Ovarian Cancer Market Size, Share, Trends, Industry Analysis Report: By Type (Epithelial Ovarian Cancer, Germ Cell Ovarian Cancer, and Stromal Cell Ovarian Cancer), Treatment Type, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Apr-2025

- Pages: 118

- Format: PDF

- Report ID: PM1369

- Base Year: 2024

- Historical Data: 2020-2023

Ovarian Cancer Market Overview

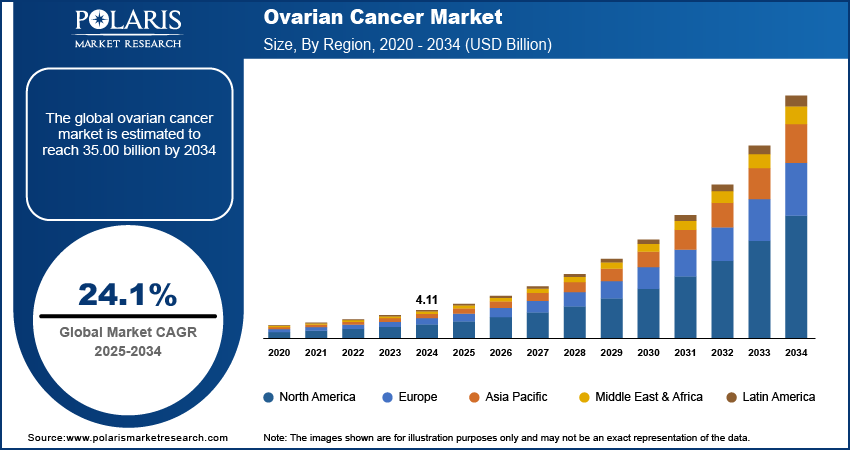

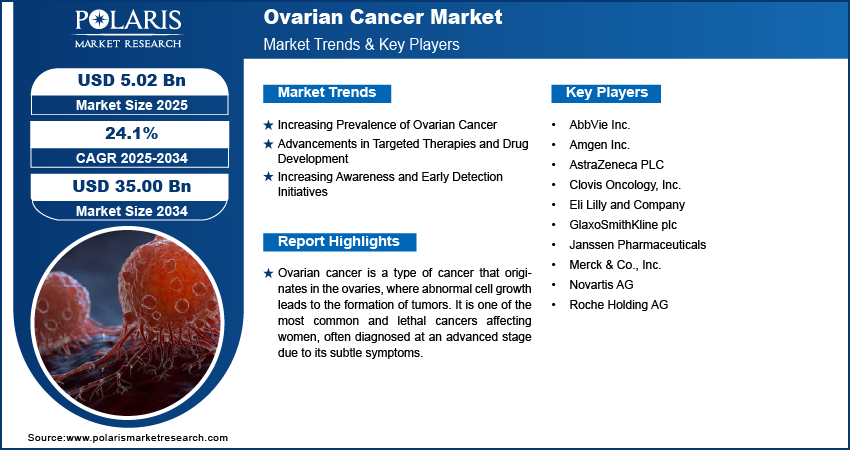

The ovarian cancer market size was valued at USD 4.11 billion in 2024. The market is projected to grow from USD 5.02 billion in 2025 to USD 35.00 billion by 2034, exhibiting a CAGR of 24.1% during 2025–2034.

The ovarian cancer market comprises diagnostics, therapeutics, and supportive care aimed at managing and treating ovarian malignancies. Key market drivers include the rising prevalence of ovarian cancer, advancements in targeted therapies, and increasing awareness initiatives for early detection. The demand for personalized medicine and biomarker-based diagnostics is also contributing to market growth. Notable ovarian cancer market trends include the expansion of immunotherapy applications, the development of poly (ADP-ribose) polymerase (PARP) inhibitors, and ongoing clinical trials evaluating novel treatment approaches. Additionally, regulatory approvals for innovative drugs and combination therapies are expected to support market expansion.

To Understand More About this Research: Request a Free Sample Report

Ovarian Cancer Market Dynamics

Increasing Prevalence of Ovarian Cancer

The rising incidence of ovarian cancer is significantly driving the ovarian cancer market growth. According to the World Cancer Research Fund, ovarian cancer was the eighth most common cancer in women globally, with approximately 313,000 new cases diagnosed in 2020. The increasing prevalence is attributed to factors such as aging populations, genetic predisposition, and lifestyle-related risks, including obesity and hormone replacement therapy. The growing patient pool is leading to higher demand for advanced diagnostic tools and effective treatment options, driving market expansion.

Advancements in Targeted Therapies and Drug Development

The development of targeted therapies, particularly poly (ADP-ribose) polymerase (PARP) inhibitors and angiogenesis inhibitors, has transformed the ovarian cancer treatment market development. PARP inhibitors, such as olaparib and niraparib, have demonstrated efficacy in patients having BRCA mutations, significantly improving progression-free survival. The US Food and Drug Administration (FDA) has approved multiple PARP inhibitors, expanding treatment options for both first-line and recurrent ovarian cancer cases. Additionally, ongoing research into immunotherapy and combination regimens is expected to enhance treatment effectiveness further, increasing adoption rates in clinical practice.

Increasing Awareness and Early Detection Initiatives

Efforts to improve early diagnosis through awareness programs and screening advancements are positively influencing ovarian cancer market opportunities. Organizations such as the Ovarian Cancer Research Alliance (OCRA) and the World Ovarian Cancer Coalition promote awareness campaigns to educate women on early symptoms and risk factors. Additionally, advancements in biomarker-based diagnostics, such as CA-125 and HE4 blood tests, along with the development of multi-modal screening approaches, are improving early detection rates. Early-stage diagnosis significantly improves survival outcomes, increasing the demand for screening technologies and targeted treatment solutions.

Ovarian Cancer Market Segment Insights

Ovarian Cancer Market Outlook by Type

The ovarian cancer market, by type, is segmented into epithelial ovarian cancer, germ cell ovarian cancer, and stromal cell ovarian cancer. The epithelial ovarian cancer segment dominated the market share in 2024. This subtype originates from the epithelial cells lining the ovary and is often diagnosed at an advanced stage due to the lack of early symptoms. The high prevalence and late-stage detection drive the demand for advanced diagnostic tools, targeted therapies, and combination treatment approaches. Poly (ADP-ribose) polymerase (PARP) inhibitors and angiogenesis inhibitors are widely used in the treatment of epithelial ovarian cancer, with ongoing clinical trials exploring new therapeutic strategies to improve patient outcomes.

Ovarian Cancer Market Evaluation by Treatment Type

The ovarian cancer market, by treatment type, is segmented into immunotherapy, chemotherapy, targeted therapy, surgery, and others. Chemotherapy accounted for a major ovarian cancer market share in 2024 due to its established role in both first-line and recurrent disease management. Platinum-based chemotherapy, particularly carboplatin and paclitaxel, is the standard treatment regimen, often used in combination with targeted therapies. Despite the emergence of newer treatment modalities, chemotherapy continues to be a primary approach due to its broad applicability across different ovarian cancer subtypes and stages. However, resistance to chemotherapy in recurrent cases has led to increasing research efforts focused on enhancing treatment efficacy through combination therapies and novel drug formulations.

The targeted therapy segment is the fastest-growing segment, driven by the increasing adoption of poly (ADP-ribose) polymerase (PARP) inhibitors and angiogenesis inhibitors. PARP inhibitors, such as olaparib and rucaparib, have significantly improved progression-free survival in patients with BRCA mutations, leading to increased regulatory approvals and broader clinical use. Additionally, angiogenesis inhibitors such as bevacizumab are being integrated into treatment regimens to enhance therapeutic outcomes. Ongoing research into combination strategies, including the use of targeted therapies with immunotherapy and chemotherapy, is further driving the segment’s growth, contributing to the evolution of ovarian cancer treatment approaches.

Ovarian Cancer Market Assessment by End User

The ovarian cancer market, by end user, is segmented into hospitals, homecare, specialty centers, and others. The hospitals segment held the largest market share in 2024, as they are the primary settings for the administration of chemotherapy, targeted therapies, and surgical interventions. The availability of advanced medical infrastructure, specialized oncology departments, and multidisciplinary teams in hospitals makes them the preferred choice for ovarian cancer patients. Additionally, the rising number of advanced treatment options and complex procedures, including surgery and combination therapies, further supports the dominance of the hospitals segment. These facilities also play a key role in clinical trials, which contribute to the ongoing development of new therapeutic agents.

The specialty centers segment is witnessing the fastest growth due to the increasing focus on personalized medicine and the advancement of specialized cancer care. These centers offer more focused treatments, including cancer immunotherapy and targeted therapies, which are increasingly in demand as treatment options for ovarian cancer evolve. Specialty centers are becoming more prominent in the healthcare landscape with the rising prevalence of ovarian cancer and the growing adoption of precision medicine. Their ability to provide tailored, advanced treatments and specialized care is driving the segment's rapid expansion.

Ovarian Cancer Market by Regional Outlook

By region, the report provides ovarian cancer market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the ovarian cancer market revenue share in 2024 due to the high incidence of ovarian cancer, advanced healthcare infrastructure, and the availability of innovative treatment options. The region benefits from strong research and development capabilities, regulatory support for new therapies, and a well-established healthcare system, facilitating the rapid adoption of targeted therapies, immunotherapies, and precision medicine. Additionally, the presence of key pharmaceutical and biotechnology companies in the US accelerated ovarian cancer market growth. The growing awareness around ovarian cancer and early detection also contributes to the region's dominance in the global market.

Europe holds a significant share of the ovarian cancer market due to the region's advanced healthcare systems, strong research infrastructure, and increasing adoption of targeted therapies and immunotherapies. The European Union (EU) has established robust cancer care frameworks, which have led to improved early detection and treatment outcomes. Countries such as Germany, the UK, and France have seen a rise in personalized medicine approaches, driving the demand for specialized treatments. Furthermore, ongoing clinical trials and the approval of novel therapies, including PARP inhibitors, are contributing to market growth in the region.

The Asia Pacific ovarian cancer market is witnessing rapid growth, driven by improving healthcare infrastructure, rising awareness, and increasing cancer incidences. Countries such as Japan, China, and India are experiencing an increase in ovarian cancer diagnoses, attributed to both lifestyle factors and better detection capabilities. The demand for advanced treatments, including chemotherapy and targeted therapies, is increasing, with a focus on expanding access to novel therapies. Government initiatives and healthcare improvements are expected to drive the Asia Pacific ovarian cancer market expansion. Additionally, the rising burden of cancer in this region highlights the growing need for effective therapies and advanced treatment options.

Ovarian Cancer Market – Key Players and Competitive Analysis Report

A few key players in the ovarian cancer market include Bristol-Myers Squibb Company; AstraZeneca PLC; Roche Holding AG; Merck & Co., Inc.; GlaxoSmithKline plc; Eli Lilly and Company; Pfizer Inc.; Novartis AG; AbbVie Inc.; Amgen Inc.; Clovis Oncology, Inc.; Gilead Sciences, Inc.; Sanofi S.A.; Teva Pharmaceutical Industries Ltd.; and Bayer AG. These companies are actively involved in the development, production, and distribution of therapies for ovarian cancer, including chemotherapy, targeted therapies, and immunotherapies. They offer a range of treatment options from first-line to advanced therapies, with a focus on personalized medicine and biomarker-driven approaches to improve patient outcomes.

In terms of competitive positioning, companies such as AstraZeneca PLC and Bristol-Myers Squibb Company are making notable strides with targeted therapies such as PARP inhibitors, which have become crucial in the treatment of ovarian cancer. AstraZeneca PLC, with its Olaparib (Lynparza), and Bristol-Myers Squibb Company, with Rucaparib (Rubraca), are expanding their presence in this market by offering new therapies that address specific genetic mutations. Meanwhile, Merck & Co., Inc. is pushing the development of immunotherapy treatments, which adds a new dimension to ovarian cancer treatment. Companies such as Pfizer Inc. and Gilead Sciences, Inc. are focusing on expanding their portfolios to include targeted therapies as well, capitalizing on new breakthroughs and clinical trials to maintain competitive advantages.

The competitive landscape is driven by research and innovation, as players in the market are focusing on improving treatment efficacy, reducing side effects, and addressing unmet needs in ovarian cancer care. Ongoing clinical trials and the approval of new drugs will continue to shape the market dynamics, as more personalized treatment options are becoming available. Strategic collaborations and partnerships between pharmaceutical companies and research organizations are essential to stay ahead in the development of novel therapies. Companies also aim to expand their market presence by enhancing their distribution networks, improving patient access to therapies, and investing in global outreach programs to address the growing global cancer burden.

AstraZeneca PLC is an international pharmaceutical company committed to the discovery, development, and commercialization of prescription medicines. The company operates in various therapeutic areas, including oncology, cardiovascular, and respiratory diseases. AstraZeneca has a significant presence in the oncology market, offering treatments for various cancers, including ovarian cancer.

AbbVie Inc., a global biopharmaceutical company, has significantly expanded its oncology portfolio by acquiring ImmunoGen in 2023, bringing Elahere (mirvetuximab soravtansine) into its offerings. Elahere is an antibody-drug conjugate targeting folate receptor-alpha (FRα), approved for treating FRα-positive, platinum-resistant ovarian cancer. Clinical trials have demonstrated that Elahere reduces the risk of death by 32% compared to chemotherapy, with a median overall survival of nearly 17 months. AbbVie continues to explore Elahere's potential in other cancer indications, reinforcing its commitment to advancing targeted cancer therapies.

List of Key Companies in Ovarian Cancer Market

- AbbVie Inc.

- Amgen Inc.

- AstraZeneca PLC

- Clovis Oncology, Inc.

- Eli Lilly and Company

- GlaxoSmithKline plc

- Janssen Pharmaceuticals

- Merck & Co., Inc.

- Novartis AG

- Roche Holding AG

Ovarian Cancer Industry Developments

- November 2024: Wistar Institute researchers discovered a new combination therapy approach for metastatic ovarian cancer.

Ovarian Cancer Market Segmentation

By Type Outlook (Revenue – USD Billion, 2020–2034)

- Epithelial Ovarian Cancer

- Germ Cell Ovarian Cancer

- Stromal Cell Ovarian Cancer

By Treatment Type Outlook (Revenue – USD Billion, 2020–2034)

- Immunotherapy

- Chemotherapy

- Targeted Therapy

- Surgery

- Others

By End User Outlook (Revenue – USD Billion, 2020–2034)

- Hospitals

- Homecare

- Speciality Centre

- Others

By Regional Outlook (Revenue – USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Ovarian Cancer Market Report Scope

|

Report Attributes |

Details |

|

Market Size in 2024 |

USD 4.11 billion |

|

Market Value in 2025 |

USD 5.02 billion |

|

Revenue Forecast by 2034 |

USD 35.00 billion |

|

CAGR |

24.1% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy: The ovarian cancer market has been segmented into detailed segments of type, treatment type, and end user. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy: The ovarian cancer market growth and marketing strategies focus on expanding access to innovative therapies and enhancing awareness around early detection. Key players are investing in research and development to introduce novel treatments, including targeted therapies and immunotherapies, which have shown promising results. Strategic partnerships and collaborations with research organizations and healthcare providers are increasingly common to accelerate the development and distribution of therapies. Additionally, companies are focusing on improving patient access through pricing strategies, expanding into emerging markets, and increasing awareness through advocacy programs and educational campaigns. Personalized medicine and the integration of biomarker-driven treatments are also playing a crucial role in shaping market growth.

FAQ's

The ovarian cancer market size was valued at USD 4.11 billion in 2024 and is projected to grow to USD 35.00 billion by 2034.

The market is projected to register a CAGR of 24.1% during 2025–2034.

\North America held the largest share of the market in 2024.

A few key players in the ovarian cancer market include Bristol-Myers Squibb Company; AstraZeneca PLC; Roche Holding AG; Merck & Co., Inc.; GlaxoSmithKline plc; Eli Lilly and Company; Pfizer Inc.; Novartis AG; AbbVie Inc.; Amgen Inc.; Clovis Oncology, Inc.; Gilead Sciences, Inc.; Sanofi S.A.; Teva Pharmaceutical Industries Ltd.; and Bayer AG.

The epithelial ovarian cancer segment accounted for the largest share of the market in 2024.

The chemotherapy segment accounted for the largest share of the market in 2024

Ovarian cancer is a type of cancer that begins in the ovaries, which are the reproductive organs responsible for producing eggs and hormones like estrogen and progesterone. The disease typically develops when abnormal cells in the ovaries begin to grow uncontrollably and form a tumor. Ovarian cancer can be categorized into several types, with epithelial ovarian cancer being the most common. Symptoms may include bloating, pelvic pain, and changes in bowel habits, but they often go unnoticed in the early stages, making early detection challenging. Ovarian cancer can spread to other parts of the body, and treatment usually involves surgery, chemotherapy, and targeted therapies.

A few key trends in the market are described below: Increased Focus on Targeted Therapies: Growing adoption of therapies such as PARP inhibitors and angiogenesis inhibitors for more effective treatment. Advancements in Immunotherapy: Rising interest in immune checkpoint inhibitors and other immunotherapy options as potential treatments for ovarian cancer. Personalized Medicine: Shift toward personalized treatments based on genetic testing and biomarkers to tailor therapies to individual patient profiles. Rising Awareness and Early Detection: More initiatives focusing on early detection and increasing public awareness about ovarian cancer symptoms and risk factors.

A new company entering the ovarian cancer market must focus on innovative areas such as personalized medicine and biomarker-driven treatments, which are increasingly in demand for more targeted and effective therapies. Investing in research for novel drug formulations or delivery systems, particularly in immunotherapy or combination therapies, could provide a competitive edge. Additionally, developing affordable diagnostic tools for early detection could address a significant unmet need. Establishing partnerships with research organizations, expanding into emerging markets, and leveraging digital health technologies for patient monitoring and support are also strategic approaches to stay ahead in a rapidly evolving market.

Companies manufacturing, distributing, or purchasing ovarian cancer therapy and diagnosis-related products and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved