Intelligent Building Automation Technologies Market Growth Analysis, 2026-2034

REPORT DETAILS

Intelligent Building Automation Technologies Market Summary

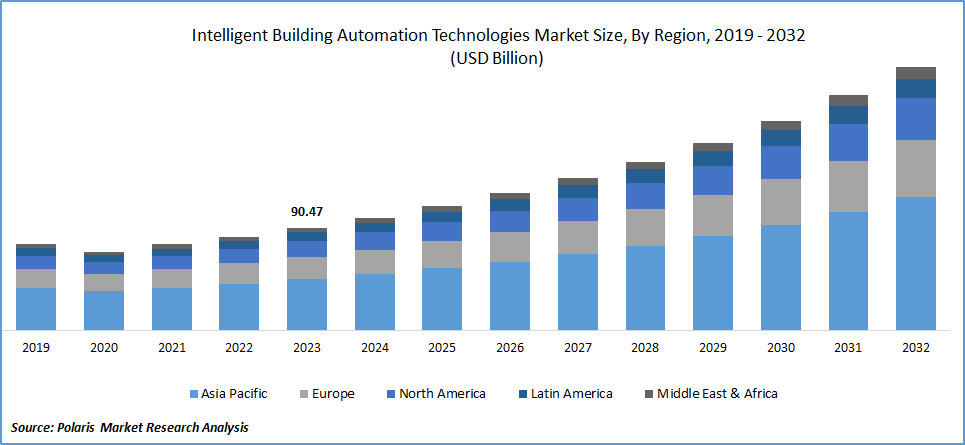

The global intelligent building automation technologies market size was valued at USD 102.59 billion in 2025, growing at a CAGR of 10.39% from 2026 to 2034. Expanding urbanization worldwide drives the demand for intelligent building automation technologies. Also, rising interest in smart home automation and increasing investments in smart city development projects propel industry growth.

Market Statistics

Key Takeaways

- North America accounted for 39.46% of the global market share in 2025. The growth is driven by investments in smart city development.

- The U.S. held a 78.15% share of the North America intelligent building automation technologies market in 2025. Strict energy regulations and corporate sustainability goals boost the dominance. The proliferation of smart buildings also drives the U.S. smart building security systems market.

- The intelligent building automation technologies industry in Asia Pacific is registering a CAGR of 11.78% from 2026 to 2034. The growth is fueled by rapid urbanization and increasing investments in smart city projects.

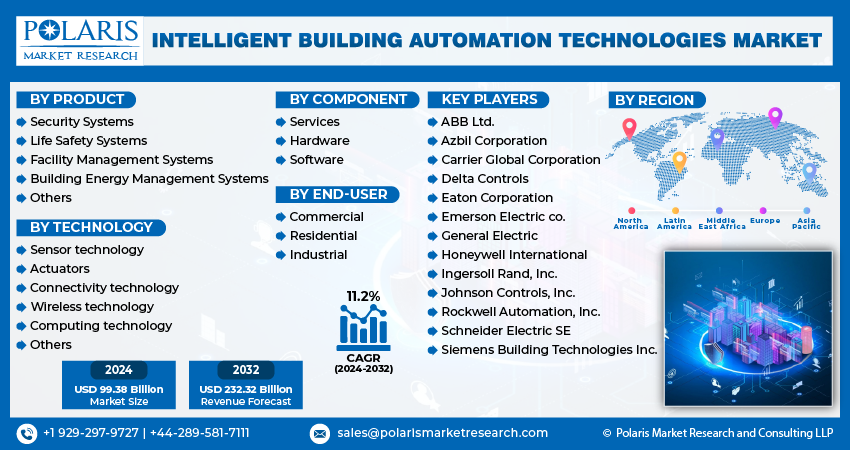

- The hardware segment accounted for 45.96% of revenue share in 2025. The widespread deployment of IoT sensors, controllers, access control systems, and HVAC control devices propels hardware demand.

- The commercial segment was valued at USD 55.77 billion in 2025. The high demand for smart infrastructure across commercial spaces, airports, shopping malls, hospitals, and hotels drives the dominance.

Industry Dynamics

- Rising demand for smart homes propels the adoption of intelligent building automation technologies (IBAT) to manage smart home solutions.

- Increasing investments in the development of smart cities boost the adoption of IBAT. Smart city management needs intelligent building automation technologies to enhance security.

- The rising focus on energy efficiency globally would create a lucrative opportunity during the forecast period.

- The high cost of intelligent building automation technologies hinders the market growth.

AI Impact on Intelligent Building Automation Technologies Market

- Artificial intelligence revolutionizes the intelligent building automation technologies (IBAT) market. The technology is turning traditional structures into responsive, efficient ecosystems.

- AI-powered energy management systems examine usage patterns and adjust lighting, HVAC, and power distribution to cut down on waste.

- Integration of AI with HVAC systems helps adapt HVAC settings in real time based on weather, user preferences, and occupancy.

- AI in building automation enhances building security. It is integrated into facial recognition, anomaly detection, and automated threat response systems.

- Tools with AI analyze foot traffic and usage patterns. It helps optimize lighting zones, space allocation, and cleaning schedules.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

What is Intelligent Building Automation?

Intelligent building automation (IBA) is an advanced way to manage building operations using integrated, data-driven technologies. It develops from traditional Building Automation Systems (BAS) and Building Management Systems (BMS). The smart building automation market includes Building Energy Management Systems (BEMS), smart building software, and energy management systems. These systems are integrated into a unified platform.

IBA uses IoT sensors, AI, and cloud-based analytics. It helps automate and optimize functions like HVAC, lighting, security, and energy use in real time. The integration is referred to as intelligent building automation technology (IBAT). IBAT facilitates predictive maintenance and greater occupant comfort. IBAT connects previously siloed systems. The building energy management systems market delivers products that enable centralized control and reduce energy consumption. This also supports sustainability goals. Thus, intelligent building automation is becoming a critical component of modern smart buildings.

What is IBAT Market Scope?

The global intelligent building automation technologies (IBAT) market refers to the ecosystem of smart technologies integrated into buildings. These technologies are used to automate and optimize system management across buildings. These systems manage heating, ventilation, air conditioning (HVAC); lighting; security; energy; and other essential functions. They use a network of sensors, controllers, and software platforms. The platforms powered by artificial intelligence (AI), the Internet of Things (IoT), and advanced analytics create more responsive, energy-efficient, and secure building environments.

Intelligent building automation helps reduce energy use. Automated systems track energy consumption and environmental conditions. They make adjustments in real time that reduce energy waste. Smart lighting systems dim or turn off based on occupancy or natural light levels. Smart HVAC systems keep temperatures regulated by considering the weather outside and how the rooms are being used. Using smart systems can reduce operational costs. Automation also decreases a building's carbon footprint and supports sustainability efforts.

Safety and security are strengthened through smart building security systems. Advanced security systems in smart buildings include biometric access controls, real-time surveillance with facial recognition, intrusion detection, and emergency response automation. These systems can be managed from a central location and connected to building management platforms. This allows for immediate alerts and actions during emergencies. As a result, using these systems improves the overall safety and strength of facilities.

The expanding urbanization worldwide drives the intelligent building technologies market growth. World Economic Forum, in its 2022 report, stated that the share of the world’s population living in cities is expected to rise to 80% by 2050. Increasing urbanization is putting pressure on developers and property managers. They seek IBAT to optimize energy use and improve security. It is also used to boost occupant comfort in high-density environments. Additionally, there is a rising demand for seamless connectivity and data-driven management in modern urban infrastructure. It fuels the building automation systems market growth.

Market Dynamics

Drivers

Rising Demand for Smart Homes: Consumers want smart homes for luxury and comfort. These smart homes include voice-controlled lighting, smart thermostats, and automated security systems. Developers and manufacturers use smart building automation technologies to manage integrated solutions. Also, energy-saving rules and higher utility costs lead homeowners to choose smart homes. As a result, the growing demand for smart homes increases the need for scalable, smart building automation technologies.

Smart home solutions require interoperable automation architecture, creating demand for scalable hardware, software, and platform ecosystems. Rising utility costs and increasing awareness of energy conservation are also supporting residential adoption. Homeowners are looking for systems that can reduce waste, automate consumption, and support remote control. The growing availability of cost-effective smart devices is making residential deployment more accessible. The devices are increasingly used in urban housing projects and premium apartment developments. Users increasingly expect connected devices to work together through centralized interfaces rather than as standalone smart gadgets. This favors vendors that can link lighting, HVAC, security, and energy management into seamless residential automation experiences.

Increasing Investments in Development of Smart Cities: Smart city development is a major structural growth catalyst for the intelligent building automation technologies market. Governments focus on modernizing transportation hubs, mixed-use developments, public buildings, and utility-connected infrastructure. Thus, the need for integrated automation becomes stronger. Smart city environments benefit from data-rich buildings that can monitor energy, occupancy, safety, and maintenance in real time.

Intelligent building automation supports this transition by enabling efficient use of resources, improved public safety, centralized control, and stronger sustainability outcomes. New projects are now incorporating automation systems from the design stage. Meanwhile, older urban buildings are being updated to fit new energy performance standards and improve building intelligence. Investments in smart cities also boost the need for building systems. The systems can connect with energy networks at the district level, emergency systems, mobility platforms, and digital municipal infrastructure. This widens the market from individual building control toward integrated urban intelligence.

In smart cities, automation systems are integrated in buildings for energy management, real-time monitoring, and better resource use. The need for data-driven smart city management drives the demand for IBAT. This technology is used to improve security and reduce carbon footprints. Investments in smart city projects are rising around the world. These investments focus on updating urban infrastructure, promoting sustainability, and improving quality of life. Therefore, the rising investments in smart city development projects fuel the smart building control systems market growth.

Opportunity

Rising Focus on Energy Efficiency: Energy efficiency remains one of the strongest long-term opportunities in the IBAT market. Automated lighting controls, demand-responsive HVAC systems, and energy analytics platforms are used to reduce waste and improve performance. Energy prices are volatile. Also, carbon reporting requirements are expanding. Thus, building owners are investing in automation. It assists them in gaining visibility into usage patterns and optimizing building operations.

Commercial real estate operators, industrial facilities, and public-sector institutions are under pressure to improve energy performance without compromising safety or comfort. Intelligent automation technologies enable that balance. The technologies use data to make continuous adjustments across building functions. Building energy management systems are particularly attractive in retrofit projects. Older buildings can gain measurable efficiency improvements without complete structural redevelopment. Retrofit-friendly sensors, gateways, wireless controls, and cloud-based analytics platforms are expanding the market. They help reduce deployment complexity and improve payback economics. As a result, increasing focus on energy efficiency will create profitable opportunities for the market in the coming years.

Challenge

High Initial Cost and Integration Complexity: The high upfront cost limits the use of intelligent building automation technologies. This is especially true for smaller property owners and in markets where costs are a concern. The total cost of implementation often goes beyond just buying hardware and software. It also covers integration, commissioning, network upgrades, training, and ongoing maintenance. Legacy infrastructure creates another challenge. Many existing buildings operate with fragmented or outdated systems. These systems are difficult to connect with newer digital platforms. This can increase project timelines and create interoperability issues. It is observed when multiple vendors and protocols are involved.

Rising Concerns Related to Data Security: Cybersecurity is another key challenge that restrains the IBAT industry growth. The technology handles a vast amount of data. Increasing cyberattacks create concerns on data security. Also, more building functions are becoming connected. The attack surface includes access control, surveillance, HVAC, cloud dashboards, and remote service interfaces. Buyers are looking more closely at vendors based on their ability to automate. Encryption, device authentication, patch management, and network resilience are also being considered.

Technology Architecture and Protocol Ecosystem

The Intelligent Building Automation (IBA) technology architecture is structured in three layers.

- Field layer: It includes sensors, actuators, and smart devices that capture real-time data.

- Control Layer: This layer comprises controllers and gateways. They are used in BAS/BMS to process data and execute automation logic.

- Management layer: This integrates BEMS, smart building software, and energy management systems. It enables analytics, visualization, and cloud-based control.

The protocol ecosystem ensures interoperability across multi-vendor systems. Common protocols include BACnet, Modbus, KNX, and LonWorks. BACnet is widely used for HVAC and BMS integration. Modbus helps in industrial device communication. KNX is suitable for building control standards. LonWorks is used for legacy automation networks. Additionally, IP-based and wireless protocols such as MQTT, Zigbee, and Wi-Fi support IoT connectivity and real-time data exchange. This architecture enables scalable, interoperable, and data-driven IBAT ecosystems. It supports seamless integration and intelligent decision-making across building operations.

Source: Polaris Market Research Analysis

Segmental Insights

By Component Analysis

The market is segmented into hardware, software, and services. The hardware segment held 46.25% of the revenue share in 2025. It witnessed 663 million unit sales in 2024. The segment growth is fueled by the widespread deployment of IoT sensors, controllers, access control systems, and HVAC control devices. Organizations across commercial, residential, and industrial sectors prioritize hardware to improve energy efficiency, safety, and operational convenience. The rise of smart sensors and IoT-enabled devices fueled their dominance. These components are essential for any intelligent building setup. In addition, the growing need to retrofit older buildings with automated lighting and energy management systems has increased hardware adoption. The most commercially relevant hardware categories include sensors, controllers, actuators, and networking devices. Sensors collect temperature, humidity, occupancy, light, and air-quality data. Controllers execute system logic, whereas actuators enable physical responses. Networking devices connect building assets into a manageable digital environment. This layered hardware architecture explains why the segment remains the backbone of the IBAT market.

The software segment is expected to register a CAGR of 11.52% from 2026 to 2034. The segment is expected to register 156 million licenses by 2034. Its growth is attributed to the growing emphasis on data-driven decision-making and real-time analytics. Centralized software helps improve energy use and monitor equipment health. It is also used for predictive maintenance strategies. AI and machine learning improve the features of software platforms. They enable automated anomaly detection and analysis of occupant behavior. The technologies also allow for flexible climate control. The trend toward smarter, scalable, and more secure automation systems increases the demand for software solutions in new construction and renovation projects. Software growth is linked to the shift from isolated building management to platform-based coordination. Buyers increasingly prefer solutions that combine energy, security, life safety, HVAC, and occupancy data into one decision layer. This increases demand for building management systems, building energy management software, lighting control platforms, and AI-enabled analytics tools.

The services segment is expected to witness rapid expansion in the coming years. Services are important for system design, integration, commissioning, cybersecurity, and lifecycle maintenance. Customers are using open-protocol and multi-vendor environments. Professional and managed services become important differentiators in successful deployment outcomes.

By End User Analysis

In terms of end use, the segmentation includes commercial, residential, and industrial. The commercial segment was valued at USD 50.53 billion in 2025. Strong demand for smart infrastructure in office buildings, airports, shopping centers, hospitals, and hotels boosts the segment growth. Facility owners in the commercial sector focused on automation to improve operational efficiency. It will also help reduce energy consumption and comply with evolving building codes and sustainability regulations. The increasing use of modern HVAC, lighting, and security control systems has allowed businesses to reduce operating costs. At the same time, these systems improve safety and comfort for occupants. Additionally, intelligent systems support real-time monitoring and performance optimization in commercial buildings. Thus, the increased focus on green building certifications such as LEED and BREEAM fueled investments in these systems.

The residential segment is projected to hold a 27.80% of revenue share by 2034. The growth is fueled by rising urbanization, growing consumer awareness about energy conservation, and the increasing popularity of smart homes. Homeowners are increasingly using integrated systems to manage lighting, security, HVAC, and entertainment through central platforms or mobile apps. Additionally, the drop in prices of smart devices and government incentives for energy-efficient home upgrades are speeding up adoption in single-family homes and multi-unit residential buildings.

Source: Polaris Market Research Analysis

Regional Analysis

North America accounted for 39.56% of the global market share in 2025. This dominance is attributed to the rising need for energy efficiency and increasing investments in smart city development. Governments and organizations in the region have increasingly adopted green building standards. It pushed the integration of hardware components such as IoT-enabled HVAC, lighting, and security systems. The hardware components in North America witnessed 254 million unit sales in 2024. The rise of hybrid work models has also increased demand for smart office solutions. They optimize space utilization and energy consumption. Additionally, advancements in AI and cloud computing enabled predictive maintenance and real-time monitoring. It further propelled demand for intelligent building automation technologies in the region.

U.S. Intelligent Building Automation Technologies Market Insights

The U.S. held a 78.02% share of the North America market in 2025. The country registered sales of 178 million hardware components in 2024. The U.S. market growth is attributed to strict energy regulations, corporate sustainability goals, and the proliferation of smart buildings. The Department of Energy (DOE) and the EPA incentivized energy-efficient buildings through programs such as ENERGY STAR. Such initiatives fueled IBAT adoption in the U.S. The growth of proptech and increasing cybersecurity concerns in smart infrastructure in the U.S. also contributed to U.S. intelligent building automation technologies market dominance.

Europe Intelligent Building Automation Technologies Market Trends

The market in Europe is projected to hold 31.03% revenue share and report 450 million unit sales of hardware components by 2034. The growth is propelled by EU directives such as the Energy Performance of Buildings Directive (EPBD) and the Green Deal. It mandated near-zero-emission buildings by 2030. Countries such as the UK, Germany, France, Italy, and others adopt IBAT to reduce carbon footprints. The rise of sustainable urban development and smart city projects drives the adoption of automation. Additionally, high energy costs and the need for occupant comfort and safety in the region are pushing demand for intelligent automation.

Germany Intelligent Building Automation Technologies Market Overview

The industry in Germany is estimated to register a CAGR of 11.39% during 2026–2034. The imposition of Energieeffizienzstrategie 2050 and stringent building energy act (GEG) regulations drives the industry expansion. The push for energy-neutral buildings and the integration of renewable energy sources drives the IBAT demand. The country’s strong manufacturing sector, which demands smart factories with automated HVAC and lighting, boosts market growth in the country.

Asia Pacific Intelligent Building Automation Technologies Market Trends

The Asia Pacific IBAT market is expected to register a CAGR of 11.71% and register 395 million unit’s sales of hardware components during 2026–2034. Rapid urbanization, smart city projects, and government initiatives drive the industry growth. United Nations Human Settlements Programme, in its report, stated that the urban population in Asia is expected to grow by 50% by 2050. China, Japan, South Korea, and other countries invest heavily in 5G-enabled smart buildings. In India and Southeast Asia, the growth of commercial real estate and concerns about energy costs are boosting demand for automated building systems. Green building certifications in the region are encouraging the use of intelligent building automation technologies. The rising middle class and demand for smart homes are driving market growth.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The intelligent building automation technologies market witnesses intense competition. Key players compete by focusing on innovation and energy efficiency. They also highlight IoT integration and AI-driven automation. They use new technologies to offer smart building solutions. Schneider Electric and Siemens lead with systems that combine building management, HVAC controls, lighting, and security into single platforms. Johnson Controls (OpenBlue) and Honeywell (Forge) focus on AI-driven analysis for predictive maintenance and energy savings. Carrier Global and Daikin emphasize new HVAC solutions with IoT connectivity. Distech Controls, Delta Controls, and other new competitors specialize in open-protocol automation. It appeals to customers seeking flexible systems. Mitsubishi Electric and Robert Bosch leverage their expertise in industrial automation to enhance the reliability of smart buildings. Rockwell Automation and Eaton Corporation serve commercial and industrial facilities with scalable automation solutions.

Emerging competition is increasingly centered on interoperability, cybersecurity, and software intelligence. Buyers are favoring vendors that can integrate legacy systems, support open protocols, deliver measurable energy outcomes, and provide scalable analytics across multiple sites. As a result, competition is shifting from device-level control toward platform value, service capabilities, and long-term operational impact.

A few major companies operating in the industry include ABB Limited; Azbil Corporation; Carrier Global Corporation; Daikin Industries, Ltd.; Delta Controls; Distech Controls; Eaton Corporation; Emerson Electric Co.; Johnson Controls, Inc.; Mitsubishi Electric Corporation; Robert Bosch GmbH; Rockwell Automation, Inc.; and Schneider Electric.

Intelligent Building Automation Market: Vendor Landscape Matrix by Specialization

| Specialization | Focus Area | Key Capabilities | Representative Vendors |

| HVAC / Building Controls | Core BAS/BMS infrastructure | HVAC automation, environmental control, building performance optimization | Siemens, Johnson Controls, Schneider Electric, Honeywell |

| Energy Management | BEMS & EMS solutions | Energy monitoring, analytics, demand response, sustainability optimization | Schneider Electric, ABB, Eaton, Siemens |

| Security & Access Control | Building safety & surveillance | Video surveillance, biometric access, intrusion detection, alarm systems, identity management | Honeywell, Bosch, Hikvision, Johnson Controls |

| Integration / Platform Software | Smart building software & analytics | Cloud platforms, AI-driven insights, system integration, digital twins | IBM, Microsoft, Siemens (Desigo), Schneider Electric (EcoStruxure) |

| Smart Device Ecosystem | Edge devices & IoT layer | Sensors, smart meters, connected devices, wireless communication modules | Legrand, Signify, Cisco, Samsung |

Source: Polaris Market Research Analysis

List of Key Players

- ABB Limited

- Azbil Corporation

- Carrier Global Corporation

- Daikin Industries, Ltd.

- Delta Controls

- Distech Controls

- Eaton Corporation

- Emerson Electric Co.

- Johnson Controls, Inc.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Rockwell Automation, Inc.

- Schneider Electric

Intelligent Building Automation Technologies Industry Developments

- May 2025: ABB announced the launch of ABB Smart EMS, a smart energy management solution. The solution empowers homeowners to control their energy use, reduce costs, and maximize efficiency. (Source:new.abb.com)

- May 2025: Carrier Global Corporation, a global company in intelligent climate and energy solutions, announced its plans to invest an additional $1 billion over five years in manufacturing, innovation, and workforce expansion across the U.S. (Source: www.corporate.carrier.com)

Strategic Analyst View

The long-term outlook for the intelligent building automation technologies market remains highly favorable. This is because building owners increasingly seek infrastructure that is connected, but self-optimizing, secure, and aligned with sustainability metrics. Over the next decade, the strongest value creation is likely to come from software-led orchestration, retrofit modernization, AI-enabled predictive maintenance, and tighter integration between building automation, grid intelligence, and occupant analytics.

The most successful vendors will be those that reduce complexity for customers. They support open standards, integrate legacy systems, and cybersecurity assurance. They also translate automation into measurable outcomes such as energy savings and asset uptime. It leads to lower service costs and better user experience.

Intelligent Building Automation Technologies Market Segmentation

By Component Outlook (Revenue, USD Billion, Volume, 2021–2034)

- Hardware

- Sensors

- Controllers

- Actuators

- Networking Devices

- Others

- Software

- Building Management Systems (BMS)

- Energy Management Software

- Lighting Control Software

- HVAC Control Software

- Fire, Life & Safety and Security

- Others

- Services

- Professional Services

- Managed Services

By End User Outlook (Revenue, USD Billion, Volume, 2021–2034)

- Commercial

- Residential

- Industrial

By Regional Outlook (Revenue, USD Billion, Volume, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Intelligent Building Automation Technologies Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 102.59 billion |

| Market Size in 2026 | USD 112.61 billion |

| Revenue Forecast in 2034 | USD 248.37 billion |

| CAGR | 10.39% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Intelligent Building Automation Technologies Market FAQ's

The global market was valued at USD 102.59 billion in 2025. It is projected to reach USD 248.37 billion by 2034, registering a CAGR of 10.39%.

Rising energy prices and growing concerns over global warming boost the demand for IBAT. Also, increasing awareness of energy conservation fuels IBAT adoption worldwide.

North America dominated the global market in 2025. This is driven by rapid urbanization and large-scale infrastructure development. It is also fueled by the increasing adoption of smart building initiatives across emerging economies.

The commercial segment led the market revenue share in 2025. Offices, retail malls, and hotel facilities use centralized IBAT. It is deployed for energy efficiency and occupant comfort. This factor contributed to the dominance.

High initial cost and integration complexity are key market restraints. Rising data security concerns and shortages of skilled professionals also hinder the IBAT deployment.

AI in building automation helps optimize HVAC and lighting. It improves occupancy-based decision-making. The technology assists in detecting anomalies and predicting maintenance needs. AI use helps enhance security analytics.

IBAT is broader than traditional BAS. IBAT includes AI, IoT, cloud platforms, analytics, and integrated digital intelligence across multiple building functions. However, BAS focuses on core building control systems.

Download Sample Report of Intelligent Building Automation Technologies Market

Please fill out the form to request a customized copy of the research report.