IoT Professional Services Market Share, Size, Trends, Industry Analysis Report, 2023 - 2032

REPORT DETAILS

REPORT DETAILS

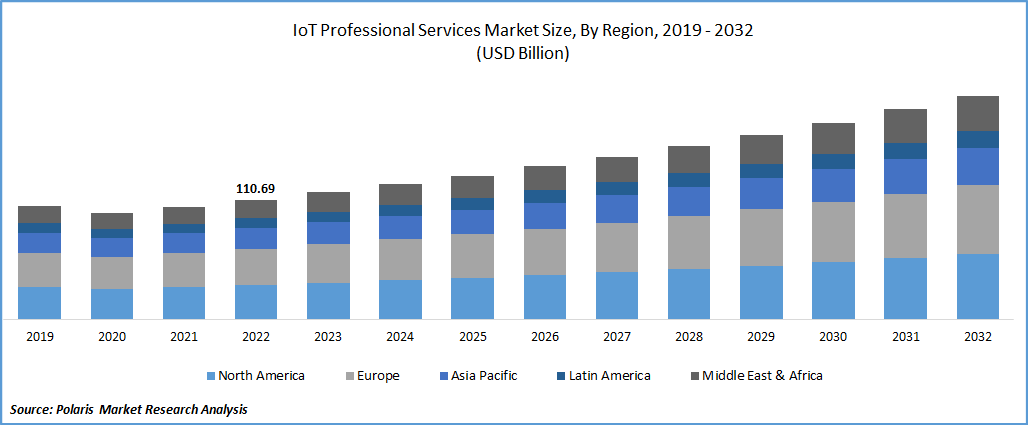

The global IoT professional services market was valued at USD 110.69 billion in 2022 and is expected to grow at a CAGR of 6.5% during the forecast period.

The continuously emerging trend of adopting a variety of connected devices across industrial sectors owing to the growing number of applications, business models, and falling device costs is a major key factor boosting the growth of the global market at a significant pace. Moreover, the wide range of benefits offered by new and advanced IoTs in reducing costs, improved data analytics, and predictive maintenance along with the high focus by key companies on the development and improvement of their products/services across the globe are propelling the adoption rates.

Know more about this report: Download Sample Report

For instance, according to our findings, there are over 13 billion connected IoT devices currently existing across the globe and it is projected to reach around 25.4 billion IoT devices by 2030. In recent past years, there has been a tremendous shift from Non-IoT to IoT devices and about 75% of all devices are estimated to be IoT-connected devices, by 2030.

Furthermore, the rapidly growing penetration of communication and advanced networking technologies worldwide and the need for connected assets, real-time analytics, and security of machines has led to a higher demand for IoT professional services, as it effectively assists in configuration and control, software updates and maintenance, provisioning and authentication, and monitoring and diagnostics of numerous connected devices.

However, shortage of qualified personnel and a very limited understanding of the latest IoT ecosystem, as understanding these technologies is quite complex and challenging since it refers to the synchronicity of almost every component and alignment of various sensors, which is major factors expected to hamper the growth of the global market over the coming years.

The outbreak of the COVID-19 pandemic has significantly impacted the growth of the IoT professional services market. During the pandemic, the global supply chain and demand for various electronics were highly disrupted due to the imposed lockdown and temporary shutdowns of manufacturing facilities in countries like China, which directly affected the demand for deployment services related to IoT devices.

Know more about this report: Download Sample Report

Industry Dynamics

Growth Drivers

There has been a growing need and demand for data processing and advanced analytics along with the increasing usage of IoTs in big data analytics tools to easily acquire data and make better strategic decisions more quickly, which are expected to be the key factors driving the global IoT professional services market growth over the anticipated period. Big data analytics has gained high popularity as a crucial method for the analysis of data produced by connected devices that allow individuals to take control of their decision-making capabilities and enhance it.

Moreover, an increased demand for IoT-based digital transformation by various organizations around the world, as they could enhance their operational efficiency through IoTs is also fueling the adoption of these services rapidly. The desire for digital transformation is mainly influenced by some of the latest technologies including cloud computing, big data analytics, and edge computing across several verticals such as retail, agriculture, transportation, and manufacturing.

Report Segmentation

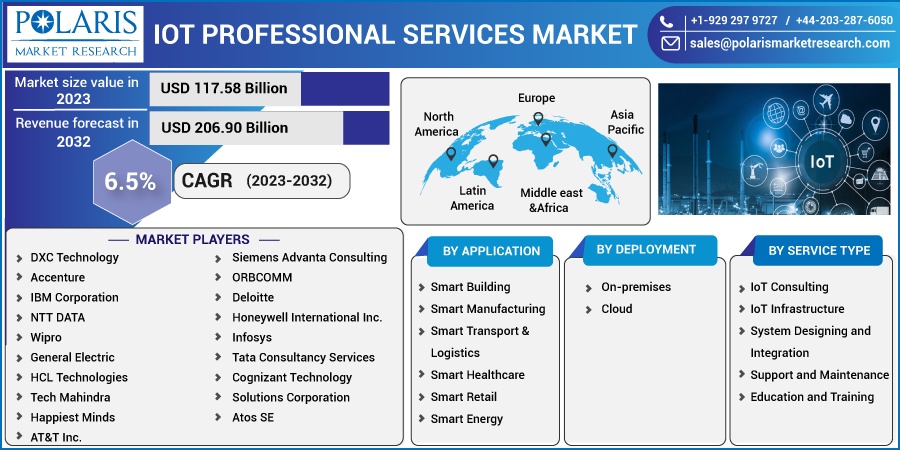

The market is primarily segmented based on application, deployment, service type, and region.

| By Application | By Deployment | By Service Type | By Region |

|

|

|

|

Know more about this report: Download Sample Report

Smart manufacturing segment accounted for the largest market share

The smart manufacturing segment accounted for a considerable global market share in 2022 and is expected to grow considerably over the projected period. The growth of the segment market can be mainly attributed to the rising dependency of manufacturers on advanced connected devices with the purpose to improve their productivity, streamline industrial operations, and reduce time to make strategic decisions. In addition, with the growing competition across the globe, manufacturers are highly implementing the establishment of intelligent solutions and expanding their product/service offerings to serve a wider range of consumers contributing significantly to the segment’s growth.

The smart healthcare segment is expected to grow at the fastest CAGR during the anticipated period owing to the increasing prevalence of connected devices to effectively track and monitor patient health and has encouraged healthcare facilities to invest highly in IoT technology, which enables them to get real-time insights into patient health. Additionally, the increasing need for personalized medicine and the high adoption of digital transformation across healthcare verticals in both developed and developing economies is further likely to provide significant growth opportunities to the market over the coming years.

The cloud segment is expected to hold a significant market share

The cloud segment is anticipated to be the fastest growing segment with a holding of significant market revenue share during the forecast period, which is mainly accelerated due to the decrease in service and licensing costs by switching to cloud services from traditional systems. Also, for businesses, the adoption of cloud services leads to a very high return on investment and they can easily utilize these savings on other important developments and innovations to build their market stronger.

However, the on-premises segment led the industry market and accounted for a considerable market share in 2022, on account of a rapid surge in consumer demand for improving their network connectivity to easily carry out the workflow with advanced solutions and technologies and increased security. IoT services help businesses to expand their overall growth rate and increased productivity and further boost the development of infrastructure.

IoT consulting service type segment held the largest market share

The IoT consulting service segment held the highest market share in terms of revenue in 2022, which is mainly driven by the high utilization of this service to plan roadmaps, appraise technologies, define IoT infrastructures, and devise various strategies. It could also be streamlined in numerous business operations for enterprises and further enables organizations to enhance their existing systems and help non-IoT companies with a limited understanding of IoT technologies.

Furthermore, the transportation & logistics segment is likely to witness the highest growth throughout the estimated period due to the increased proliferation of delivering real-time online information regarding traffic flow, asset tracking, and passengers/commuters. Additionally, it is highly used in inventory management, passenger information system management, traffic management, ticketing administration, parking management, and freight management, which is fueling its adoption all over the world and having a positive impact on segment market growth.

The demand in Asia Pacific is expected to witness significant growth

Asia Pacific region is anticipated to emerge as the fastest-growing region with a significant growth rate during the projected period. The growth of the regional market is mainly driven by growing infrastructural advancements and several supportive economic conditions for the improvement of digitalization in countries like India, China, and Indonesia. Moreover, the presence of some of the world’s largest service providers such as Tata Consultancy Services, Infosys, Wipro Limited, and Tech Mahindra Ltd, and their rising efforts on the enhancement of connected device services and offerings are likely to have a significant impact on market growth in the near future.

North America region dominated the market for IoT professional services market in 2022 with a holding of considerable market share owing to the aggressively growing investments in cutting-edge technologies by various industry verticals including energy & utilities, oil & gas, and manufacturing.

Competitive Insight

Some of the major players operating in the global market include DXC Technology, Accenture, IBM Corporation, NTT DATA, Wipro, General Electric, HCL Technologies, Tech Mahindra, Happiest Minds, Siemens Advanta Consulting, ORBCOMM, Deloitte, Honeywell International Inc., Infosys, Tata Consultancy Services, Cognizant Technology Solutions Corporation, Atos SE, and AT&T Inc.

Some of the major players:

- DXC Technology

- Accenture

- IBM Corporation

- NTT DATA

- Wipro

- General Electric

- HCL Technologies

- Tech Mahindra

- Happiest Minds

- Siemens Advanta Consulting

- ORBCOMM

- Deloitte

- Honeywell International Inc.

- Infosys

- Tata Consultancy Services

- Cognizant Technology Solutions Corporation

- Atos SE

- AT&T Inc.

Recent Developments

- In February 2025, Cognizant reported higher fourth-quarter 2024 revenue, driven by growth in AI-powered platforms and recent acquisitions that strengthened its IoT capabilities.

- In March 2024, Accenture introduced the “IoT Integration Hub,” a service that streamlines IoT deployment by integrating diverse devices and platforms with existing IT systems. The initiative supports scalable, secure IoT solutions for industries including healthcare and manufacturing.

- In February 2024, IBM expanded its Watson IoT platform with advanced AI-driven analytics, enabling businesses to gain deeper insights from IoT data. The upgrade enhances operational efficiency and predictive maintenance, particularly for manufacturing and automotive industries, helping optimize IoT deployments.

IoT Professional Services Market Report Scope

| Report Attributes | Details |

| Market size value in 2023 | USD 117.58 billion |

| Revenue forecast in 2032 | USD 206.90 billion |

| CAGR | 6.5% from 2023 – 2032 |

| Base year | 2022 |

| Historical data | 2019 – 2021 |

| Forecast period | 2023 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2023 to 2032 |

| Segments covered | By Application, By Deployment, By Service Type, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

| Key companies | DXC Technology, Accenture, IBM Corporation, NTT DATA, Wipro, General Electric, HCL Technologies, Tech Mahindra, Happiest Minds, Siemens Advanta Consulting, ORBCOMM, Deloitte, Honeywell International Inc., Infosys, Tata Consultancy Services, Cognizant Technology Solutions Corporation, Atos SE, and AT&T Inc. |

FAQ's

key companies are DXC Technology, Accenture, IBM Corporation, NTT DATA, Wipro, General Electric, HCL Technologies, Tech Mahindra, Happiest Minds, Siemens Advanta Consulting, ORBCOMM.

The global IoT professional services market expected to grow at a CAGR of 6.5% during the forecast period.

key segments are application, deployment, service type, and region.

key driving factors are Increased data traffic due to increasing number of IoT connections.

IoT Professional Services Market Size Worth $206.90 Billion By 2032.

The smart manufacturing segment accounted for the largest market share in 2022, driven by manufacturers' growing reliance on advanced connected devices to improve productivity, streamline operations, and reduce decision-making time. Meanwhile, the smart healthcare segment is projected to grow at the fastest CAGR during the forecast period, fueled by increasing adoption of connected devices for real-time patient health monitoring and digital transformation across healthcare.

The IoT consulting segment held the highest revenue share in 2022, primarily due to its widespread use by enterprises to plan technology roadmaps, define IoT infrastructures, and devise operational strategies. It also helps organizations with limited IoT knowledge effectively navigate and adopt IoT technologies into their existing systems.

Download Sample Report of iot professional services market

Please fill out the form to request a customized copy of the research report.