Mesenchymal Stem Cells Market Size, Share, Trends, Industry Analysis Report: By Products and Services (Cell & Cell Lines, Consumables, and Services), Workflow, Type, Application, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Feb-2025

- Pages: 119

- Format: PDF

- Report ID: PM1565

- Base Year: 2024

- Historical Data: 2020-2023

Mesenchymal Stem Cells Market Overview

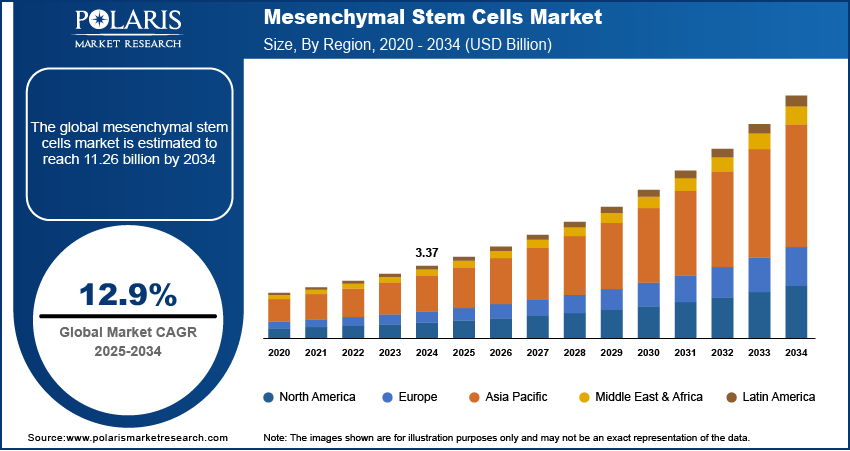

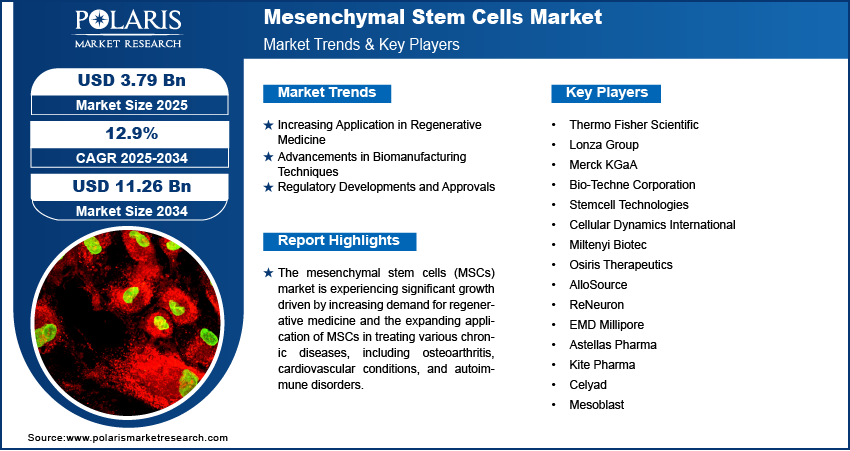

The mesenchymal stem cells market size was valued at USD 3.37 billion in 2024. The market is projected to grow from USD 3.79 billion in 2025 to USD 11.26 billion by 2034, exhibiting a CAGR of 12.9% during the forecast period.

The mesenchymal stem cells (MSCs) market focuses on the research, development, and commercialization of MSC-based therapies and applications. MSCs, derived from various tissues such as bone marrow, adipose tissue, and umbilical cord, are increasingly recognized for their potential in regenerative medicine, cell therapy, and tissue engineering. Key drivers of mesenchymal stem cells market growth include advancements in stem cell research, increasing demand for personalized medicine, and rising applications in treating conditions such as osteoarthritis, cardiovascular diseases, and autoimmune disorders. Additionally, trends such as the growing adoption of MSCs for drug discovery, tissue regeneration, and the use of biomanufacturing techniques are expected to further propel the market. However, challenges such as ethical concerns, regulatory hurdles, and high production costs may impact the market's progress.

To Understand More About this Research: Request a Free Sample Report

Mesenchymal Stem Cells Market Dynamics

Increasing Application in Regenerative Medicine

One of the most prominent mesenchymal stem cells (MSCs) market trends is their increasing application in regenerative medicine. MSCs have shown great potential in repairing and regenerating damaged tissues and organs, particularly in the treatment of osteoarthritis, cardiovascular diseases, and neurological disorders. The versatility of MSCs in differentiating into various cell types, such as bone, cartilage, and fat cells, has made them a focus of research in developing treatments for age-related diseases and tissue degeneration. A study published in Frontiers in Bioengineering and Biotechnology in 2022, highlights the growing interest in MSC-based therapies for orthopedic conditions, particularly osteoarthritis, where MSCs are used for tissue repair and reducing inflammation. This trend is supported by ongoing clinical trials and increasing funding for MSC research, driving their wider adoption in clinical practice.

Advancements in Biomanufacturing Techniques

Another significant trend in the MSC market is the advancement of biomanufacturing techniques that enable more efficient and scalable production of mesenchymal stem cells. As the demand for MSC-based therapies rises, manufacturers are investing in technologies that streamline the cell culture process, reduce production costs, and ensure consistency and quality in the final product. Techniques such as automated cell culture systems, bioreactors, and xeno-free culture media are helping to address challenges related to large-scale MSC production. The introduction of these advanced manufacturing platforms is expected to improve the overall commercial viability of MSC therapies. For example, a 2023 study from the Journal of Stem Cell Research & Therapy noted that automated systems for cell expansion and harvesting are increasing efficiency in MSC production, paving the way for cost-effective therapies. This trend is crucial in making MSC-based treatments more accessible and affordable for a broader patient population.

Regulatory Developments and Approvals

The regulatory landscape surrounding mesenchymal stem cells is evolving, with increasing efforts by global health authorities to establish clear guidelines and streamline approval processes for MSC-based therapies. Regulatory agencies such as the US FDA and the European Medicines Agency (EMA) are progressively defining the pathways for clinical trials and commercialization of stem cell products. Recent developments in regulatory frameworks, such as the FDA’s expanded use of “fast track” designations for cell therapies, have provided manufacturers with clearer routes to bring MSC-based treatments to market faster. In the European Union, the introduction of the Advanced Therapy Medicinal Products (ATMP) regulation has facilitated the development of stem cell-based medicines. These regulatory advancements are essential in supporting the MSC market growth by ensuring that products are safe and effective while meeting the increasing demand for stem cell therapies.

Mesenchymal Stem Cells Market Segment Insights

Mesenchymal Stem Cells Market Assessment by Products and Services

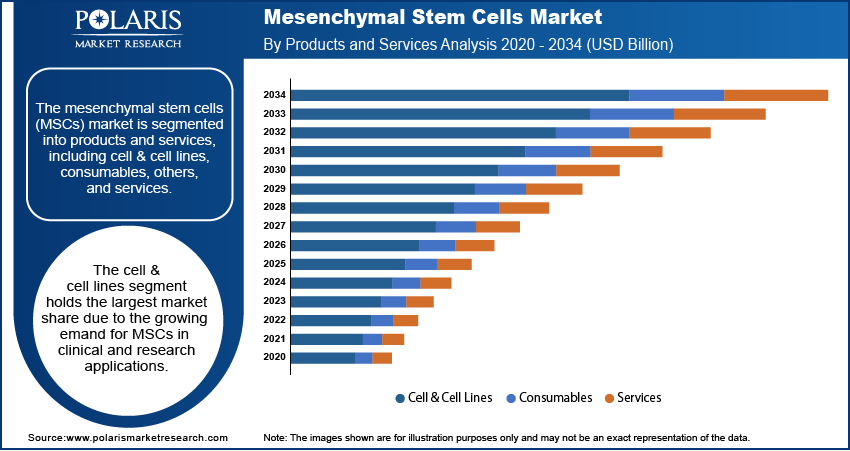

The mesenchymal stem cells market segmentation, based on products and services, includes cell & cell lines, consumables, and services. The cell & cell lines segment holds the largest market share due to the growing demand for MSCs in clinical and research applications. This segment is driven by the increasing use of MSCs for regenerative medicine and the development of cell-based therapies. As stem cell research continues to advance, the need for high-quality, scalable MSCs for clinical trials and therapeutic applications is expanding. Additionally, the increasing investment in regenerative medicine and the adoption of MSC-based therapies in clinical settings are boosting the demand for cell & cell lines. In terms of growth, the consumables segment is registering the highest growth, primarily due to the rising demand for media, reagents, and other consumables used in MSC cultivation and expansion. These consumables are crucial for maintaining optimal culture conditions and ensuring the quality and viability of MSCs during therapeutic procedures. The increasing number of MSC-based research initiatives and clinical trials is contributing to this growth, with consumables being essential for large-scale production and application.

The services segment, which includes research and clinical services related to MSC-based therapies, is also witnessing steady growth. Services provided by biotechnology companies and contract research organizations (CROs) for stem cell banking, genetic modification, and cell therapy development are in high demand as MSC applications continue to proliferate. As more hospitals and clinics integrate MSC-based treatments, service providers are being sought to support clinical applications and regulatory compliance.

Mesenchymal Stem Cells Market Evaluation by Workflow

The mesenchymal stem cells (MSCs) market is segmented based on workflow into cell sourcing & isolation, culture & cryopreservation, differentiation, and characterization. The culture & cryopreservation segment holds the largest market share, driven by the essential role these processes play in the production and storage of MSCs for therapeutic use. The growing demand for MSCs in clinical trials and regenerative medicine applications is contributing to the need for efficient culture methods and storage solutions that maintain cell viability over extended periods. Cryopreservation is particularly important for ensuring the long-term preservation of MSCs, enabling their widespread use in future treatments and clinical applications. Additionally, advancements in culture techniques, including the use of xeno-free media and automated bioreactors, are supporting the expansion of this segment.

The differentiation segment is also registering the fastest growth due to the increasing interest in MSCs for their ability to differentiate into a variety of cell types, making them suitable for a wide range of therapeutic applications, including tissue repair and regenerative treatments. This segment is fueled by ongoing research into harnessing MSCs for specific clinical indications, such as bone and cartilage regeneration, and their potential to address complex diseases. As MSC-based therapies evolve, the need for optimized differentiation protocols to direct stem cells toward desired cell lineages are driving growth in this market. The cell sourcing & isolation and characterization segments also contribute to the workflow but are not experiencing the same growth rates as differentiation. However, they remain critical for ensuring high-quality, functional MSCs for therapeutic use.

Mesenchymal Stem Cells Market Assessment by Type

The mesenchymal stem cells (MSCs) market is segmented by type into autologous and allogeneic MSCs. The autologous MSCs segment holds the largest mesenchymal stem cells market share, primarily driven by their use in personalized medicine. Autologous MSCs, derived from the patient’s tissues, offer significant advantages in terms of safety and reduced risk of immune rejection, making them a preferred choice for regenerative therapies, particularly in orthopedics, cardiovascular treatments, and autoimmune disorders. This segment's growth is also supported by the increasing number of clinical trials exploring the use of autologous MSCs in various therapeutic applications, contributing to their widespread adoption in clinical practice.

The allogeneic MSCs segment is also registering the fastest growth due to their potential for off-the-shelf availability, which provides a significant advantage over autologous cells in terms of scalability and cost-effectiveness. Allogeneic MSCs, sourced from healthy donors, are increasingly used in cell therapy products, as they can be manufactured in larger quantities and stored for future use, facilitating easier administration in emergency treatments or clinical settings with high patient turnover. This growth is driven by the expanding focus on developing allogeneic MSC therapies for conditions such as graft-versus-host disease (GVHD), inflammatory diseases, and other chronic disorders. As research advances, the acceptance of allogeneic MSCs in clinical applications is expected to increase, further driving market expansion.

Mesenchymal Stem Cells Market Evaluation by Application

The mesenchymal stem cells market segmentation, based on application, includes disease modeling, drug development & discovery, stem cell banking, tissue engineering, toxicology studies, and others. The drug development & discovery segment holds the largest market share, driven by the increasing use of MSCs for screening new drug candidates and for creating disease models that replicate human physiology. MSCs are particularly valuable in modeling diseases such as osteoarthritis, cardiovascular diseases, and autoimmune disorders, where they serve as platforms for understanding disease mechanisms and evaluating therapeutic efficacy. This application’s growth is also boosted by the rising demand for personalized medicine and the potential of MSCs to generate patient-specific disease models for more targeted drug development.

The tissue engineering segment is also registering the fastest growth, fueled by the expanding use of MSCs in regenerative medicine and organ/tissue repair. MSCs are being studied extensively for their ability to differentiate into various cell types, which is critical for applications in tissue repair, including cartilage, bone, and skin regeneration. As advancements in tissue engineering continue, the potential of MSCs to generate functional tissues for transplantation or healing is driving this segment’s growth. Additionally, stem cell banking and toxicology studies contribute to the market, with increasing investment in biobanking for future therapies and the use of MSCs for evaluating drug toxicity. However, the tissue engineering segment is expected to see the most significant expansion as MSC-based therapeutic applications continue to gain traction.

Mesenchymal Stem Cells Market Regional Insights

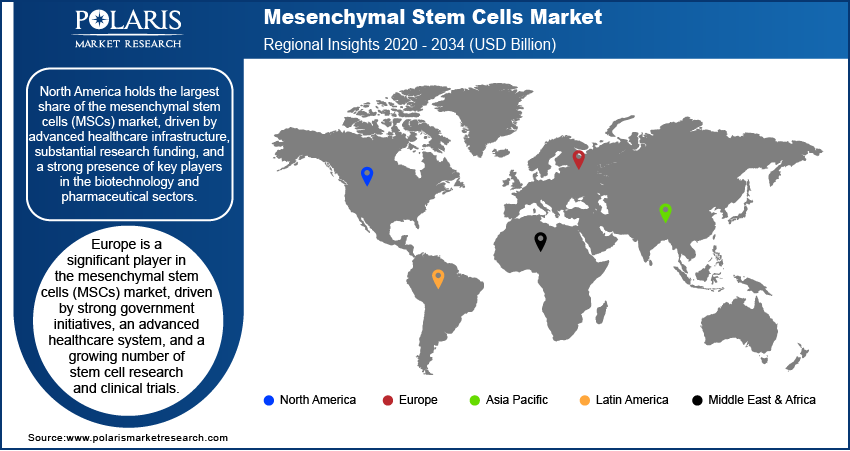

By region, the study provides mesenchymal stem cells market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest market share, driven by advanced healthcare infrastructure, substantial research funding, and a strong presence of key players in the biotechnology and pharmaceutical sectors. The region benefits from significant government and private investments in stem cell research and regenerative medicine alongside a well-established regulatory framework that supports the clinical development and commercialization of MSC-based therapies. The US, in particular, is a leader in MSC-related clinical trials and the adoption of innovative stem cell therapies for a wide range of diseases. Additionally, growing demand for personalized medicine, advancements in biomanufacturing technologies, and the increasing prevalence of chronic diseases contribute to North America's dominance in the market. Other regions, such as Europe and Asia Pacific, are also witnessing growth, but North America's robust healthcare system and regulatory support ensure it maintains the largest market share.

Europe is a significant player in the mesenchymal stem cells (MSCs) market, driven by strong government initiatives, an advanced healthcare system, and a growing number of stem cell research and clinical trials. The European Medicines Agency (EMA) has established regulatory frameworks for the approval of stem cell-based therapies, providing a supportive environment for MSC development and commercialization. Countries such as the UK, Germany, and France are at the forefront of stem cell research, with numerous academic institutions and biotechnology companies focusing on regenerative medicine. The rising demand for MSC therapies in regenerative applications, coupled with the increasing prevalence of chronic diseases and the aging population, is propelling market growth in Europe. However, regulatory and reimbursement challenges could impact the market's pace of expansion.

Asia Pacific is experiencing rapid growth in the MSCs market, driven by a combination of increasing healthcare investments, expanding clinical applications, and growing interest in regenerative medicine. Countries such as Japan, China, and South Korea are leading the region due to their advanced research infrastructure and government support for stem cell innovation. Japan's regulatory environment, including its approval of stem cell therapies, has created a favorable atmosphere for MSC-based treatments. Furthermore, the rising prevalence of age-related conditions and chronic diseases and the need for innovative medical solutions are boosting the adoption of MSC therapies in the region. Despite challenges such as regulatory hurdles and market fragmentation, Asia Pacific is expected to continue to see strong market growth as investments in healthcare and stem cell research intensify.

Mesenchymal Stem Cells Market – Key Market Players and Competitive Insights

Key players in the mesenchymal stem cells (MSCs) industry include companies such as Thermo Fisher Scientific, Lonza Group, Merck KGaA, Bio-Techne Corporation, and Stemcell Technologies. Other significant contributors include Cellular Dynamics International, Miltenyi Biotec, Osiris Therapeutics, AlloSource, and ReNeuron. Additionally, companies such as EMD Millipore, Astellas Pharma, Kite Pharma, Celyad, and Mesoblast are also active in the market. These companies are involved in the development, production, and commercialization of MSC-based products for clinical applications, research, and tissue engineering. Many of these companies have established strong research pipelines and partnerships with academic institutions and hospitals to further the development of MSC therapies.

The competitive landscape of the MSC market is shaped by ongoing research, collaborations, and the development of proprietary technologies for stem cell culture, expansion, and differentiation. Companies such as Thermo Fisher and Lonza Group are focusing on improving biomanufacturing techniques and providing high-quality MSC products for research and clinical applications. Others, such as Mesoblast and Osiris Therapeutics, are more focused on advancing clinical trials and seeking regulatory approvals for MSC-based therapies for conditions such as osteoarthritis, cardiovascular diseases, and autoimmune disorders. The competition is further intensified by advancements in regulatory approval processes and increasing investment in research and development, pushing companies to enhance their product portfolios.

Insights into the market suggest that the focus is shifting towards the optimization of MSC-based therapies and improving their accessibility. As demand grows for regenerative medicine and cell-based therapies, companies are investing in automation, standardized processes, and innovations to reduce production costs. The development of allogeneic MSC products, which offer off-the-shelf availability, is also a major trend, allowing companies to scale their operations and reach broader patient populations. Furthermore, strategic mergers, acquisitions, and partnerships are helping companies expand their research capabilities and broaden their market reach, thereby strengthening their positions in the MSC market.

Thermo Fisher Scientific is a prominent player in the MSC market, providing a range of products and services to support stem cell research and therapy development. The company offers cell culture media, reagents, and equipment necessary for the cultivation and expansion of mesenchymal stem cells. Thermo Fisher is involved in various collaborations and partnerships aimed at advancing the use of MSCs in clinical applications.

Lonza Group is another MSC market key player. It offers a variety of cell culture products, services, and manufacturing solutions for stem cell research and therapeutic development. The company works with biopharmaceutical companies and research institutions to develop MSC-based treatments, focusing on improving cell expansion, differentiation, and quality control processes.

Key Companies in Mesenchymal Stem Cells Market

- Thermo Fisher Scientific

- Lonza Group

- Merck KGaA

- Bio-Techne Corporation

- Stemcell Technologies

- Cellular Dynamics International

- Miltenyi Biotec

- Osiris Therapeutics

- AlloSource

- ReNeuron

- EMD Millipore

- Astellas Pharma

- Kite Pharma

- Celyad

- Mesoblast

Mesenchymal Stem Cells Market Developments

- September 2024: Lonza expanded its collaboration to enhance the production of allogeneic MSC therapies. This partnership aims to meet the increasing demand for off-the-shelf regenerative treatments. This partnership underscores Lonza’s role in scaling MSC production and advancing the clinical application of these therapies.

- August 2024: Thermo Fisher announced the launch of a new bioreactor system designed to improve the scalability and consistency of cell culture processes, including for stem cell-based therapies. This advancement highlights the company's focus on enhancing biomanufacturing capabilities to support the growing demand for MSC applications.

Mesenchymal Stem Cells Market Segmentation

By Products and Services Outlook

- Cell & Cell Lines

- Consumables

- Services

By Workflow Outlook

- Cell Sourcing & Isolation

- Culture & Cryopreservation

- Differentiation

- Characterization

By Type Outlook

- Autologous

- Allogeneic

By Application Outlook

- Disease Modeling

- Drug Development & Discovery

- Stem Cell Banking

- Tissue Engineering

- Toxicology Studies

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Mesenchymal Stem Cells Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 3.37 billion |

|

Market Size Value in 2025 |

USD 3.79 billion |

|

Revenue Forecast in 2034 |

USD 11.26 billion |

|

CAGR |

12.9% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive landscape |

|

|

Report format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy

The mesenchymal stem cells market has been segmented into detailed segments of products and services, workflow, type, and application. Moreover, the study provides the reader with a detailed understanding of the different segments at both the and regional levels.

Growth/Marketing Strategy

The growth strategy for companies in the mesenchymal stem cells (MSCs) market focuses on expanding research and development efforts to enhance the efficacy and scalability of MSC-based therapies. Companies are investing in advanced biomanufacturing techniques and automation to reduce production costs and improve the consistency of cell products. Strategic partnerships, collaborations with research institutions, and mergers or acquisitions are key tactics to strengthen product offerings and expand market reach. Additionally, increasing focus on regulatory compliance and securing approvals for clinical applications are essential to gaining market access. Marketing strategies often involve educating healthcare providers and investors about the potential of MSC therapies in treating a variety of chronic diseases and disorders.

FAQ's

? The mesenchymal stem cells market size was valued at USD 3.37 billion in 2024 and is projected to grow to USD 11.26 billion by 2034.

? The market is projected to register a CAGR of 12.9% during the forecast period, 2025-2034.

? North America had the largest share of the market.

? Key players in the mesenchymal stem cells (MSCs) market include companies such as Thermo Fisher Scientific, Lonza Group, Merck KGaA, Bio-Techne Corporation, and Stemcell Technologies. Other significant contributors include Cellular Dynamics International, Miltenyi Biotec, Osiris Therapeutics, AlloSource, and ReNeuron.

? The cell & cell lines segment accounted for the largest share of the market.

? The Culture & Cryopreservation segment accounted for the largest share of the market.

? Mesenchymal stem cells (MSCs) are a type of multipotent stem cell that can differentiate into a variety of cell types, including bone cells (osteocytes), cartilage cells (chondrocytes), and fat cells (adipocytes). They are primarily found in tissues such as bone marrow, adipose tissue, and the umbilical cord and are known for their regenerative properties. MSCs have gained significant attention in regenerative medicine and cell therapy due to their ability to repair or replace damaged tissues, promote healing, and modulate immune responses. These cells are being explored in clinical applications for treating conditions like osteoarthritis, cardiovascular diseases, and autoimmune disorders.

? A few key trends in the mesenchymal stem cells market are described below: Increased Focus on Regenerative Medicine: Growing applications of MSCs for tissue repair and regenerative therapies, particularly in orthopedics, cardiovascular, and neurological diseases. Advancements in Biomanufacturing: Improved cell culture and production techniques, including the use of automated systems and bioreactors, to enhance scalability and reduce production costs. Growing Adoption of Allogeneic MSCs: Increasing use of off-the-shelf, donor-derived MSCs to meet the demand for scalable therapies. Expansion of Clinical Trials: An increase in clinical trials exploring MSC therapies for various conditions, advancing research in their therapeutic potential.

? A new company entering the mesenchymal stem cells (MSCs) market could focus on advancing biomanufacturing techniques to improve the scalability, consistency, and cost-effectiveness of MSC production. Developing innovative, off-the-shelf, allogeneic MSC products could address the growing demand for ready-to-use therapies, offering a competitive edge. Additionally, investing in personalized medicine and tailoring MSC therapies to specific patient needs could differentiate the company in the market. Forming strategic partnerships with research institutions and clinical centers to expedite clinical trials and regulatory approvals would further enhance its market position. A focus on innovative applications, such as MSCs in drug discovery and disease modeling, could also provide a unique value proposition.

? Companies manufacturing, distributing, or purchasing Mesenchymal Stem Cells and related products, and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved