Lancets Market Size, Share, Trends, Industry Analysis Report: By Type, Application, Gauze Size (22G and Below, 23G–33G, and Above 33G), Age Group, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Dec-2024

- Pages: 128

- Format: PDF

- Report ID: PM5315

- Base Year: 2024

- Historical Data: 2020-2023

Lancets Market Overview

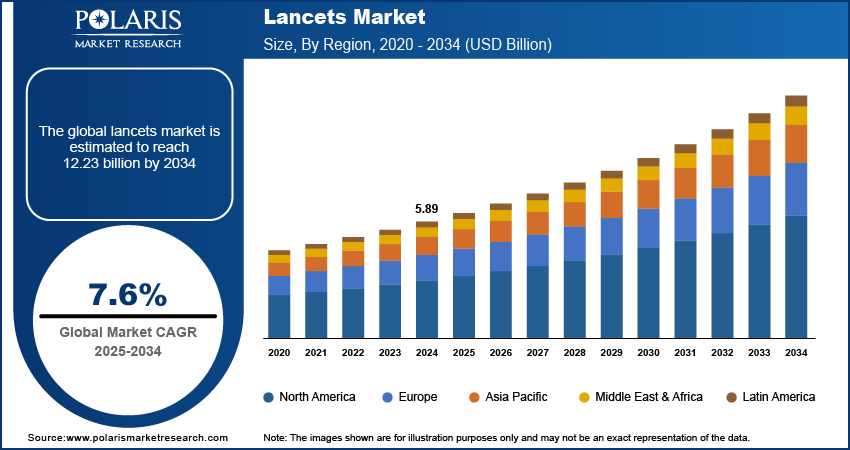

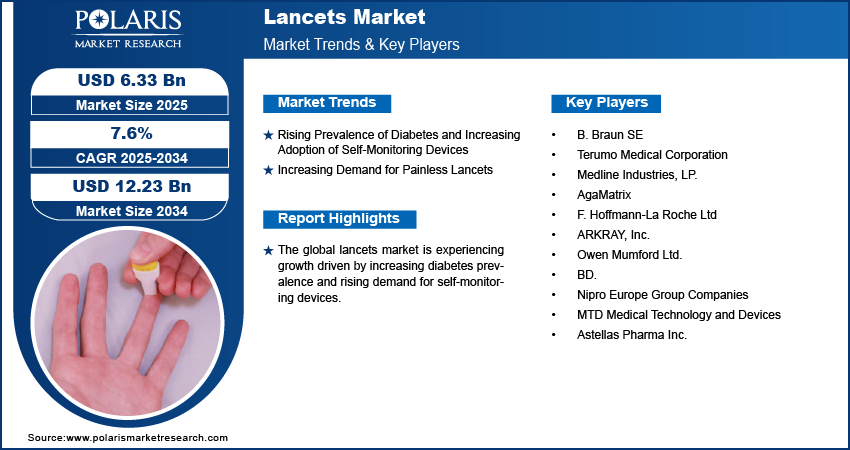

The lancets market size was valued at USD 5.89 billion in 2024. The market is projected to grow from USD 6.33 billion in 2025 to USD 12.23 billion by 2034, exhibiting a CAGR of 7.6% during 2025–2034.

Lancets are small, sharp medical devices used to make skin punctures, primarily for obtaining blood samples in procedures such as glucose testing and other diagnostic purposes. They are designed for single-use to ensure safety and reduce the risk of contamination or infection.

The lancets market demand is driven by the increasing prevalence of chronic conditions such as diabetes, which necessitate frequent blood glucose monitoring. These single-use devices are essential for minimally invasive blood sampling and are widely used in diagnostic applications across healthcare settings and home care environments. The market is further driven by technological advancements, such as improved safety features to minimize cross-contamination risks and pain reduction mechanisms. Rising awareness about preventive healthcare and point-of-care diagnostics also contributes to the lancets market expansion. For instance, in March 2021, Owen Mumford launched the Unistik Touch 16G safety lancet for high-volume capillary blood sampling. The device incorporates features such as one-touch activation and Comfort Zone Technology to minimize discomfort during use. It is designed to support healthcare professionals and point-of-care testing kits while addressing safety concerns and reducing sampling errors. Additionally, the growing geriatric population and expanding access to healthcare services in emerging markets are supporting the market growth.

To Understand More About this Research: Request a Free Sample Report

Lancets Market Drivers

Rising Prevalence of Diabetes and Increasing Adoption of Self-Monitoring Devices

The growing prevalence of diabetes has led to an increased need for regular blood glucose testing devices, thereby driving the demand for lancets, as they are crucial for capillary blood sampling. A report from the Institute for Health Metrics and Evaluation, published in June 2023, highlighted that over 500 billion people worldwide are suffering from diabetes. This number is projected to more than double to 1.3 billion over the next 30 years, indicating an increase in the demand for tools such as lancets for blood glucose monitoring. Moreover, as more individuals seek to monitor their blood sugar levels regularly, the use of lancets in at-home and clinical settings increases, supporting the market's growth. Additionally, the increasing preference for in-home monitoring solutions has led to greater adoption of lancets as part of self-care routines, promoting convenience and timely management of the condition. The shift toward preventive healthcare and the need for constant monitoring in chronic disease management propel the lancets market growth.

Increasing Demand for Painless Lancets

Patients seek more comfortable and less invasive methods for blood sampling. This demand is particularly noticeable among individuals affected by chronic conditions such as diabetes, where frequent blood glucose monitoring is essential. There is a growing emphasis on lancets that minimize pain and discomfort, improving patient compliance and overall experience as self-monitoring devices gain popularity. Manufacturers are responding by developing lancets with advanced technologies such as automatic retraction and Comfort Zone Technology, which are designed to reduce pain and enhance safety. For instance, in October 2024, the University of Colorado Boulder unveiled a new handheld diagnostic system that uses sound waves to analyze blood samples. The organization stated that the device can provide precise test results within an hour with just a finger prick, making it ideal for bedside diagnostics. Thus, this shift toward more comfortable solutions that reduce pain is driving the lancet market development.

Lancets Market Segment Analysis

Lancets Market Assessment by Type Outlook

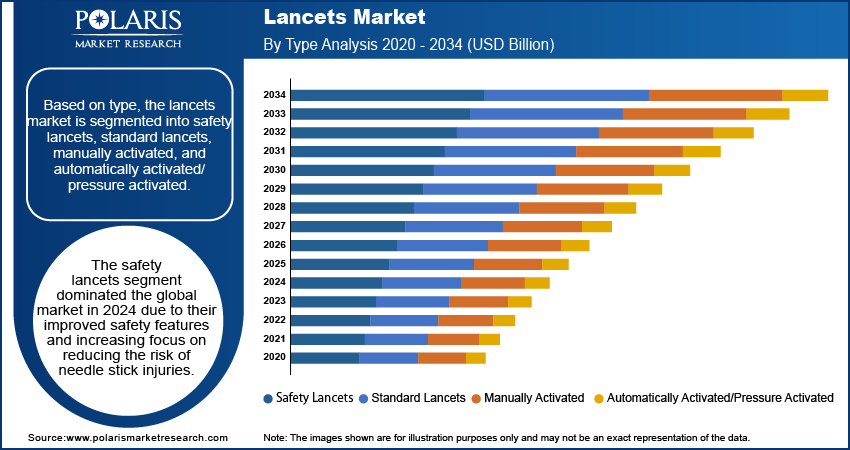

The global lancets market segmentation, based on type, includes safety lancets, standard lancets, manually activated, and automatically activated/pressure activated. The safety lancets segment dominated the global market in 2024 due to their improved safety features and increasing focus on reducing the risk of needle stick injuries. Safety lancets are designed with automatic retraction mechanisms, preventing accidental pricks after use and making them more reliable and safer for healthcare professionals and patients. The growing focus on patient safety and infection control in clinical settings, along with the rising adoption of self-monitoring devices for chronic conditions such as diabetes, has further driven the demand for safety lancets. Additionally, their ease of use and reduced risk of cross-contamination make them an essential tool for home care settings, contributing to their market dominance.

Lancets Market Evaluation by Application Outlook

The global lancets market segmentation, based on application, includes glucose testing, hemoglobin testing, coagulation testing, cholesterol testing, allergy testing, neonatal testing, and other applications. The hemoglobin testing segment is expected to register the highest CAGR during the forecast period due to the increasing prevalence of anemia, a condition related to low hemoglobin levels, particularly in developing regions where malnutrition is more common. Additionally, hemoglobin testing is becoming a routine part of healthcare diagnostics, especially for monitoring individuals with chronic conditions such as diabetes and kidney disease. The convenience of home-based testing and the increasing demand for point-of-care devices that offer quick, accurate results have further fueled the segment growth. This trend is supported by advancements in lancet technology that improve ease of use and minimize pain, making it more appealing for patients and healthcare professionals.

Lancets Market Regional Analysis

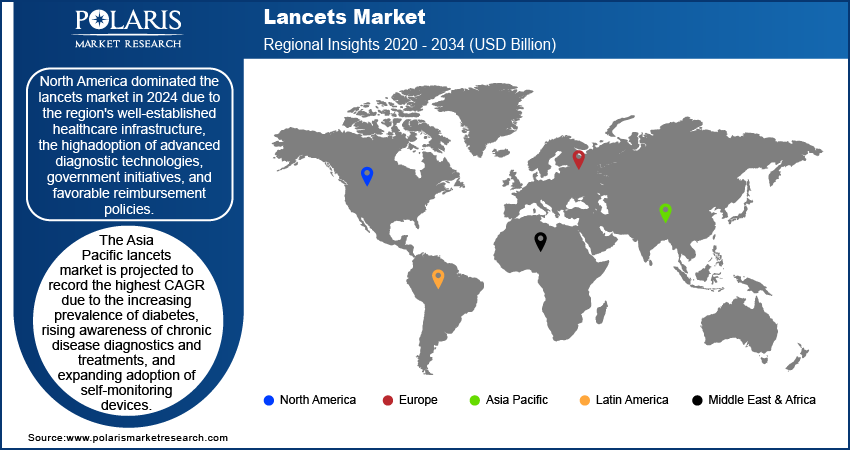

By region, the study provides lancets market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the lancets market share in 2024 due to the region's well-established healthcare infrastructure, the high adoption of advanced diagnostic technologies, government initiatives, and favorable reimbursement policies. Additionally, the increasing prevalence of chronic diseases such as diabetes, which requires frequent blood glucose testing, has created a strong need for lancets. The region also benefits from a high rate of healthcare awareness and self-monitoring, particularly in home-based testing. Moreover, strong market presence from leading lancet manufacturers and the development of innovative, user-friendly products such as safety lancets further fuel the market growth. Additionally, the rising demand for pain-minimizing technologies, such as automatic retraction and comfort zone technology, aligns with the growing consumer preference for less invasive testing options in North America.

The Asia Pacific lancets market is projected to register the highest CAGR due to increasing diabetes prevalence, rising healthcare awareness, and expanding adoption of self-monitoring devices. The region's growing healthcare infrastructure, alongside rising disposable incomes, is contributing to a higher demand for advanced diagnostic tools. Additionally, the shift toward home-based diagnostic testing and the increasing focus on preventive healthcare are expected to drive lancets market expansion in the region. In April 2024, BD India launched the BD Vacutainer UltraTouch Push Button Blood Collection Set, featuring BD RightGauge and PentaPoint Technologies. The set uses a thinner needle to reduce insertion pain and incorporates Push Button Technology, which lowers the risk of needle injuries by 88%.

Lancets Market – Key Players and Competitive Analysis

The competitive landscape of the lancets market features a mix of global leaders and regional players competing to secure market share through innovation, strategic alliances, and geographic expansion. A few major companies such as Medline Industries, LP. and AgaMatrix leverage their robust R&D capabilities and vast distribution networks to develop and deliver advanced lancet solutions tailored to various healthcare applications, such as diabetes management, cholesterol testing, and routine blood sampling. These dominant players focus on improving product precision, patient comfort, and usability to address the growing demand for minimally invasive and user-friendly devices. Simultaneously, regional firms are emerging with specialized products tailored to meet local needs, emphasizing affordability and accessibility. Key competitive strategies include mergers and acquisitions, partnerships with healthcare organizations, and the introduction of eco-friendly and reusable lancet designs to align with sustainability trends. B. Braun SE; Terumo Medical Corporation; Medline Industries, LP.; AgaMatrix; F. Hoffmann-La Roche Ltd; ARKRAY, Inc.; Owen Mumford Ltd.; BD; Nipro Europe Group Companies; MTD Medical Technology and Devices; and Astellas Pharma Inc. are among the key market players.

Roche, officially known as F. Hoffmann-La Roche Ltd, is a biotechnology firm dedicated to advancing medical solutions for various significant ailments. Its focus encompasses the development of drugs and diagnostic tools to combat major diseases, such as cancer, autoimmune disorders, central nervous system conditions, eye-related afflictions, infectious ailments, and respiratory issues. Roche also provides comprehensive diabetes management solutions, in vitro diagnostic systems, and cutting-edge cancer diagnostics based on tissue analysis. The company's operational structure revolves around two key segments: diagnostics and pharmaceuticals. Under the pharmaceutical domain, Roche concentrates on creating innovative medications in oncology, immunology, ophthalmology, infectious diseases, and neuroscience. The company specializes in disease identification via in vitro diagnostic procedures in the diagnostic realm. Its pursuits extend to pioneering research and exploration of novel disease prevention, detection, and treatment strategies. Its broad range of offerings caters to diverse stakeholders, including hospitals, commercial laboratories, healthcare practitioners, researchers, and pharmacists.

B. Braun SE is a medical technology company that produces a wide range of medical devices and pharmaceutical products. These include surgical instruments; infusion pumps and systems; suture materials; dialysis equipment and accessories; hip and knee implants; and products for disinfection, ostomy, and wound care. The company operates through Hospital Care, Avitum, and Aesculap. The Hospital Care division specializes in providing nutrition, infusion, and pain therapy products. Its system solutions include single-use products, drugs, and smart medical device systems for infusion therapy. The division also offers parenteral and enteral nutrition products and drink solutions for nutritional therapy.

List of Key Companies in Lancets Market

- B. Braun SE

- Terumo Medical Corporation

- Medline Industries, LP.

- AgaMatrix

- F. Hoffmann-La Roche Ltd

- ARKRAY, Inc.

- Owen Mumford Ltd.

- BD.

- Nipro Europe Group Companies

- MTD Medical Technology and Devices

- Astellas Pharma Inc.

Lancets Market Development

In December 2023, BD received FDA 510(k) clearance for a novel fingertip blood collection device designed to draw samples via a fingerstick, delivering lab-quality results for several commonly ordered blood tests.

In July 2024, Babson Diagnostics launched BetterWay, a diagnostic solution that is a fingertip collection device to extract a small blood sample roughly the size of a pea. The device is paired with a micro sample lab and advanced technology, that eliminates the need for traditional blood-drawing methods such as needles and vials, enabling diagnostic testing across Austin without the need for a phlebotomist.

Lancets Market Segmentation

By Type Outlook (Revenue, USD Billion, 2020–2034)

- Safety Lancets

- Standard Lancets

- Manually Activated

- Push Button Lancets

- Side Button Lancets

- Automatically Activated/Pressure Activated

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Glucose Testing

- Hemoglobin Testing

- Coagulation Testing

- Cholesterol Testing

- Allergy Testing

- Neonatal Testing

- Other Applications

By Gauze Size Outlook (Revenue, USD Billion, 2020–2034)

- 22G and Below

- 23G–33G

- Above 33G

By Age Group Outlook (Revenue, USD Billion, 2020–2034)

- Adult

- Pediatrics

By End User (Revenue, USD Billion, 2020–2034)

- Hospitals, Clinics, and Ambulatory Surgery Centers

- Homecare Settings

- Other End Users

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Lancets Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 5.89 billion |

|

Market Size Value in 2025 |

USD 6.33 billion |

|

Revenue Forecast by 2034 |

USD 12.23 billion |

|

CAGR |

7.6% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global lancets market size was valued at USD 5.89 billion in 2024 and is projected to grow to USD 12.23 billion by 2034.

The global market is projected to register a CAGR of 7.6% during the forecast period.

In 2024, North America dominated the market due to the strong presence of leading research institutions, early adoption of advanced diagnostic technologies, and substantial investments in optical and photonic technologies across the region.

A few key players in the market are B. Braun SE; Terumo Medical Corporation; Medline Industries, LP.; AgaMatrix; F. Hoffmann-La Roche Ltd; ARKRAY, Inc.; Owen Mumford Ltd.; BD; Nipro Europe Group Companies; MTD Medical Technology and Devices; and Astellas Pharma Inc.

The safety lancets segment dominated the global market in 2024.

The hemoglobin testing segment is expected to register the highest CAGR in the market during the forecast period.

© 2025 Polaris Market Research and Consulting. All rights reserved