes dry etching techniques to selectively remove material from a semiconductor wafer's surface, creating the intricate patterns needed for integrated circuits and microelectronic devices.

The increasing demand for advanced technologies is significantly driving the semiconductor dry etch system market growth. As industries adopt advanced innovations such as 5G networks, artificial intelligence, and the Internet of Things (IoT), the demand for sophisticated semiconductor components is increasing. These technologies require semiconductors with complex architectures and higher performance capabilities, achievable only through precision manufacturing processes. Thus, the growing demand for advanced technologies in telecommunication and consumer electronics requires high-performance dry etch systems capable of producing smaller, more efficient chips while maintaining rigorous quality and miniaturization standards. As manufacturers strive to enhance device performance and integrate new functionalities, the evolution of dry etch technologies becomes crucial, positively impacting the growth of the semiconductor dry etch system market.

To Understand More About this Research: Request a Free Sample Report

The growing application of sophisticated semiconductors in consumer electronics is expected to drive the semiconductor dry etch system market growth during the forecast period. As consumer demand shifts toward innovative technologies such as wearable devices, smart home products, and advanced healthcare solutions, the complexity of semiconductor components increases. These applications require high-performance chips that can accommodate new functionalities, which necessitates precise manufacturing techniques such as dry etching.

The expansion of smart devices and connected technologies has led to a high demand for semiconductors. This increase in demand pushes manufacturers to adopt advanced dry etch systems capable of producing intricate designs with high precision and efficiency. Moreover, as companies plan to differentiate their products in a competitive market, the need for compact semiconductor fabrication processes becomes necessary. Thus, the rising application of semiconductors in consumer electronics with advanced technology is expected to fuel the growth of the semiconductor dry etch systems market during the forecast period.

Semiconductor Dry Etch Systems Market Trends

Increasing Government Investments in Semiconductor Manufacturing

Governments and private sectors across the world are recognizing the strategic importance of semiconductors, leading to substantial financial commitments to enhance production capabilities. For instance, according to the India Brand Equity Foundation, India initiated the Semicon India Program in December 2021 with an initial allocation of ∼USD 9.2 billion to develop its semiconductor and display manufacturing ecosystems. In the interim Union Budget for 2024, this allocation was raised to about USD 833.7 million, demonstrating ongoing support for the industry. Moreover, the revised estimates for the Modified Program for Development of Semiconductors and Display Manufacturing Ecosystem in India during FY24 highlight an expenditure of ∼USD 181.5 million. Such investments aim to boost local production, accelerate technological advancements, and attract global players to set up manufacturing facilities across the country.

Rising government initiatives will accelerate the demand for advanced dry etch systems during the forecast period for producing the high-performance chips needed in emerging technologies. Consequently, the rising investments in semiconductor manufacturing, coupled with the expansion of local and global players, would drive the demand for dry etch systems. Therefore, the semiconductor dry etch system market is expected to experience significant growth and demand due to increasing government investments in semiconductor manufacturing.

Growing Demand for Electric Vehicles

The increasing shift of the automotive industry toward electrification propels the demand for semiconductors crucial for EV components such as batteries, power electronics, and advanced driver-assistance systems (ADAS). According to the International Energy Agency, sales of electric cars skyrocketed to 16 million units per year in 2023, up from just 0.2 million in 2012.

In the first quarter of 2024 alone, ∼3 million EVs were sold, marking a notable increase compared to the previous year. With a total of 40 million electric cars registered to date, the demand for semiconductor manufacturers to produce high-performance chips is increasing. This increased demand necessitates advanced manufacturing processes, including precise dry etching techniques, to create the complex circuitry needed for EV technologies. As the EV market continues to expand, the demand for reliant and efficient dry etch systems will rise during the forecast period.

Semiconductor Dry Etch Systems Market Segment Insights

Semiconductor Dry Etch Systems Market Breakdown, by Technique Insights

The semiconductor dry etch systems market, based on technique, is segmented into reactive ion etching, inductively coupled plasma etching, and deep reactive ion etching. The deep reactive ion etching segment is expected to record the highest CAGR in the global market during the forecast period due to its ability to create high-aspect-ratio structures essential for advanced applications. This technique allows for precise etching of materials such as silicon and silicon compounds, making it ideal for MEMS (Micro-Electro-Mechanical Systems) and 3D integrated circuits. Thus, due to its advanced ability, the deep reactive ion etching segment is expected to record a significant growth rate in the semiconductor dry etch system market during the forecast period.

Semiconductor Dry Etch Systems Market Breakdown, by Application Insights

The semiconductor dry etch systems market segmentation, based on application, includes consumer electronics, automotive, and telecommunications. The consumer electronics segment is expected to dominate the market during the forecast period due to the growing number of consumers using smart devices. There has been a rise in connected gadgets such as smart thermostats, wearable health monitors, and other consumer electronics. More people are interested in advanced electronic gadgets, leading to increased demand for advanced semiconductors. As advanced semiconductor manufacturing grows, the use of dry etch systems for manufacturing also increases.

Semiconductor Dry Etch Systems Market Regional Insights

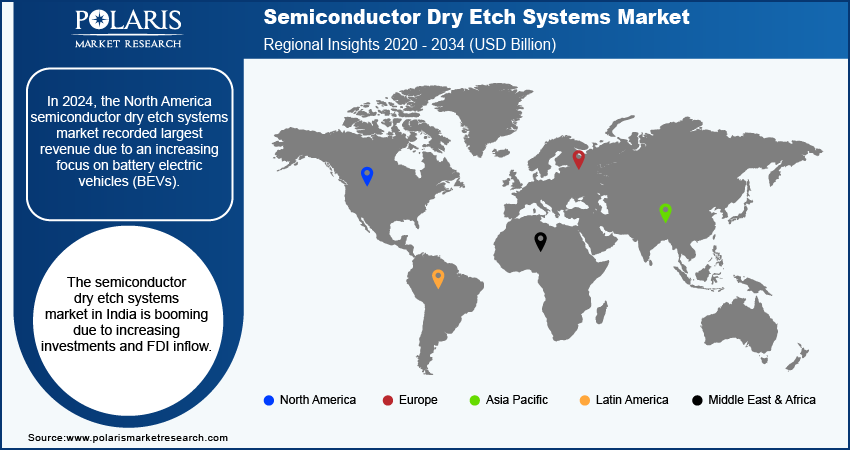

By region, the study provides the semiconductor dry etch systems market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America held the largest revenue share in the semiconductor dry etch systems market due to the increasing focus on battery electric vehicles (BEVs) that has led to heightened demand for advanced semiconductor components essential for various vehicle systems, including battery management, power distribution, and infotainment.

According to the Federal Reserve Bank of Chicago, from 2000 to 2021, battery electric vehicle sales reached 400,000 units in the US, showcasing a growing consumer interest in sustainable transportation solutions. As automakers invest in EV technology, the demand for high-performance semiconductors is set to increase, driving manufacturers to adopt sophisticated dry etching techniques, leading to the growth of the semiconductor dry etch systems market.

The Asia Pacific semiconductor dry etch systems market is projected to register a substantial CAGR during the forecast period due to an increase in mergers and acquisitions aimed at market expansion. Major semiconductor companies are increasingly consolidating to enhance their technological capabilities and broaden their product portfolios. This strategic move facilitates access to advanced manufacturing processes, including sophisticated dry etching techniques necessary for producing high-performance chips.

As these companies seek to leverage synergies and improve operational efficiencies, the semiconductor landscape is set to expand, leading to an increase in demand for semiconductor dry etch systems. Consequently, an increase in mergers, acquisitions, and partnerships is set to fuel the semiconductor dry etch systems market growth during the forecast period.

The India semiconductor dry etch systems market is experiencing significant growth, fueled by increasing foreign direct investments (FDIs) and strong investments in key end-user industries such as automotive, semiconductor, and telecommunications. According to Invest India, between April 2000 and September 2023, the automobile sector attracted ∼USD 35.40 billion in equity FDI, underscoring the country’s appeal to global investors. This influx of capital is driving advancements in semiconductor manufacturing capabilities, particularly as the automotive industry shifts toward electric vehicles and smart technologies. As companies expand their operations and adopt advanced manufacturing processes, the demand for sophisticated dry etch systems in India is expected to rise, propelling the growth of the semiconductor dry etch market during the forecast period.

Semiconductor Dry Etch Systems Market – Key Players and Competitive Insights

The semiconductor dry etch systems market is constantly evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, advanced software technologies, and significant capital to maintain a competitive edge. These companies pursue strategic initiatives such as mergers, acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

New companies are impacting the industry by introducing innovative devices and meeting the needs of sectors. This competitive environment is amplified by continuous progress in product offerings and new techniques, greater emphasis on sustainability, and the rising requirement for tailor-made products in diverse industries. A few major players in the semiconductor dry etch systems market are Applied Materials Inc.; Tokyo Electron Limited; Lam Research Corporation; KLA Corporation; Shin-Etsu Chemical Co., Ltd.; Nitto Denko Corporation; H-Square Corporation; Ted Pella, Inc.; AMAC Technologies; SIPEL ELECTRONIC SA; and Hefei TREC Precision Equipment Co., Ltd.

Tokyo Electron Limited, established on November 11, 1963, and headquartered in Minato-ku, Tokyo, Japan, is a global supplier of semiconductor and flat panel display (FPD) production equipment. The company operates as a subsidiary of Tokyo Electron Group and is listed on the Tokyo Stock Exchange. TEL has grown to become a pivotal player in the semiconductor manufacturing industry. Tokyo Electron manufactures a wide range of equipment essential for semiconductor fabrication processes. Its product portfolio includes wafer vacuum assembling equipment, cleaning systems, deposition systems, and etch systems. It operates primarily in regions such as Japan, North America, Europe, and Asia. The Tokyo Electron dry etch products include the Tactras and ACT12 systems, which are designed for advanced applications such as 3D NAND flash memory and flat panel displays.

Lam Research Corporation, established in 1980, is a supplier of wafer fabrication equipment and services for the semiconductor industry. Headquarter in Fremont, California, the company is publicly traded on the NASDAQ. Its product portfolio includes etch, deposition, and cleaning systems. Lam Research serves various regions, including North America, Europe, and Asia, supporting advanced manufacturing processes for semiconductor devices and enabling the production of smaller, more powerful chips in the global market. On March 3, 2020, Lam Research Corporation announced the launch of its new Sense. I plasma etch technology and system solution. This platform, featuring Lam’s Equipment Intelligence technology, was designed to enhance productivity and reduce floor space in semiconductor fabs. The Sense. I system offered advanced etch capabilities and a compact architecture, significantly improving etch output density by over 50%. The innovation was set to support future technology developments while addressing the cost-scaling challenges faced by chipmakers in the evolving semiconductor landscape.

Key Companies in Semiconductor Dry Etch Systems Market

- Applied Materials Inc.

- Tokyo Electron Limited

- Lam Research Corporation

- KLA Corporation

- Shin-Etsu Chemical Co., Ltd.

- Nitto Denko Corporation

- H-Square Corporation

- Ted Pella, Inc.

- AMAC Technologies

- SIPEL ELECTRONIC SA

- Hefei TREC Precision Equipment Co., ltd.

Semiconductor Dry Etch Systems Market Industry Developments

August 2020: Applied Materials, Inc. announced the launch of its new Centris Sym3 Y etch system, enhancing the Centris Sym3 etch product family. This advanced conductor etch system was designed to enable chipmakers to pattern smaller features in leading-edge memory and logic chips precisely. Utilizing innovative RF pulsing technology, the Sym3 Y system provided high materials selectivity and exceptional etch profile control.

March 2021: Tokyo Electron (TEL) announced the launch of the Impressio 1800 PICP Pro and Betelex 1800 PICP Pro plasma etch systems, featuring the new PICP Pro chamber for high-resolution processing of 6th-generation glass substrates. Designed to meet the growing demand for high-resolution OLED displays in smartphones, the PICP Pro technology provided enhanced plasma control and reduced particle generation. This innovation was aimed at improving maintenance and yield, ultimately achieving lower running costs and superior etch precision in advanced display manufacturing.

Semiconductor Dry Etch Systems Market Segmentation

By Technique Outlook (USD Billion, 2020–2034)

- Reactive Ion Etching

- Inductively Coupled Plasma Etching

- Deep Reactive Ion Etching

By Application Outlook (USD Billion, 2020–2034)

- Consumer Electronics

- Automotive

- Telecommunications

By Regional Outlook (USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Semiconductor Dry Etch Systems Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 16.62 billion |

|

Market Size Value in 2025 |

USD 17.62 billion |

|

Revenue Forecast by 2034 |

USD 29.87 billion |

|

CAGR |

6.0% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report End User |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The semiconductor dry etch systems market size was valued at USD 16.62 billion in 2024 and is projected to grow to USD 29.87 billion by 2034.

The global market is projected to register a CAGR of 6.0% during 2025–2034.

North America accounted for the largest share of the global market in 2024.

A few key players in the market are Applied Materials Inc.; Tokyo Electron Limited; Lam Research Corporation; KLA Corporation; Shin-Etsu Chemical Co., Ltd.; Nitto Denko Corporation; H-Square Corporation; Ted Pella, Inc.; AMAC Technologies; SIPEL ELECTRONIC SA; and Hefei TREC Precision Equipment Co., Ltd.

The deep reactive ion etching segment is anticipated to experience substantial growth with a significant CAGR in the global market during the forecast period due to its advanced abilities and cost effectiveness.

The consumer electronics segment accounted for the largest revenue share of the market in 2024 due to the increasing number of consumers adopting smart devices.

© 2025 Polaris Market Research and Consulting. All rights reserved