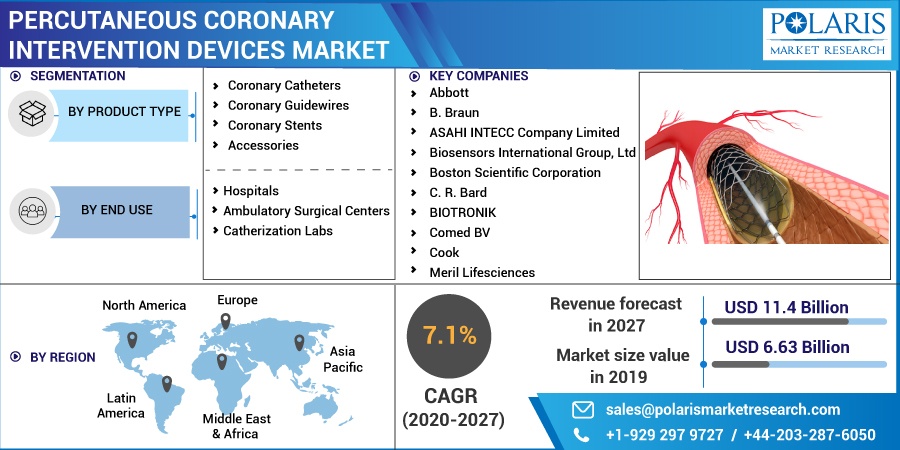

Percutaneous Coronary Intervention (PCI) Devices Market Share, Size, Trends, Industry Analysis Report, By Product (Coronary Catheters, Coronary Guidewires, Coronary Stents, and Accessories); By End Use (Hospitals, Ambulatory Surgical Centers, and Catherization Labs); By Regions; Segment Forecast, 2020 –2027

- Published Date:Jul-2020

- Pages: 107

- Format: PDF

- Report ID: PM1695

- Base Year: 2019

- Historical Data: 2016-2018

Report Outlook

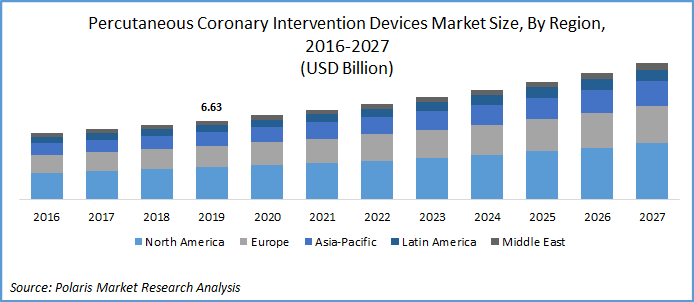

The global percutaneous coronary intervention (PCI) devices market was valued at USD 6.63 billion in 2019 and is expected to grow at a CAGR of 7.1% during the forecast period. The growth of the market is attributed to the increasing technological advances, new product launches, unhealthy lifestyle habits and high prevalence of Coronary artery disease (CAD).

Rapid shift towards MI techniques such as PCI procedures which are used to treat CAD conditions is significantly gaining prominence by the physicians. Also, an increase in obese and geriatric population positively drives the market as they are most prone to cardiac diseases. Adding to the high-risk factors also includes diabetes and sedentary life style habits which increase the PCI procedures. As they cause heart diseases, stroke and many other complications.

Know more about this report: request for sample pages

Industry Dynamics

Growth Drivers

Coronary artery disease is the most common heart disease affecting millions of people globally. Coronary artery disease (CAD) is usually caused due to the development of the plaque on the walls of the arteries that carries blood to the heart (coronary arteries). It blocks the carrying blood vessel, which results in unevenness in blood flow, through partial narrowing of those arteries, also known as atherosclerosis. The incidence of CAD is high income countries is increased due to faulty lifestyles, high fat diet, excessive consumption of alcohol and smoking.

Know more about this report: request for sample pages

Know more about this report: request for sample pages

The acute coronary syndrome includes unstable angina and heart attack. Angina which is the major symptom of the CAD includes chest pain and discomfort. As per CDC estimation of 2.7 to 6.1 million people in the U.S. have atrial fibrillation (AFib). More than 750,000 hospitalizations occur each year and contribute to an estimated death of 130,000 each year.

Globally, millions of people have one or more risk factors for the heart disease such as high blood pressure smoking and high cholesterol. For instance, according to CDC about 30.3 million in the US have diabetes that is 9.4% of the US population. such as drastic number of diseased populations could potentially fuel the use of PCI procedures which are used to treat the CAD.

Also, coronary heart disease forms the second leading cause of cardiovascular deaths in the Chinese population accounting for 23 per cent of deaths in urban areas while 14 per cent of deaths in the rural areas. There are approximately 3 million deaths due to CVD every year accounting for 41 per cent of the total deaths in China.

Also, about 2.4 million people in Canada aged 20 years above live with ischemic heart disease. The heart diseases stand second place in Canada claiming more than 48500 lives in 2012. Also, every 7 minutes CVD kills one person in Canada. Likewise, in the European region CVD causes more than half of the deaths. The disease burden of CVD in the European region is more than AIDS, Tuberculosis and malaria combined. Factors such as globalization, urbanizations, diabetes, alcohol tobacco and inactivity contribute to the growing number of CAD diseases. Thus, increasing in incidence of the coronary heart diseases increase the adoption of PCI procedures thus fueling the percutaneous coronary interventions devices market.

Challenges

The global market is hindered with few side effects associated with coronary intervention devices and accessories. The common challenges that occurred during the procedure include allergies to local anesthesia, adverse reactions to the contrast media in use, and complications during cardiac catheterization. During cardiac catheterization, the possible complications are bleeding, infection, and pain at the insertion site. Further potential damage might occur when the catheter pokes a hole in the blood vessels.

Percutaneous Coronary Intervention Devices Market Report Scope

The market is primarily segmented on the basis of Product, By End Use, and Geographic region.

|

By Product |

By End Use |

By Region |

|

|

|

Know more about this report: request for sample pages

Insight by Product

Based upon product, global PCI Devices market is categorized into coronary catheters, coronary guidewires, coronary stents, and accessories. The coronary stent segment accounted for the majority of the share. The factors responsible for its high share are its high usage in heart related procedures, consumer preference towards minimally invasive surgeries, and technological advancements in the product category. The segment is expected to remain dominant over the study period, owing to continuous innovation in the product by the manufacturers possessing efficient clinical outcomes.

Insight by End Use

On the basis of end use, the global market is categorized into hospitals, catherization labs, and ambulatory surgical centers. In 2019, hospital segment held the largest share, owing to the higher patient admissions coming for the surgical procedures. These hospitals have advanced technologies, supporting MI procedures, trained professionals, and advanced robotic devices performing PCI techniques.

Moreover, hospitals are equipped with advanced diagnostic and therapeutic systems which help in accurate diagnosis and treatment of the disease, tie-up with reimbursement authorities such as Medicare and Medicaid policies, regulatory authorities, and the constant pressure of reducing cost by Affordable care act (ACT) increases the utilization of the hospitals.

Geographic Overview

Geographically, the global PCI Devices market is bifurcated into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa (MEA). North America region is the largest revenue contributor followed by Europe and the Asia Pacific regions. In 2019, the North America region accounted for more than % of the global market. The US and Canada were the major revenue contributor. According to CDC statistics, one out of four deaths in the U.S. is due to heart diseases. Physicians are performing approximately 300,000 balloon angioplasty procedures annually in the US. Unhealthy habits, high elevated blood pressure with cholesterol increase the risk of heart attacks/stroke. CDC states that in every 40 seconds someone in the US suffers with heart attack. The high incidence rate of CAD fuels the percutaneous coronary interventions devices market in the Americas.

The growth of the market in the region is influenced by the growing number of technological advancements, players focusing on R&D to design novel products which cater to the requirements of the physicians. The increasing number of Food and Drug Administration (FDA) approvals, the launch of third generation stents significantly impact the market. As the new generation stents proven to show fewer side effects and improved clinical outcomes with less chance of restenosis.

Japan, India, South Korea, and China are the top three revenue generators in the APAC regions. With the high incidence of CAD, increased volume of PCI procedures coupled with contributing factors such as diabetes, obesity, sedentary life styles spur the market growth. Also increased awareness of MI PCI procedures in these countries significantly contribute to the market growth.

With the rapid urbanization of many developing countries and the increase in the disposable income of the people lead to change in the lifestyles such as smoking, excessive alcohol use and unhealthy habit thus increasing the risk of CAD.

Competitive Insight

Key players in the market are Abbott, B. Braun, ASAHI INTECC Company Limited, Biosensors International Group, Ltd, Boston Scientific Corporation, C. R. Bard, BIOTRONIK, Comed BV, Cook, Meril Lifesciences, Cordis, Medtronic PLC, Merit Medical System, and Terumo Corporation.

© 2025 Polaris Market Research and Consulting. All rights reserved