Lab Automation Market Share, Size, Trends, Industry Analysis Report, By Product (Software, System); By Automation; By Application; By End-Use; By Region; Segment Forecast, 2024 - 2032

- Published Date:Jan-2024

- Pages: 114

- Format: PDF

- Report ID: PM3981

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

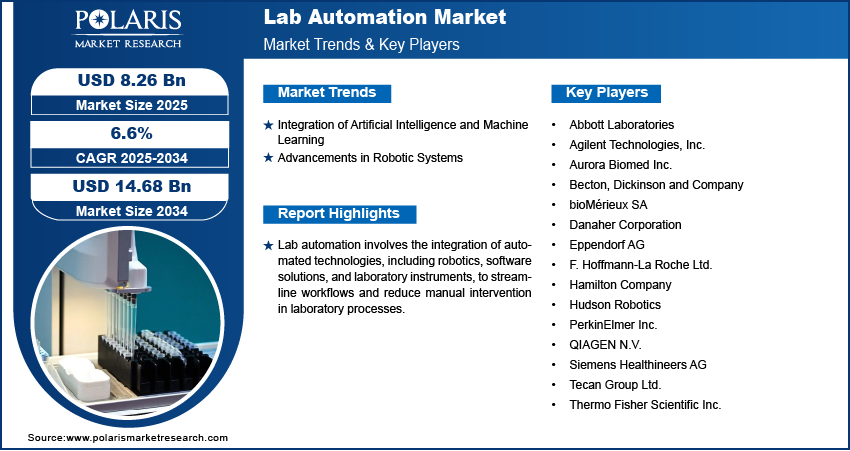

The global lab automation market is projected to witness robust growth. It was valued at USD 5.7 billion in 2023 and is projected to grow to USD 14.09 billion By 2032 exhibiting a CAGR of 6.00% in the forecast period 2024 – 2032.

Laboratory automation employs specific technology to simplify or replace manual handling of methods and equipment, with the extent of automation determined by the laboratory's workflow. Increased adoption of automated tools is commonly seen in academic and research institutions, aiming to enhance productivity and reduce the time allocated to labor-intensive tasks. Moreover, the expanding utilization of automated tools in drug discovery and development is projected to drive market growth in the foreseeable future.

The research study provides a comprehensive analysis of the industry, assessing the market on the basis of various segments and sub-segments. It sheds light on the competitive landscape and introduces the lab automation market key players from the perspective of market share, concentration ratio, etc. The study is a vital resource for understanding the growth drivers, opportunities, and challenges in the industry.

The rising number of patients worldwide means modern labs face increasing pressures to improve both throughput and quality. As such, the resources and workforce of these labs often get stretched to their absolute limit. Besides, the need to manage sophisticated tasks and multiple workflows presents significant challenges to laboratories of all sizes and specialties. To address these issues, several labs have turned towards laboratory automation to replace manual tasks, increase efficiency, and improve quality.

Laboratory automation involves the integration of automation technologies into a lab to improve existing processes and enable new ones. Lab automation offers several benefits to laboratories worldwide, including reproducibility, data accuracy, safety, efficiency, and faster translation. By using automation tools, labs can reduce the safety risks to researchers and technicians. Besides, it can significantly reduce the variability and contamination that may be induced due to the handler. The rising utilization of automation is the primary factor facilitating the lab automation market growth.

To Understand More About this Research: Request a Free Sample Report

For instance, In June 2022, Insilico Medicine revealed its intention to inaugurate an AI-driven robotics laboratory for automated drug discovery.

The increasing array of benefits associated with process automation stands as a pivotal driver for market expansion. Clinical laboratories, in particular, are experiencing a transformative shift from manual operations to automated processes, reaping numerous advantages. These significant advantages encompass heightened productivity, enhanced safety, dependable outcomes, and substantial savings in time, effort, and overall product costs.

Furthermore, lab automation enhances the efficiency of laboratory equipment by handling processes like sample management, verifications, and tube labeling, alleviating the physical strain associated with manual procedures. Consequently, the manifold advantages provided by automated systems are expected to enable small and medium-sized laboratories to embrace these systems for heightened productivity.

The growing demand for process miniaturization serves as another catalyst for the global market. A primary motivator behind the adoption of automated technologies in clinical laboratories is to expedite the miniaturization of research procedures, addressing the challenges of intricate lab automation processes in fields like microbiology, biotechnology, and clinical chemistry. Additionally, miniaturization simplifies cell expansion, monitoring, and cultivation, thereby accelerating turnaround times, especially in point-of-care environments.

Additionally, market growth is poised to be powered by the expanding array of applications within lab automation. A multitude of laboratory processes once reliant on manual procedures has been transformed by the advent of lab automation. This transformation encompasses a wide spectrum, including automated chemistry, synthetic biology, cell line development, genomics, cellular assays, drug discovery, and various other applications. Consequently, the increased clinical utilization of automated instruments in laboratories is expected to drive the adoption of lab automation systems.

Furthermore, the mounting demand for high-throughput analysis within laboratories, capable of handling substantial volumes of samples, is anticipated to present significant growth prospects for the market. Lab automation systems facilitate the automation of time-intensive and repetitive tasks such as liquid handling, data analysis, and sample preparation, thereby amplifying output and streamlining research and testing capabilities.

Industry Dynamics

Growth Drivers

Rising Utilization of Automated Workstations Facilitates Market Growth

The growing adoption of automated workstations in laboratories is enhancing overall performance and productivity. These automated workstations alleviate the mental strain and fatigue that can result from conducting various experiments, enabling lab personnel to use their time more efficiently. Furthermore, customized automated liquid-handling workstations ensure continuous lab operations, even in the absence of personnel, allowing assays to progress over weekends, thus maximizing research progress before the workweek begins. The use of personalized lab workstations is on the rise.

Many larger laboratories employ stand-alone automated liquid handlers, manually moving plates to and from storage incubators, with readers integrated into automated workstations. Most labs are incorporating additional features into benchtop analyzers for liquid handling, facilitating automation through the transition to workstations. While implementing total lab automation can be costly, workstations enhance lab efficiency and reduce manual errors in the process. These factors are expected to drive lab automation market growth in the forecast period.

Report Segmentation

The market is primarily segmented based on product, automation, application, end-user, and region.

|

By Product |

By Automation |

By Application |

By End-User |

By Region |

|

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

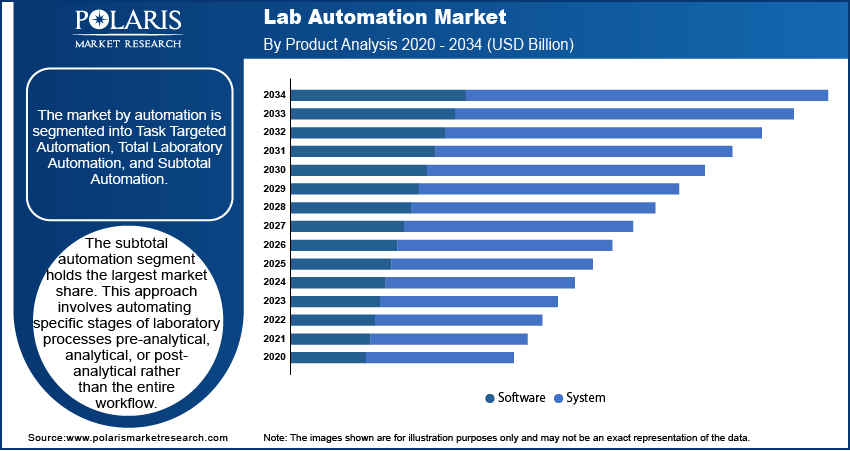

By Product Analysis

The System Segment Held the Largest Revenue Share in 2022

The systems category plays a pivotal role in the market and is expected to demonstrate a substantial CAGR during the forecast period. Lab automation systems encompass different stages of the product life cycle. Notably, microplate readers are currently in their introductory phase, indicating that their adoption is still in the initial stages of market development. The use of automated robots in liquid handling segments is designed to assist human operators. Furthermore, the ability to manage smaller sample volumes is a noteworthy aspect propelling the adoption of robotic instruments within the market. The systems segment can be further subdivided into robotic systems, automated workstations, and microplate readers.

By Application Analysis

The Drug Discovery Segment Accounted for the Highest Market Share During the Forecast Period

The drug discovery segment dominates the market throughout the forecast period. Drug discovery laboratories can significantly reduce the time required for designing, synthesizing, and screening compounds, condensing the process from weeks to mere days despite its inherent complexity and time-consuming nature. This intricacy is a primary reason for the limited involvement of individuals in the drug discovery process. Furthermore, many companies are actively striving to mitigate risks within the drug development process, with one solution being the adoption of laboratory automation technologies in the market. Automated robots and workstations empower researchers to swiftly assess the activity of numerous compounds against specific biological targets facilitated by high-throughput screening. A key advantage is the ability to rapidly and consistently test thousands to hundreds of thousands of agents, including small molecules or functional genomics tools. Laboratories automate procedures through the utilization of robots, plate readers, and specialized instrumentation control and data processing software.

By Automation Analysis

The Subtotal Automation Segment Accounted for the Highest Market Share During the Forecast Period

The partial automation segment constitutes the largest share of the market during the forecast period. Laboratory processes are typically divided into preanalytical, analytical, and post-analytical stages. When one or two of these stages are automated, it falls under the category of partial automation. These are typically standalone or independent specimen processing systems automated to perform various tasks. Partial automation comes with lower costs compared to a full laboratory automation setup. While some medium and a few smaller labs initially leaned towards partial automation, the current trend has shifted, with more labs opting for complete laboratory automation to enhance quality and reduce turnaround time. Beckman Coulter offers a partial automation product system, the AutoMate 800 Sample Processor, tailored for laboratories with daily workloads ranging from 500 to 1500 specimens.

Regional Insights

North America Dominated the Largest Market in 2022

North America emerges as the dominant player in the global lab automation market throughout the forecast period. The United States initially adopted a successful lab automation approach following Japan's lead. Many hospitals embarked on lab automation to address staff shortages, enhance the precision of test results, and elevate patient care. Conventional device-based diagnostics proved costlier for insurance providers, prompting some to reduce reimbursements over the past decade. Consequently, there was a transition to new instruments, marking the inception of automation within the market. This shift compelled hospitals and laboratories to opt for lab automation. Furthermore, the region hosts over 530 regenerative medicine and stem cell medicine companies primarily engaged in product R&D. The laboratories involved in these processes require sophisticated infrastructure, including automated analyzers and liquid-handling instruments integrated with Laboratory Information Management Systems (LIMS) for efficient sample handling and tracking, thereby stimulating regional market growth.

Europe is poised for significant growth in the forecast period, surpassing the pace of development in other regions. The adoption of rapid testing and Point of Care (POC) solutions in European hospitals is steadily increasing. Emergency departments (EDs) are embracing rapid flu tests to expedite diagnoses and alleviate the strain during flu seasons. Europe stands out as a well-established market for in-vitro diagnostics, with large laboratory instruments exhibiting a high degree of automation compared to most POCT devices. This automation has not only enhanced device efficiency but also led to a workforce that is fully trained and acclimated to this technology. Additionally, the region is witnessing notable advancements in the field of regenerative medicine, including the introduction of cutting-edge infrastructure for cell and gene therapies, positioning it as a formidable competitor to the US market. These developments are expected to drive the demand for lab automation in the region.

Key Market Players & Competitive Insights

The market is characterized by intense competition, with established players relying on advanced technology, high-quality products, and a strong brand image to drive revenue growth. These companies employ various strategies such as research and development, mergers and acquisitions, and technological innovations to expand their product portfolios and maintain a competitive edge in the market.

Some of the major players operating in the global market include:

- Abbott

- Agilent Technologies

- Bio-Rad Laboratories

- CrelioHealth

- Danaher

- Dassault Systèmes

- Hoffmann-La Roche

- Illumia

- INTEGRA Biosciences

- LabLynx

- LabVantage

- Peak Analysis & Automation

- Siemens Healthineers

- Tecan

- Thermo Fisher Scientific

Recent Developments

- In May 2023, Opentrons has introduced the Opentrons Flex robot, a next-generation, cost-effective, and user-friendly liquid-handling laboratory robot aimed at democratizing access to advanced lab automation for labs of all sizes and making it accessible to a broader spectrum of researchers.

- In April 2023, MolGen, headquartered in Utrecht and specializing in life science research reagents, disclosed its acquisition of Synchron Instrumenten BV, a Dutch company renowned for automation solutions. Synchron Instrumenten, also recognized as Synchron Lab Automation, has been delivering automated solutions for a diverse range of laboratory applications, encompassing fields such as oil, agriculture, chemicals, clinical, and water/food, since its establishment in 1985.

- In January 2023 Becton, Dickinson, and Company (BD) unveiled the latest iteration of the BD Kiestra Complete Lab Automation System, representing the third generation, designed for microbiology laboratories.

Lab Automation Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 6.03 billion |

|

Revenue forecast in 2032 |

USD 14.09 billion |

|

CAGR |

6.00% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024 – 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments Covered |

By Product, By Automation, By Application, end-user, By End-Use, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region, and segmentation. |

Seeking a more personalized report that meets your specific business needs? At Polaris Market Research, we’ll customize the research report for you. Our custom research will comprehensively cover business data and information you need to make strategic decisions and stay ahead of the curve.

In today’s hyper-connected world, running a business around the clock is no longer an option. And at Polaris Market Research, we get that. Our sales & analyst team is available 24x5 to assist you. Get all your queries and questions answered about the lab automation market report with a phone call or email, as and when needed.

© 2025 Polaris Market Research and Consulting. All rights reserved