Intraoperative Imaging Market Share, Size, Trends, Industry Analysis Report, By Product (X-ray, C-arms, Intraoperative Ultrasound); By Application; By End-User; By Region; Segment Forecast, 2024 - 2032

- Published Date:Feb-2024

- Pages: 115

- Format: PDF

- Report ID: PM4625

- Base Year: 2023

- Historical Data: 2019 – 2022

Report Outlook

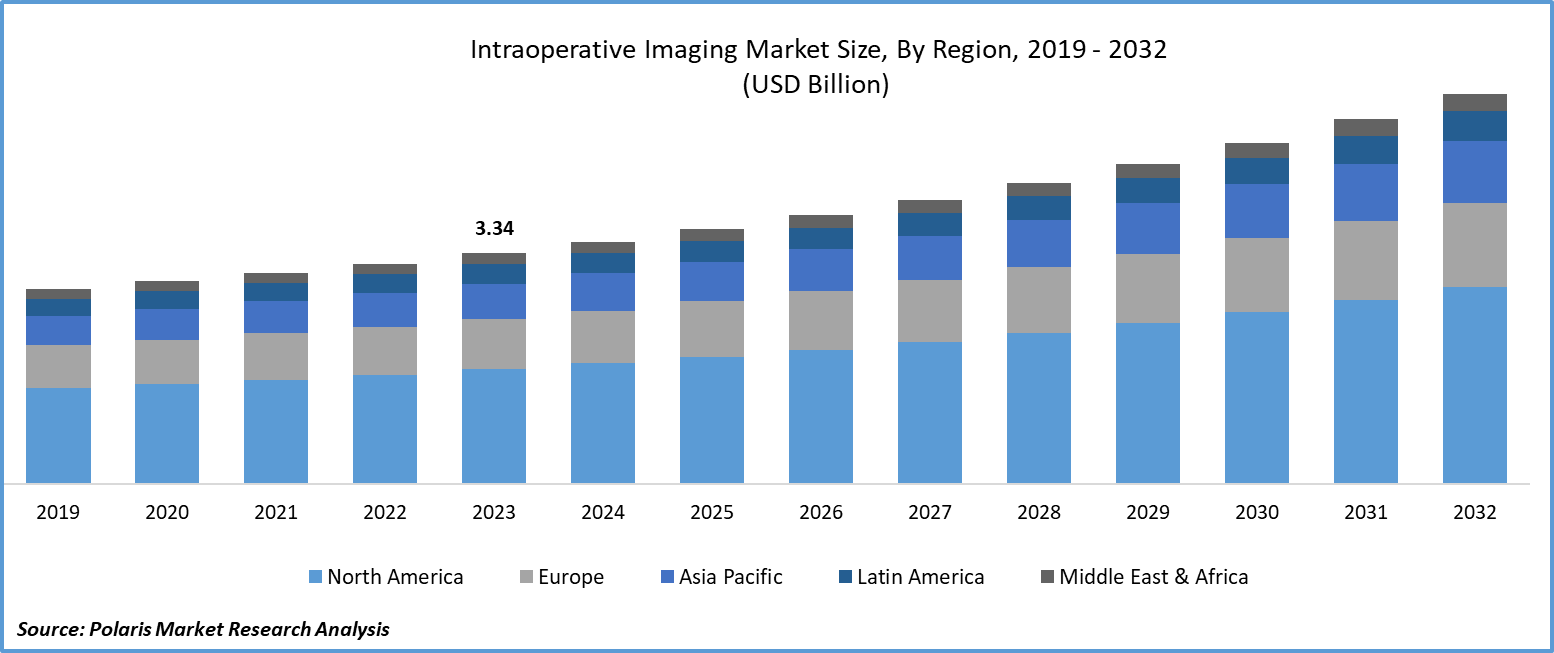

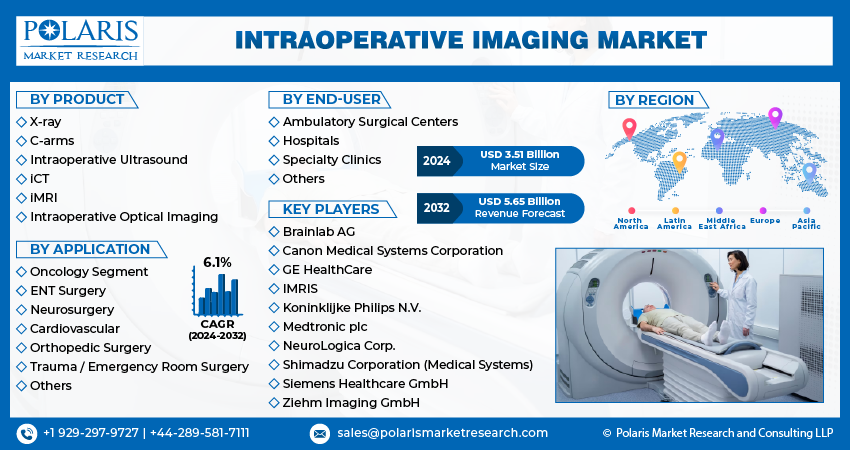

Global intraoperative imaging market size was valued at USD 3.34 billion in 2023. The market is anticipated to grow from USD 3.51 billion in 2024 to USD 5.65 billion by 2032, exhibiting the CAGR of 6.1% during the forecast period.

Intraoperative Imaging Market Overview

The use of intraoperative imaging has grown in popularity due to its ability to improve surgical precision and efficacy. In addition to improving patient outcomes, this strategy simplifies workflows for medical staff both within and outside of the operating room. Technology such as iUltrasound, C-arm and iMRI have greatly increased surgical possibilities. The ability to visualize soft tissues and bones with precision has transformed the way that a variety of disorders are treated in specialties such as neurology, orthopedics, cardiology, and vascular. The further development of technologies like real-time and 3D imaging is anticipated to propel market development.

- For instance, in October 2023, IMRIS and Black Forest Medical Group launched a new cranial stabilization system. This innovative system is designed specifically to assist with intraoperative MRI imaging for neurosurgical procedures.

To Understand More About this Research: Request a Free Sample Report

Moreover, the increasing use of minimally invasive surgeries, which rely on imaging procedures for visualizing the surgical field indirectly throughout the procedure, is anticipated to propel market growth. Nevertheless, the market development may encounter challenges like the high prices of intraoperative imaging systems and a growing preference for refurbished imaging systems in the forecast period.

The research study provides a comprehensive analysis of the industry, assessing the market on the basis of various segments and sub-segments. It sheds light on the competitive landscape and introduces intraoperative imaging market key players from the perspective of market share, concentration ratio, etc. The study is a vital resource for understanding the growth drivers, opportunities, and challenges in the industry.

However, regulatory policies play a crucial role in the development of intraoperative imaging devices, as they are essential for maintaining patient safety, improving the quality of care, and fostering innovation in the medical device sector. However, adhering to these regulations can be costly for manufacturers, potentially affecting the affordability and availability of these devices.

Intraoperative Imaging Market Dynamics

Market Drivers

Rising Technological developments in modalities for intraoperative imaging

The medical device sector has seen significant changes in intraoperative imaging over the last decade, with the introduction of focused imaging technologies and portable or smartphone-based devices. Advanced intraoperative imaging systems offer faster results, higher image quality, easier operations, and simpler consoles compared to traditional devices. Key market players are increasingly focused on launching innovative, technologically advanced products that are cost-effective and easy to use. One notable advancement is the reduction in noise from these systems, with devices now producing much less sound. These advancements aim to improve system functionality and broaden their applications, driving demand among end users.

Market Restraints

High cost associated with the intraoperative imaging systems and its installation is likely to impede the market growth.

Intraoperative imaging techniques are priced at high prices, requiring substantial investments for installation. This leads to higher procedural costs for patients, which can hinder the adoption of new systems, particularly in emerging countries where many healthcare facilities cannot afford such technology. Facilities that do invest in these costly systems often rely on third-party payers like Medicaid, Medicare, or private health insurance plans to reimburse the costs of screening and therapeutic procedures performed using these systems. However, continuous reductions in reimbursement rates for intraoperative imaging scans, coupled with the rising cost of these systems, pose challenges for medium-sized and small healthcare facilities looking to invest in advanced intraoperative imaging technologies.

Report Segmentation

The market is primarily segmented based on product, application, end-user, and region.

|

By Product |

By Application |

By End-User |

By Region |

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

Intraoperative Imaging Market Segmental Analysis

By Product Analysis

- The iMRI segment is projected to grow at the fastest CAGR during the projected period. The iMRI system offers high-quality imaging, enabling greater surgical precision and providing real-time images without the use of ionizing radiation, thereby reducing the risk of inaccuracies. These capabilities have positioned iMRI as a critical tool in surgeries, particularly in neurological procedures. Intraoperative scans allow neurosurgeons to assess anatomical and pathological structures, minimize errors from brain shifts, and update neuronavigational data. Apart from neurological surgeries, iMRI is also applied in other medical specialties like ophthalmology, surgical oncology, and radiation oncology.

- The C-arm segment led the industry market with a substantial revenue share in 2023. This is due to its ability to maneuver around the patient, ensuring optimal imaging angles while keeping the patient comfortable. Technological advancements are expected to drive this segment forward. For instance, in September 2023, Philips introduced the Zenition 30 transportable C-arm system for image-guided therapy. This system, part of the Zenition series, is designed to offer personalized control and clear imaging, enhancing clinical procedure efficiency. Built on the reliable Zenition platform known for its user-friendliness and workflow efficiency, the Zenition 30 is priced to meet current economic and business objectives, making it an ideal choice to enhance decision-making speed and accuracy in various medical procedures.

By Application Analysis

- The neurosurgery segment accounted for the largest market share in 2023 and is likely to retain its position throughout the market forecast period due to the growing prevalence of neurological disorders such as multiple sclerosis, brain tumors, migraine, Parkinson's disease, epilepsy, stroke, Alzheimer's disease, and other forms of dementia. Intraoperative imaging outcomes have a profound impact, enabling neurosurgeons to operate with enhanced precision and accuracy. This reduces the necessity for further procedures and lowers the risk of infections when patients are moved to and from the operating room.

- The orthopedic surgery segment is expected to grow at the fastest growth rate over the coming years. The primary driver of the segment's growth is the increase in traffic accident cases. The World Health Organization (WHO) reports that road traffic accidents have a substantial financial cost, costing most nations approximately 3% of their GDP. It is anticipated that as the number of orthopedic procedures rises, so will the utilization of intraoperative imaging equipment. Though these imaging devices offer real-time guidance during operations, surgical results are enhanced.

By End-User Analysis

- Based on the end-user analysis, the market has been segmented on the basis of ambulatory surgical centers, specialty clinics, and hospitals. In 2023, the hospital segment held the largest share of revenue and is projected to maintain its leadership throughout the forecast period. This can be linked to hospitals using more cutting-edge intraoperative imaging technologies in an effort to improve patient outcomes.

Intraoperative Imaging Market Regional Insights

The North America region dominated the global market with the largest market share in 2023

The North America region dominated the global market with the largest market share in 2023 and is expected to maintain its dominance over the anticipated period. North America is considered a mature market for intraoperative imaging, with the widespread use of these technologies among major end users and established distribution channels for manufacturers and suppliers. The region's high per capita healthcare spending, particularly by the US and Canadian governments, facilitates easy access to and adoption of advanced technologies. Additionally, supportive government regulations contribute to market growth in North America.

The Asia Pacific is expected to be the fastest-growing region with a healthy CAGR during the projected period, owing to the growing need for advanced imaging equipment, driven by an increasing incidence of chronic diseases and a rising elderly population. According to UNFPA, the number of elderly people in the region is projected to triple from 2010 to 2050, reaching nearly 1.3 billion individuals.

Competitive Landscape

The Intraoperative Imaging market is fragmented and is anticipated to witness competition due to several players' presence. Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

Some of the major players operating in the global market include:

- Brainlab AG

- Canon Medical Systems Corporation

- GE HealthCare

- IMRIS

- Koninklijke Philips N.V.

- Medtronic plc

- NeuroLogica Corp.

- Shimadzu Corporation (Medical Systems)

- Siemens Healthcare GmbH

- Ziehm Imaging GmbH

Recent Developments

- In September 2023, GE Healthcare and Mayo Clinic have been entered into a strategic partnership for product development and research programs. This partnership aims to transform the patient and clinician experience in radiology and to enable the delivery of cutting-edge therapies.

Report Coverage

The Intraoperative Imaging market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, product, applications, end-users, and their futuristic growth opportunities.

Intraoperative Imaging Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 3.51 billion |

|

Revenue forecast in 2032 |

USD 5.65 billion |

|

CAGR |

6.1% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024 – 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments covered |

By Product, By Application, By End-User, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation. |

Gain profound insights into the 2024. Intraoperative imaging with meticulously compiled statistics on market share, size, and revenue growth rate by Polaris Market Research Industry Reports. This thorough analysis not only provides a glimpse into historical trends but also unfolds a roadmap with a market forecast extending to 2032. Immerse yourself in the comprehensive nature of this industry analysis through a complimentary PDF download of the sample report.

FAQ's

The global Intraoperative Imaging market size is expected to reach USD 5.65 billion by 2032

Key players in the market are GE HealthCare, Siemens Healthcare GmbH, Medtronic plc, Koninklijke Philips N.V., Canon Medical Systems Corporation

North America contribute notably towards the global Intraoperative Imaging Market

Intraoperative Imaging Market exhibiting the CAGR of 6.1% during the forecast period

The Intraoperative Imaging Market report covering key segments are product, application, end-user, and region.

© 2025 Polaris Market Research and Consulting. All rights reserved