Military Vetronics Market Share, Size, Trends, Industry Analysis Report By Platform (Homeland Security, Military); By Vehicle Type; By System; By Region; Segment Forecast, 2024 - 2032

- Published Date:Jan-2024

- Pages: 118

- Format: PDF

- Report ID: PM3212

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

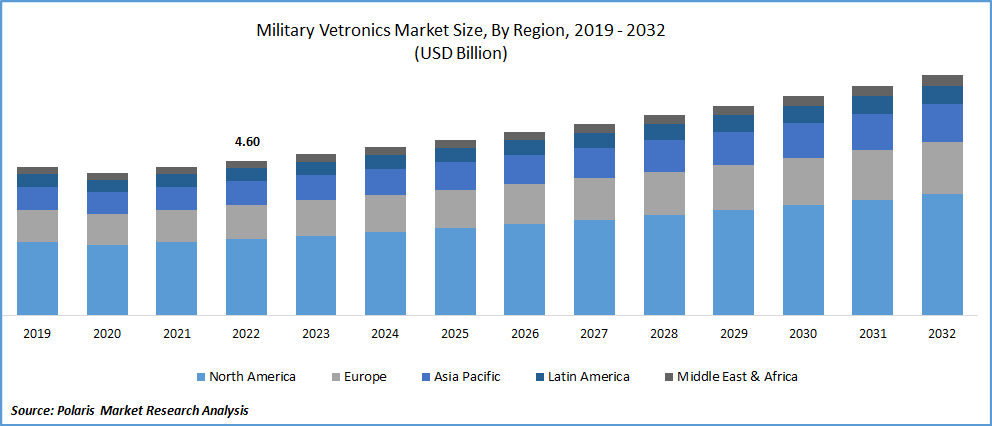

The global military vetronics market was valued at USD 4.79 billion in 2023 and is expected to grow at a CAGR of 4.5% during the forecast period. Redundant vetronics system includes a strong hardware and software interface to support the necessary operations. Systems for military robotics can be retrofitted or fitted directly. In line fit, a set of military vehicles from a manufacturer are equipped with their pre-selected vetronics systems; in retrofit, the vetronics systems are installed in the aftermarket. Expanding commercial prospects are anticipated as demand for open military vetronics with an open architecture to support single system many types of vehicles rises.

Know more about this report: Request for sample pages

The military and defense services' increased emphasis on improving situational awareness is also boosting the military vetronics market expansion. Vetronics are being widely used to enhance inter- and intra-vehicle communications, surveillance, and navigation because of growing geopolitical upheaval, cross-border security concerns, and border crossing incidents. A beneficial effect on the market is also being produced by several technological developments, such as the rise of wireless communications technology and the upgrading of military vehicles unmanned vehicles (UMV) and drones are employed for commercial objectives including taking pictures and films of athletic events and cityscapes, as well as for surveillance purposes.

The availability of affordable components and rising government spending on defense are two further factors that are anticipated to fuel market growth. In September 2022, The United States Department of Defense (DoD) is pushing for a modular open systems approach (MOSA) in updates and new designs.

Vetronics systems are becoming increasingly focused on C4ISR [command, control, communications, computers, intelligence, surveillance, and reconnaissance], compatibility with other battlefield components and the potential to be unmanned if needed. C4ISR funding is substantial in the Army and has a direct impact on ground vehicles. Analysts estimate that the Army will spend $9 billion in 2021, with funding growing at a similar rate in 2022, with $6 billion invested.

For instance, in February 2020, the SCORPION military modernization program will get a $12 billion investment from the French Army, according to its plans. The program calls for the upgrade of current armored assets as well as the purchase of new armored vehicles. Another illustration is the Franco-German Major Ground Combat System (MGCS), a collaborative initiative to create main combat tanks that will replace the Leopard 2 and Leclerc in Germany and France, respectively, by 2035. As a result, the market is expanding due to the purchase of new vehicles as well as the upgrade of current armored vehicles.

The broader military business as well as the vetronics industry have suffered as a result of the COVID-19 epidemic. The pandemic's widespread breakout, constrained company operations, and logistical assistance, and the budget's diversion toward managing medical emergencies reduced the market's chances for growth.

However, the increase in geopolitical tensions between different countries has given the vetronics market growth a long-term boost. Countries in Asia-Pacific and North America are more likely to increase and modernize their military fleets to ensure that they are prepared for warfare in the upcoming years. These elements are anticipated to bolster the market expansion.

Industry Dynamics

Growth Drivers

Increasing data management and work bandwidth required for successful military operations can no longer be handled by redundant vetronics systems. In addition, highly efficient, technologically advanced electronic systems that make use of cloud computing are susceptible to cyber-attacks. To maintain smooth operation, the new car electronics system frequently communicates data and information with the central hub via cloud platforms. An excellent possibility for hackers to intercept or manipulate information exists due to constant data interchange.

Further, in November 2022, VR simulation firm VRAI announced a partnership with Microsoft to offer next-generation simulations to military end users through a product that leverages VR, ML, and the Microsoft Azure’s cloud platform. The VRAI ReACT tool is designed to expand training & repetition chances for soldiers by replacing the requirement for the platforms with immersive VR surroundings. The market for military vetronics is significantly challenged by such tactics.

Report Segmentation

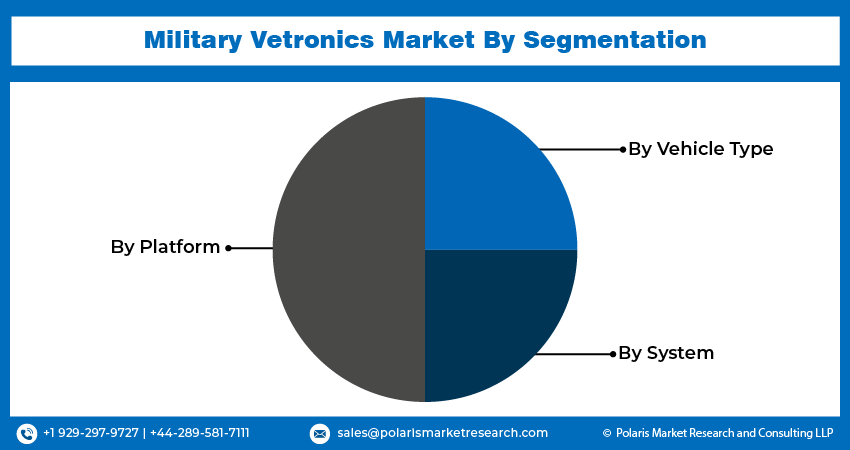

The market is primarily segmented based on platform, vehicle type, system, and region.

|

By Platform |

By Vehicle Type |

By System |

By Region |

|

|

|

|

Know more about this report: Request for sample pages

The Command & Communication Installation Segment is Expected to Witness the Fastest Growth

The segment growth is predicted to be aided by the growing need for sophisticated communication and navigation systems for real-time data on the battlefield. Modern warfare is heavily reliant on technology, and good communication increases the interoperability and success rate of military missions, spurring industry expansion. During the anticipated time, the command, control, and computer system (C4 System) segment will experience significant expansion. Combat vehicles may grow and rearrange parts on the fly owing to command and control systems. These devices lessen the time, money, and risks involved in disassembling a vehicle.

The Light Combat Vehicles Segment is Expected to Hold the Significant Revenue Share

Light-protected vehicle market is anticipated to grow at a faster rate. Another factor contributing to the growing popularity of light-protected vehicles is their ability to be updated to perform a particular task. Due to growing domestic security concerns and the increasing demand for unmanned vehicles to protect military forces from losing their lives, the unmanned ground vehicles market is predicted to hold a sizeable market share in terms of value and consumption.

The Demand in North America is Expected to Witness Significant Growth

The regional growth is attributable to rising defense spending by the American government for the acquisition of cutting-edge vehicles as well as expanding investments in the modernization of the current fleet of American military vehicles. Over the past few years, it has been crucial in the United States to swiftly integrate electronic information and command systems into military vehicles. These systems are now networked and communicate with ground troops as well as among themselves and on the same platform.

For instance, in August 2021, US Army land warfare experts chose five military companies to produce the next-generation rapid armored combat vehicles and vetronics architects for the Army M2 Bradley Fighting Vehicle replacement. In addition, the US Army announced five contracts worth a combined USD 26.6 million for the optionally manned fighting vehicle's phase-two concept design (OMFV). Such changes could accelerate the market expansion of the nation.

Further, due to the escalating terrorist threats and cross-border disputes among Asia-Pacific nations, the region is anticipated to experience exponential growth during the projection period. Additionally, governments in the region are concentrating on boosting spending on military operations. For instance in June 2020, Under the Make in India initiative, the Indian Ministry of Defense announced the purchase of 156 BMP 2 infantry vehicles for the army.

Competitive Insight

Some of the major players operating in the global military vetronics market include BAE Systems, Curtiss-Wright Corporation, General Dynamics, Harris Corporation, Kongsberg Gruppen, Leonardo-Finmeccanica, Lockheed Martin Corporation, L3Harris Technologies, Oshkosh Corporation, Raytheon Company, Rheinmetall, Saab Group, & Thales Group.

Recent Developments

- In June 2021, Elbit has been selected by BAE Systems to provide vetronics sensors and active protection for a Swedish armored combat vehicle. The mid-1980s saw the development of the Swedish CV90, a tracked combat vehicle that saw service in Sweden.

Military Vetronics Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 5 billion |

|

Revenue forecast in 2032 |

USD 7.12 billion |

|

CAGR |

4.5% from 2024 - 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2023 |

|

Forecast period |

2024- 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments Covered |

By Platform, By Vehicle Type, By System, By Region |

|

Regional scope |

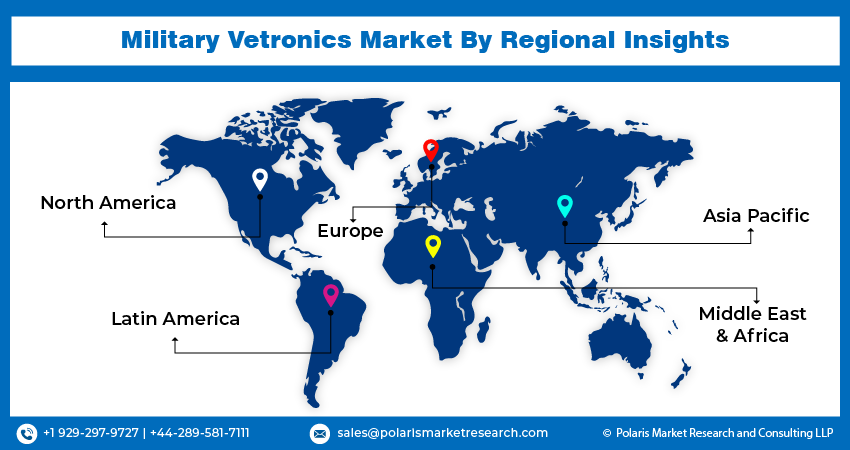

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Key Companies |

BAE Systems PLC, Curtiss-Wright Corporation, General Dynamics Corporation, Harris Corporation, Kongsberg Gruppen ASA, Leonardo-Finmeccanica S.P.A, Lockheed Martin Corporation, L3Harris Technologies, Inc, Oshkosh Corporation, Raytheon Company, Rheinmetall AG, Saab Group, and Thales Group. |

FAQ's

The global military vetronics market size is expected to reach USD 7.12 billion by 2032.

Key players in the military vetronics market are BAE Systems, Curtiss-Wright Corporation, General Dynamics, Harris Corporation, Kongsberg Gruppen, Leonardo-Finmeccanica, Lockheed Martin Corporation.

North America contribute notably towards the global military vetronics market.

The global military vetronics market expected to grow at a CAGR of 4.5% during the forecast period.

The military vetronics market report covering key segments are platform, vehicle type, system, and region.

© 2025 Polaris Market Research and Consulting. All rights reserved