Prostate Cancer Treatment Market Size, Share, Trends, Industry Analysis Report: By Drug Class (Hormonal Therapy, Chemotherapy, Immunotherapy, Targeted Therapy, and Others), Distribution Channel, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Mar-2025

- Pages: 118

- Format: PDF

- Report ID: PM1395

- Base Year: 2024

- Historical Data: 2020-2023

Prostate Cancer Treatment Market Overview

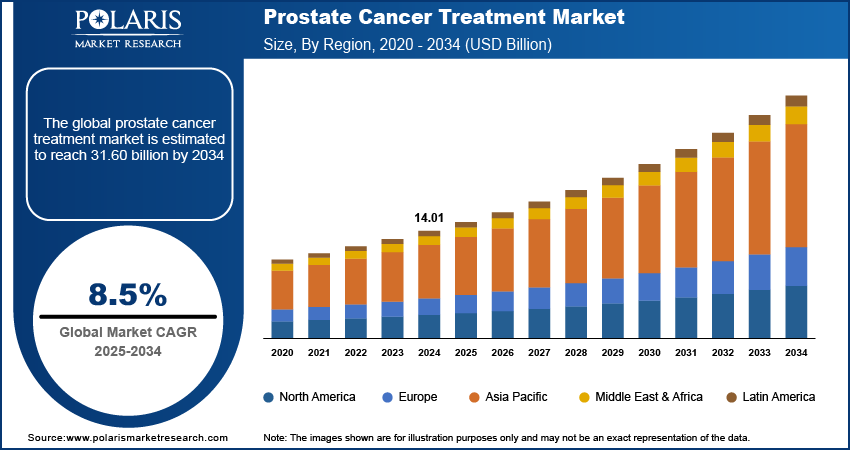

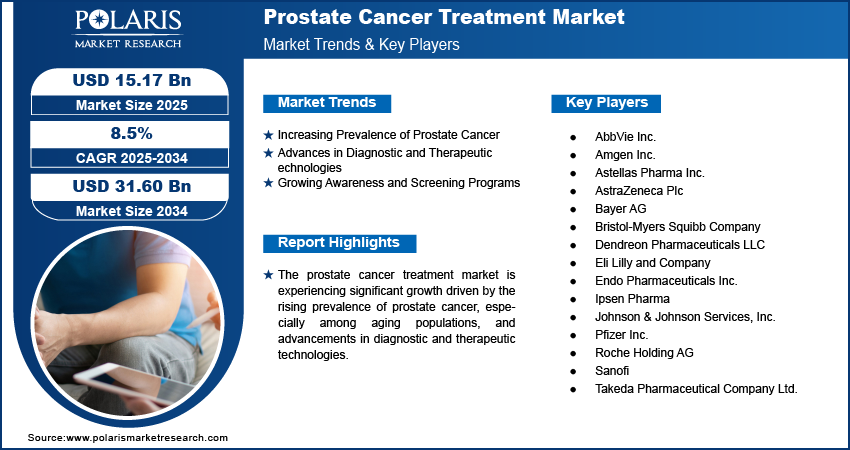

The prostate cancer treatment market size was valued at USD 14.01 billion in 2024. The market is projected to grow from USD 15.17 billion in 2025 to USD 31.60 billion by 2034, exhibiting a CAGR of 8.5% during 2025–2034.

The prostate cancer treatment market encompasses the development, production, and distribution of therapies and interventions used to manage prostate cancer. This includes hormonal therapies, chemotherapy, radiation therapy, immunotherapy, and advanced treatments such as targeted therapies and radiopharmaceuticals. Key drivers of this market include the rising prevalence of prostate cancer globally, advancements in diagnostic and therapeutic technologies, and increasing healthcare expenditures. Notable trends include the growing adoption of minimally invasive procedures, the emergence of precision medicine, and the increasing use of combination therapies to improve treatment outcomes. Regulatory approvals for novel therapies and growing awareness about early screening are further fueling the prostate cancer treatment market demand.

To Understand More About this Research:Request a Free Sample Report

Prostate Cancer Treatment Market Dynamics

Increasing Prevalence of Prostate Cancer

The prevalence of prostate cancer is rising significantly across the world. According to the World Health Organization (WHO), prostate cancer is among the most common cancers in men, with ∼1.4 million new cases diagnosed globally in 2020. Factors such as aging populations and improved diagnostic capabilities contribute to the growing number of diagnoses. The increasing burden of this disease has intensified the demand for effective treatment options, driving innovation. Thus, the rising prevalence of prostate cancer drives the prostate cancer treatment market growth.

Advances in Diagnostic and Therapeutic Technologies

Enhanced imaging techniques, such as multiparametric MRI and PSMA PET-CT, have improved early detection and staging accuracy of cancer. On the therapeutic front, innovations such as radiopharmaceuticals, robotic-assisted surgeries, and targeted therapies are becoming more accessible. The FDA approved the radiopharmaceutical drug Pluvicto (lutetium Lu 177 vipivotide tetraxetan) in 2022 for treating advanced prostate cancer, marking a breakthrough in precision medicine. These technological developments are assisting healthcare professionals in providing advanced and personalized treatment solutions. Therefore, technological advancements in diagnostics and therapeutics have positively impacted the prostate cancer treatment market development.

Growing Awareness and Screening Programs

Efforts by organizations such as the American Cancer Society and the European Association of Urology have emphasized early screening and regular health checks for at-risk populations, including men aged 50 years and above. Increased awareness has led to earlier detection, which significantly improves treatment success rates. For example, the National Cancer Institute (NCI) highlights that early-stage prostate cancer has a nearly 100% five-year survival rate with proper treatment. This has prompted higher adoption of therapeutic interventions. Hence, awareness campaigns and expanded prostate cancer screening programs are driving the prostate cancer treatment market growth.

Prostate Cancer Treatment Market Segment Insights

Prostate Cancer Treatment Market Assessment – Drug Class-Based Insights

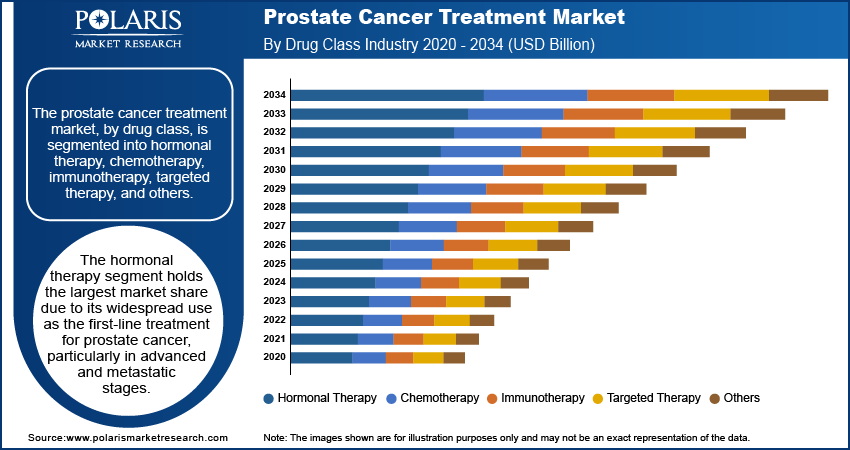

The prostate cancer treatment market, by drug class, is segmented into hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and others. The hormonal therapy segment holds the largest market share due to its widespread use as the first-line treatment for prostate cancer, particularly in advanced and metastatic stages. Androgen deprivation therapies (ADTs) and androgen receptor inhibitors are key components of this segment, benefiting from their established efficacy and the growing number of patients diagnosed at advanced stages. Drugs such as enzalutamide and abiraterone acetate are significant contributors to the dominance of this segment, supported by their broad adoption in clinical practice.

The targeted therapy segment is projected to register the highest growth during the forecast period, driven by advancements in precision medicine and increasing approvals of novel agents. The emergence of radiopharmaceuticals and PARP inhibitors has expanded the therapeutic options for patients suffering from specific genetic mutations or metastatic conditions. The FDA approval of Lynparza (olaparib) for BRCA-mutated metastatic prostate cancer underscores the growing importance of personalized medicine biomarker in this segment. Rising research and development activities and an increasing focus on biomarker-driven treatments are expected to fuel the demand for targeted therapies, marking a transformative shift in prostate cancer management.

Prostate Cancer Treatment Market Outlook – Distribution Channel-Based Insights

The prostate cancer treatment market, by distribution channel, is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies. The hospital pharmacies segment dominates the prostate cancer treatment market share due to their role in facilitating access to specialized oncology treatments. These pharmacies are integral to the administration of advanced therapies, including hormonal treatments, chemotherapy, and targeted therapies, as they ensure proper handling, storage, and dispensing of these drugs under professional supervision. Additionally, the presence of oncology departments within hospitals supports the preference for hospital pharmacies, particularly for injectable and infused therapies requiring professional administration.

The online pharmacies segment is experiencing the highest growth rate, driven by increasing digitalization and a shift toward convenient, home-based healthcare solutions. The ease of ordering medications online, coupled with enhanced delivery services and the availability of patient support programs, has contributed to their rising popularity. This trend has been further accelerated by the COVID-19 pandemic, which heightened the adoption of online pharmacy platforms. Patients undergoing prostate cancer treatment with oral medications, such as hormonal therapies or targeted drugs, increasingly rely on online channels, supported by the growing adoption of telemedicine and e-prescriptions.

Prostate Cancer Treatment Market Regional Insights

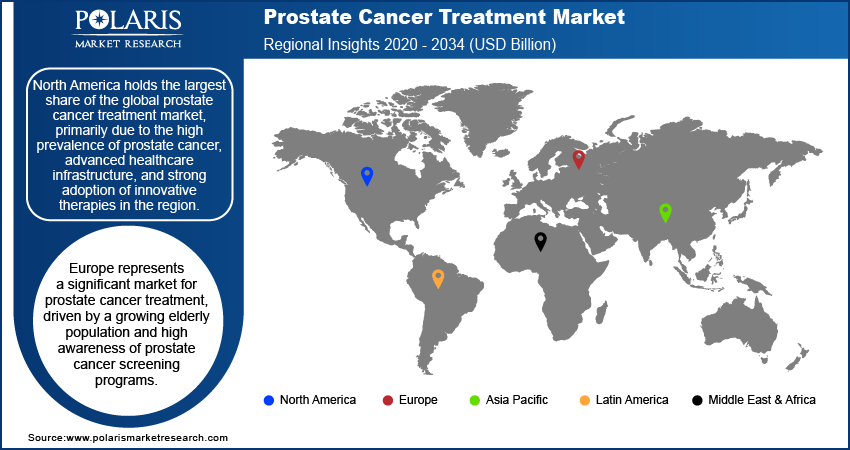

By region, the study provides prostate cancer treatment market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest share of the prostate cancer treatment market revenue, primarily due to the high prevalence of prostate cancer, the presence of advanced healthcare infrastructure, and the strong adoption of innovative therapies in the region. According to the American Cancer Society, prostate cancer is the most common cancer among men in the US, with an estimated 288,300 new cases in 2023 alone. The region benefits from significant investments in research and development, leading to early access to novel treatments such as targeted therapies and immunotherapies. Additionally, widespread awareness campaigns and robust screening programs contribute to early diagnosis and increased treatment uptake. The presence of key market players and favorable reimbursement policies further boost the dominance of North America in the global prostate cancer treatment market.

Europe represents a significant market for prostate cancer treatment, driven by a growing elderly population and high awareness of prostate cancer screening programs. Countries such as Germany, the UK, and France lead the regional market due to their advanced healthcare systems and strong focus on cancer research. Government initiatives promoting early diagnosis and the availability of innovative therapies contribute to market growth. Additionally, ongoing clinical trials and collaborations between academic institutions and pharmaceutical companies further support advancements in prostate cancer management across the region.

Asia Pacific is emerging as a rapidly growing market for prostate cancer treatment, fueled by increasing healthcare investments, rising prevalence of the disease, and improved access to medical care. Countries such as China, Japan, and India are witnessing significant growth due to the expanding healthcare infrastructure and the adoption of modern diagnostic and therapeutic approaches. Rising awareness about prostate cancer, coupled with government-led health campaigns and initiatives, is driving earlier diagnosis and treatment. The region’s growing pharmaceutical industry and focus on cost-effective treatment solutions further propel the prostate cancer treatment market expansion in Asia Pacific.

Prostate Cancer Treatment Market – Key Players and Competitive Insights

The prostate cancer treatment market includes active participation from companies such as Astellas Pharma Inc., AstraZeneca plc, Bayer AG, Bristol-Myers Squibb Company, F. Hoffmann-La Roche AG, Ferring Pharmaceuticals Inc., GlaxoSmithKline plc, Ipsen Pharma, Johnson & Johnson, Pfizer Inc., Sanofi, Amgen Inc., Dendreon Pharmaceuticals LLC, Endo Pharmaceuticals Inc., and Takeda Pharmaceutical Company Ltd. These organizations are actively involved in developing and commercializing innovative therapies, including hormonal treatments, chemotherapy, immunotherapy, and targeted therapies, to meet the evolving needs of prostate cancer patients worldwide. Their extensive research and development efforts have led to the introduction of new drugs and treatment modalities, enhancing patient outcomes and expanding the therapeutic landscape.

In the competitive landscape, companies such as Johnson & Johnson Services, Inc., through its subsidiary Janssen Biotech, and Astellas Pharma Inc. have made significant strides with products such as Zytiga and Xtandi, respectively, which have become standard treatments in advanced prostate cancer. Bayer AG has also strengthened its position with Nubeqa, a drug co-developed with Finland's Orion Corporation, which has achieved blockbuster status with over a billion euros in sales.

Johnson & Johnson, through its subsidiary Janssen Biotech, is a significant player in the prostate cancer treatment market. The company offers Zytiga (abiraterone acetate), a widely used hormonal therapy for metastatic prostate cancer, and Erleada (apalutamide), designed for non-metastatic castration-resistant prostate cancer. These therapies are integral to the company’s oncology portfolio.

Bayer is a prominent pharmaceutical company in the prostate cancer treatment market, particularly known for Nubeqa (darolutamide), which targets non-metastatic castration-resistant prostate cancer. Nubeqa has seen growing adoption due to its safety and efficacy profile.

List of Key Companies in Prostate Cancer Treatment Market

- AbbVie Inc.

- Amgen Inc.

- Astellas Pharma Inc.

- AstraZeneca Plc

- Bayer AG

- Bristol-Myers Squibb Company

- Dendreon Pharmaceuticals LLC

- Eli Lilly and Company

- Endo Pharmaceuticals Inc.

- Ipsen Pharma

- Johnson & Johnson Services, Inc.

- Pfizer Inc.

- Roche Holding AG

- Sanofi

- Takeda Pharmaceutical Company Ltd.

Prostate Cancer Treatment Industry Developments

- In March 2022, the US FDA approved 177Lu-PSMA-617, a targeted radiotherapy for metastatic prostate cancer, offering improved treatment options for patients with advanced disease resistant to conventional therapies.

- In August 2024, Johnson & Johnson announced positive data from a Phase 3 clinical trial evaluating a new combination therapy for advanced prostate cancer, showcasing its ongoing commitment to developing innovative treatment solutions.

Prostate Cancer Treatment Market Segmentation

By Drug Class Outlook

- Hormonal Therapy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Others

By Distribution Channel Outlook

- Hospital Pharmacies

- Drug Stores & Retail Pharmacies

- Online Pharmacies

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Prostate Cancer Treatment Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 14.01 billion |

|

Market Size Value in 2025 |

USD 15.17 billion |

|

Revenue Forecast by 2034 |

USD 31.60 billion |

|

CAGR |

8.5% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy:

The prostate cancer treatment market has been segmented into detailed segments of drug class and distribution channels. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy:

The prostate cancer treatment market growth and marketing strategy focuses on expanding therapeutic portfolios through research and development, strategic partnerships, and clinical trials to introduce innovative therapies. Companies are emphasizing personalized medicine and biomarker-driven treatments to address specific patient needs. Direct engagement with healthcare professionals through educational initiatives and awareness campaigns enhances market penetration. Additionally, the adoption of digital marketing strategies, including telemedicine platforms and e-prescription systems, supports patient accessibility and strengthens brand visibility. These approaches are complemented by collaborations with healthcare providers to streamline treatment adoption.

FAQ's

The prostate cancer treatment market size was valued at USD 14.01 billion in 2024 and is projected to grow to USD 31.60 billion by 2034

The market is projected to register a CAGR of 8.5% during the forecast period

North America held the largest share of the market in 2024.

The prostate cancer treatment market includes active participation from companies such as Astellas Pharma Inc., AstraZeneca plc, Bayer AG, Bristol-Myers Squibb Company, F. Hoffmann-La Roche AG, Ferring Pharmaceuticals Inc., GlaxoSmithKline plc, Ipsen Pharma, Johnson & Johnson, Pfizer Inc., Sanofi, Amgen Inc., Dendreon Pharmaceuticals LLC, Endo Pharmaceuticals Inc., and Takeda Pharmaceutical Company Ltd.

The hormonal therapy segment accounted for the largest share of the market in 2024.

The hospital pharmacies segment accounted for the largest share of the market in 2024.

Prostate cancer treatment refers to the medical interventions used to manage and cure prostate cancer, a type of cancer that occurs in the prostate, a small gland in the male reproductive system. Treatment options vary based on the cancer's stage, grade, and the patient's overall health. Common treatments include surgery to remove the prostate (prostatectomy), radiation therapy, hormonal therapy to block the production or action of male hormones (androgens), chemotherapy, immunotherapy, and targeted therapies. In advanced stages, treatments such as targeted therapy, which focuses on specific cancer cell markers, and radiopharmaceuticals, used to target cancer cells with radiation, are employed. The aim of prostate cancer treatment is to eliminate the cancer or control its growth, alleviate symptoms, and improve the life quality for patients.

A few key trends in the market are described below: Shift Toward Personalized Medicine: Increasing focus on precision medicine, where treatments are tailored based on genetic profiles and biomarkers. Advancements in Immunotherapy: Growing use of immunotherapies, such as checkpoint inhibitors, to stimulate the body’s immune system to target prostate cancer cells. Adoption of Minimally Invasive Procedures: Rising adoption of less invasive surgical and radiation techniques, improving recovery times and reducing complications. Use of Combination Therapies: Growing trend of combining different treatment modalities, such as hormonal therapy with chemotherapy or immunotherapy, to improve outcomes.

For a new company entering the prostate cancer treatment market, focusing on personalized medicine and biomarker-driven treatments could provide a competitive edge. By developing therapies tailored to individual genetic profiles, the company can address the growing demand for precision oncology. Additionally, exploring novel immunotherapies, radiopharmaceuticals, or combination therapies presents significant growth opportunities, as these treatment modalities are gaining traction in advanced-stage prostate cancer. Leveraging digital health platforms for patient engagement and treatment adherence can also enhance market presence. As the market continues to grow due to increasing prostate cancer incidence, improved diagnostics, and advancements in therapeutic options, focusing on these areas can help a new company stay ahead of the competition.

Companies manufacturing, distributing, or purchasing prostate cancer treatment-related products and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved