Idiopathic Pulmonary Fibrosis Treatment Market Size, Share, Trends, Industry Analysis Report: By Drug Class, Route of Administration, Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Oct-2024

- Pages: 118

- Format: PDF

- Report ID: PM5148

- Base Year: 2024

- Historical Data: 2020-2023

Idiopathic Pulmonary Fibrosis Treatment Market Overview

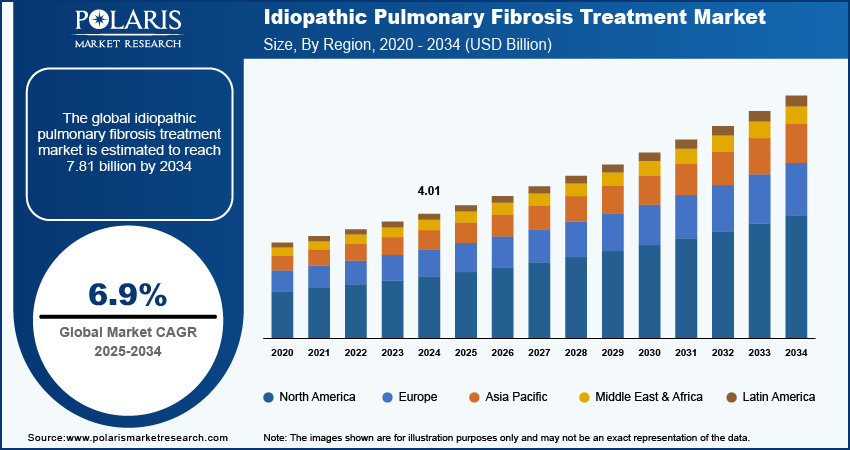

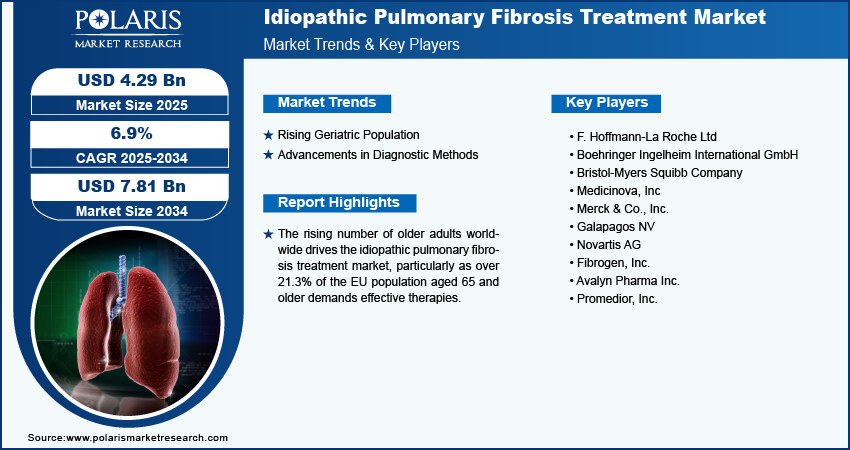

The idiopathic pulmonary fibrosis treatment market size was valued at USD 4.01 billion in 2024. The market is projected to grow from USD 4.29 billion in 2025 to USD 7.81 billion by 2034, exhibiting a CAGR of 6.9% during 2025–2034.

Idiopathic Pulmonary Fibrosis (IPF) is a chronic lung disease characterized by progressive scarring of lung tissue. The scarring causes difficulty in breathing and decreases oxygen supply. The term "idiopathic" indicates that the exact cause of the condition is unknown, although factors such as age, smoking, and genetic predisposition may lead to the condition.

To Understand More About this Research: Request a Free Sample Report

The increasing prevalence of idiopathic pulmonary fibrosis (IPF) is significantly driving the idiopathic pulmonary fibrosis treatment market growth. As more patients are diagnosed with idiopathic pulmonary fibrosis, the demand for effective treatment is on the rise. For instance, according to the National Institute of Health, in 2021, the prevalence of IPF was 36 people in a group of 100,000 people in United States. Enhanced awareness and improved diagnostic methods have led to earlier identification of the disease, resulting in a growing patient population seeking effective therapies. Thus, the growing prevalence of idiopathic pulmonary fibrosis, coupled with improved diagnostic methods, is positively impacting the growth of the idiopathic pulmonary fibrosis treatment market.

The idiopathic pulmonary fibrosis treatment market is growing due to changing lifestyle habits, particularly increased smoking rates and exposure to environmental pollutants. Riskier behaviors, such as smoking tobacco and using recreational drugs, along with occupational exposure to harmful substances like asbestos and industrial chemicals, are contributing to a rise in the incidence of idiopathic pulmonary fibrosis (IPF). The increasing awareness of these lifestyle-related risk factors is further fueling the demand for effective IPF treatments, driving market growth.

Idiopathic Pulmonary Fibrosis Treatment Market Drivers

Rising Geriatric Population

Elderly individuals are more susceptible to pulmonary fibrosis due to age-related loss of protective stem cells and pericytes, which can lead to fibroblast activation and proliferation. As the global population ages, the incidence of idiopathic pulmonary fibrosis increases. For instance, the European Commission reported that over 21.3% of the European Union's population was older than 65 years. This significant portion of the population highlights the potential risk of IPF, which drives the demand for effective treatment methods. Thus, the increasing population of older adults worldwide boosts the idiopathic pulmonary fibrosis treatment market expansion.

Advancements in Diagnostic Methods

Advancements in diagnostic methods are significantly driving growth in the idiopathic pulmonary fibrosis (IPF) treatment market. Improved imaging techniques, such as high-resolution computed tomography (HRCT), enable earlier and more accurate detection of IPF, facilitating timely intervention.

Additionally, the development of biomarker testing and genetic profiling helps identify at-risk populations, enhancing personalized treatment approaches. These innovations not only improve diagnostic accuracy but also increase awareness among healthcare providers and patients about the disease. As early diagnosis leads to better management and treatment outcomes, the demand for effective therapies in the IPF market continues to rise, further propelling its growth.

Idiopathic Pulmonary Fibrosis Treatment Market Segment Insights

Idiopathic Pulmonary Fibrosis Treatment Market – Route of Administration Insights

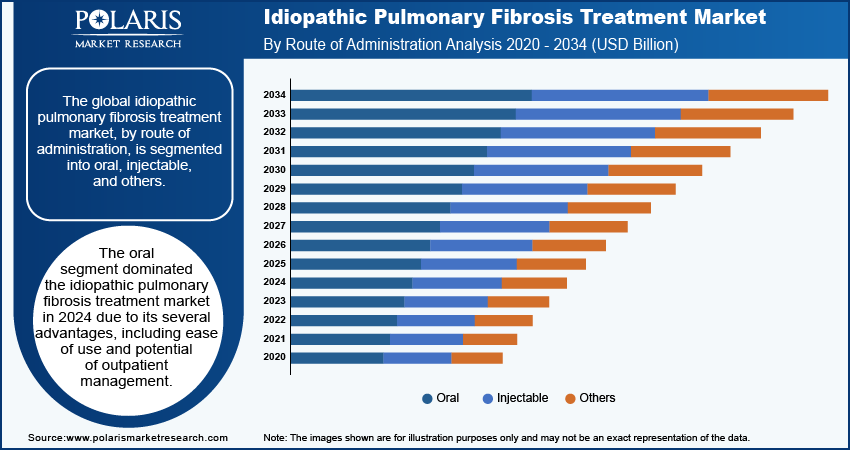

The idiopathic pulmonary fibrosis treatment market, based on route of administration, is segmented into oral, injectables, and others. The oral segment is expected to experience the highest CAGR in the global market during the forecast period. Oral medications have several advantages, including ease of use, improved patient compliance, and the potential for outpatient management. As awareness of idiopathic pulmonary fibrosis increases and more therapies receive approval, the oral route is likely to become the major choice due to its convenience and effectiveness.

Idiopathic Pulmonary Fibrosis Treatment Market – Distribution Channel Insights

The idiopathic pulmonary fibrosis treatment market segmentation, based on distribution channel, includes hospital pharmacies, retail pharmacies, and others. The hospital pharmacies segment dominated the market in 2023. This is due to the rise in specialized treatment protocols tailored for IPF patients. Hospitals increasingly employ multidisciplinary teams to manage complex cases, ensuring that patients receive comprehensive care. This collaborative approach enhances treatment outcomes and improves patient satisfaction. Additionally, hospital pharmacies are better equipped to manage and dispense medication for advanced therapies, such as antifibrotic medications, which often require careful monitoring and adjustment. The focus on patient-centered care in hospitals further solidifies this segment's role, making it a critical component in the management of idiopathic pulmonary fibrosis.

Idiopathic Pulmonary Fibrosis Treatment Market Regional Insights

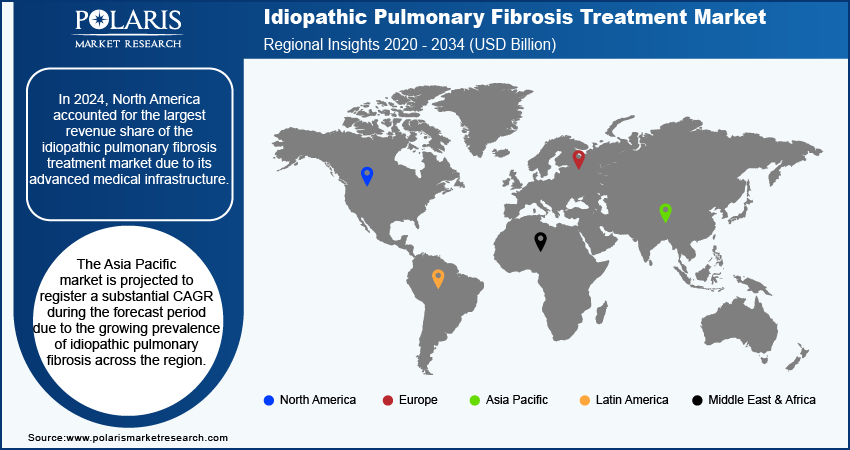

By region, the study provides the idiopathic pulmonary fibrosis treatment market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America accounted for the largest revenue share of the global idiopathic pulmonary fibrosis treatment market due to its advanced medical infrastructure. According to the American Hospital Association and Government of Canada, the region has 6,742 hospitals and offers specialized care and innovative therapies. This allows patients access to advanced treatments and clinical trials. Additionally, strong healthcare policies and a focus on research and development also contribute to the idiopathic pulmonary fibrosis treatment market growth in North America.

The Asia Pacific market is projected to register a substantial CAGR during the forecast period due to the growing prevalence of idiopathic pulmonary fibrosis. For instance, according to the National Institute of Health, the prevalence of idiopathic pulmonary fibrosis ranges from 0.57 to 4.51 per 10,000 people. This increasing incidence is driving the demand for effective treatment options and healthcare infrastructure. Growing awareness and advanced diagnostic methods are expected to fuel the market growth in Asia Pacific during the forecast period.

The idiopathic pulmonary fibrosis treatment market in India is poised for significant growth due to the increased investments in its pharmaceutical manufacturing sector. According to Invest India, the pharmaceutical sector accounts for 3.32% of the total Foreign Direct Investment (FDI) influx, attracting significant resources for research and development. Improved manufacturing capabilities and innovation in drug formulations are expected to improve the availability of effective treatments for idiopathic pulmonary fibrosis, which would boost the idiopathic pulmonary fibrosis market growth in India during the forecast period.

Idiopathic Pulmonary Fibrosis Treatment Market – Key Players and Competitive Insights

The idiopathic pulmonary fibrosis treatment market is evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, advanced manufacturing technologies, and significant capital to maintain a competitive edge. These companies pursue strategic initiatives such as mergers, acquisitions, partnerships, and collaborations to enhance their drug class offerings and expand into new markets.

New companies are positively impacting the industry by introducing innovative medical devices and meeting the needs of specific market sectors. This competitive environment is amplified by continuous progress in drug class offerings and new routes of administration, greater emphasis on sustainability, and the rising requirement for tailor-made single-use drug classes. A few major players in the idiopathic pulmonary fibrosis treatment market are F. Hoffmann-La Roche Ltd; Boehringer Ingelheim International GmbH; Bristol-Myers Squibb Company; Medicinova, Inc; Merck & Co., Inc.; Galapagos NV; Novartis AG; and Fibrogen, Inc.

Roche, officially known as F. Hoffmann-La Roche Ltd, is a biotechnology firm dedicated to advancing medical solutions for various significant ailments. Its focus encompasses the development of drugs and diagnostic tools to combat major diseases, such as cancer, autoimmune disorders, central nervous system conditions, eye-related afflictions, infectious ailments, and respiratory issues. Roche also provides comprehensive diabetes management solutions, in vitro diagnostic systems, and advanced cancer diagnostics based on tissue analysis. The company's operational structure revolves around two key segments: diagnostics and pharmaceuticals. Under the pharmaceutical domain, it concentrates on creating innovative medications in oncology, immunology, ophthalmology, infectious diseases, and neuroscience. Roche specializes in disease identification via in vitro diagnostic procedures in the diagnostic realm. Roche's pursuits extend to pioneering research and exploration of novel disease prevention, detection, and treatment strategies. Its broad range of offerings caters to diverse stakeholders, including hospitals, commercial laboratories, healthcare practitioners, researchers, and pharmacists.

Novartis AG is a Swiss pharmaceutical corporation headquartered in Basel, Switzerland. Established in 1996 from the merger of Ciba-Geigy and Sandoz. The company focuses on medicines, generic pharmaceuticals, vaccines, and consumer health products, reaching over 250 million patients worldwide. The company has a workforce of ∼98,000 associates across more than 140 countries. It has research and development facilities in areas such as oncology, cardiology, and immunology. Notable products include Gleevec for cancer treatment and Entresto for heart failure. Novartis operates through distinct divisions, which include innovative medicines and Sandoz (its generics division).

Key Companies in Idiopathic Pulmonary Fibrosis Treatment Market

- F. Hoffmann-La Roche Ltd

- Boehringer Ingelheim International GmbH

- Bristol-Myers Squibb Company

- Medicinova, Inc

- Merck & Co., Inc.

- Galapagos NV

- Novartis AG

- Fibrogen, Inc.

- Avalyn Pharma Inc.

- Promedior, Inc.

Idiopathic Pulmonary Fibrosis Treatment Industry Developments

October 2024: Bristol Myers Squibb announced that the FDA granted Breakthrough Therapy Designation for BMS-986278, an oral LPA1 antagonist, for progressive pulmonary fibrosis. The designation followed positive results from a Phase 2 study demonstrating significant efficacy and safety in patients.

November 2023: LevitasBio introduced the LeviCell EOS system, a new advancement in cell isolation and enrichment developed in collaboration with Planet Innovation. Launched mid-year, the LeviCell EOS builds on the Levitation Technology of its predecessor, LeviCell 1.0, offering higher throughput with the ability to process four samples simultaneously and connect up to four modules. The system features real-time analysis software and a flexible design with interchangeable modules. Early installations at leading research labs highlight its impact on sample processing and characterization.

Idiopathic Pulmonary Fibrosis Treatment Market Segmentation

By Drug Class Outlook (USD Billion, 2020–2034)

- Pirfenidone

- Nintedanib

- Interferon Gammato1b

- Others

By Route of Administration Outlook (USD Billion, 2020–2034)

- Oral

- Injectable

- Others

By Distribution Channel Outlook (USD Billion, 2020–2034)

- Hospital Pharmacies

- Retail Pharmacies

- Others

By Regional Outlook (USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Idiopathic Pulmonary Fibrosis Treatment Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 4.01 billion |

|

Market Size Value in 2025 |

USD 4.29 billion |

|

Revenue Forecast by 2034 |

USD 7.81 billion |

|

CAGR |

6.9% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Distribution Channel |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The idiopathic pulmonary fibrosis treatment market size was valued at USD 4.01 billion in 2024 and is projected to grow to USD 7.81 billion by 2034.

The global market is projected to register a CAGR of 6.9% during the forecast period

North America accounted for the largest share of the global market in 2024.

A few key players in the market are F. Hoffmann-La Roche Ltd; Boehringer Ingelheim International GmbH; Bristol-Myers Squibb Company; Medicinova, Inc; Merck & Co., Inc.; Galapagos NV; Novartis AG; and Fibrogen, Inc.

The oral segment is anticipated to record a significant CAGR in the global market during the forecast period. This growth is attributed to its several advantages, including ease of use and potential of outpatient management.

The hospital pharmacy segment dominated the market in 2024 due to increasing hospitalization rates and the availability of specialized care for patients requiring advanced treatments.

© 2025 Polaris Market Research and Consulting. All rights reserved