Indoor Location Market Share, Size, Trends, Industry Analysis Report, By Component (Hardware, Solutions, Services), By Technology (BLE, UWB, Wi-Fi, RFID), By Application, By End-User; By Region; Segment Forecast, 2022 - 2030

- Published Date:Jan-2022

- Pages: 118

- Format: PDF

- Report ID: PM2158

- Base Year: 2021

- Historical Data: 2018 - 2020

Report Outlook

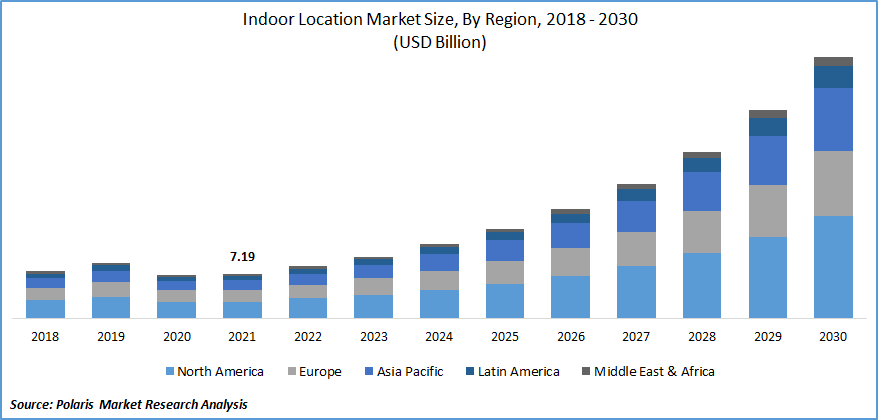

The global indoor location market was valued at USD 7.19 billion in 2021 and is expected to grow at a CAGR of 22.3% during the forecast period. The consistent support from government authorities for improving public safety increased the proliferation of smartphones, coupled with GPS technology in indoor locations, which are expected to drive the indoor location market growth over the forecast period.

Know more about this report: request for sample pages

Know more about this report: request for sample pages

In addition, rising awareness of the government to provide smart services to its citizens. Apart from this, the rising number of applications powered by beacons and BLE tags, along with the favorable government initiatives relating to digital transformation, is also augmenting the growth outlook for the indoor location market.

The recent outbreak of the COVID-19 pandemic is extensive around the world, tapping communities, countries, and societies under massive pressure. Despite this, the pandemic does not severely impact the industry since manufacturers leverage the utility for indoor locations for better facility management, virus tracking, and smart quarantining service to people globally. In particular, businesses offering solutions and services are gaining wider adoption even in the pandemic scenario, which eventually creates a huge demand for the product.

Know more about this report: request for sample pages

Market Dynamics

Growth Drivers

In recent years, the growing proliferation of smartphones with sophisticated mobile applications, along with the ongoing trend of digitalization, mobile commerce, and technological advancements, are contributing to the industry's higher growth. The advent of indoor location systems has offered enterprises increased accuracy across different industrial venues, despite the dimension and area of the facility.

In addition to this, the system has helped several manufacturing units tackle their floor level efficiently. Thus, the indoor location plays a significant role in bringing greater agility and improving efficiency, speed, responsibility, and reliability to manage the industrial datasets.

In addition, the integration of IoT technology further enhances utility for indoor locations to support better tracking of any object and improved customer engagement. As per the International Data Corporation, in 2019, the United States dominated the IoT market with a value of USD 194 billion. China is to be second leading by almost spending of USD 182 billion. In comparison, Germany surpasses the IoT development and spending with USD 35.5 billion across Europe, followed by France (USD 25.6 billion) and the UK (USD 25.5 billion), as per the International Data Corporation. Thus, the increased pool of investment for advanced technologies creates the adoption of indoor locations, which eventually accelerates the market growth.

Report Segmentation

The market is primarily segmented on the basis of component, technology, application, end-user, and region.

|

By Component |

By Technology |

By Application |

By End-User |

By Region |

|

|

|

|

|

Know more about this report: request for sample pages

Insight by End-User

In 2021, the transportation & logistics segment held a large revenue size in the global market, owing to the extensive requirement for providing better mobility support to passengers at airports and railway stations to navigate them in the right direction and right place. In addition, indoor location is also gaining wide popularity in transportation & logistics as it brings facilities to identify customer behavior, provide valuable information that helps in building magnified advertising campaigns, and optimize services.

On the contrary, the retail and e-commerce segment is projected to register a significant growth rate in the overall market. Factors such as the rise in the presence of e-commerce transactions in the retail sector to provide exceptional customer experience, along with the growing focus of e-commerce companies to provide additional benefits for promoting efficiency in business operations, are likely to act as a key factor for driving the market growth worldwide.

Geographic Overview

Geographically, North America dominated the global market in 2020 and is estimated for the significant revenue share on account of the rising indoor location adoption to improve resource utilization and asset tracking facilities. Furthermore, the region also has a large availability of vendors and organizations with extensive business operations and customers, further contributing to the region's higher market growth.

Rising investments in the development of various technologies and applications of indoor locations, coupled with increasing implementation and acceptance of BLE beacons technology, are a few factors that considerably pave the market growth in the region.

For instance, in 2018, the top Venture Capital investors in the IoT tech space were Baidu, Amazon Alexa Fund, Robert Bosch, Intel Capital, Khosla Ventures, Parkwalk Advisors, Northern Light Venture Capital, General Catalyst Partners, Andreessen Horowitz, and GV Management. The investors participated in 52 funding rounds, equating to a total proportionate investment of USD 350.2 million in 2018. Such investments in technology development are responsible for the high adoption of an indoor location in the region.

Moreover, Asia-Pacific is projected to observe a significant growth rate over the forecast period of 2022-2029. Asian countries have undergone the most remarkable transformation initiatives regarding digital technology across enterprises and different industry verticals in the last few years. The growth of industries, particularly the retail, transportation, and communication sectors, is gaining massive momentum, creating a lucrative demand for indoor locations.

In addition, several companies and institutes are stepping up to unveil sophisticated BLE modules. For instance, in 2018, the Tokyo Institute of Technology launched a "Bluetooth Low-Energy transceiver" with comparatively low power consumption for use in the popular 2.4 GHz band. This new BLE transceiver set a breakthrough to accelerate the widespread development of indoor locations in Japan and the overall Asian region.

Competitive Insight

Some of the major players operating in the global market include Acuity Brands, AiRISTA, Apple, Azitek, CenTrak, Cisco, Esri, Google, HERE, HID Global, HPE, Infsoft, InnerSpace, Inpixon, Kontakt.io, Mapxus, Microsoft, Mist, Navenio, Navigine, Oriient, Polaris Wireless, Pozyx, Quuppa, SITUM, Sonitor, STANLEY Healthcare, Syook, Ubisense, and Zebra Technologies.

Indoor Location Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2021 |

USD 7.19 billion |

|

Revenue forecast in 2030 |

USD 42.34 billion |

|

CAGR |

22.3% from 2022 - 2030 |

|

Base year |

2021 |

|

Historical data |

2018 - 2020 |

|

Forecast period |

2022 - 2030 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2022 to 2030 |

|

Segments covered |

By Component, By Technology, By Application, By End-User, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Acuity Brands, AiRISTA, Apple, Azitek, CenTrak, Cisco, Esri, Google, HERE, HID Global, HPE, Infsoft, InnerSpace, Inpixon, Kontakt.io, Mapxus, Microsoft, Mist, Navenio, Navigine, Oriient, Polaris Wireless, Pozyx, Quuppa, SITUM, Sonitor, STANLEY Healthcare, Syook, Ubisense, and Zebra Technologies. |

© 2025 Polaris Market Research and Consulting. All rights reserved