Hyper-Adaptive Virtual Reality Environments Market Size, Share, Trends, Industry Analysis Report: By Component (Hardware and Software), Technology, Device Type, Application, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Apr-2025

- Pages: 129

- Format: PDF

- Report ID: PM5554

- Base Year: 2024

- Historical Data: 2020-2023

Hyper-Adaptive Virtual Reality Environments Market Overview

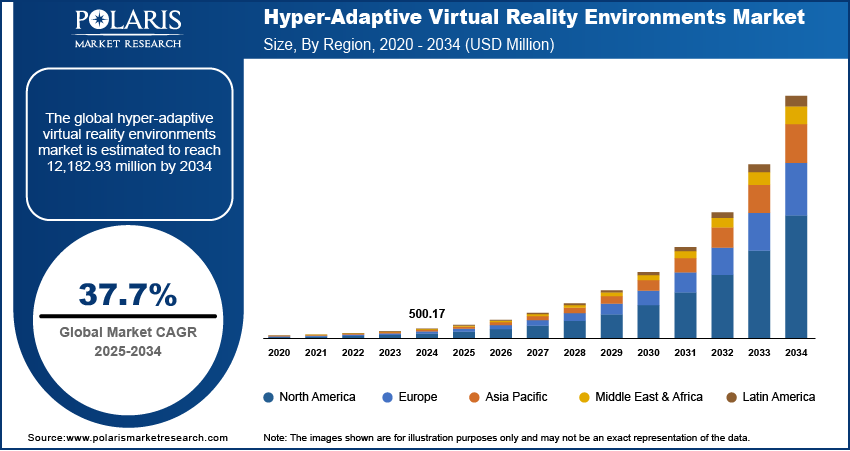

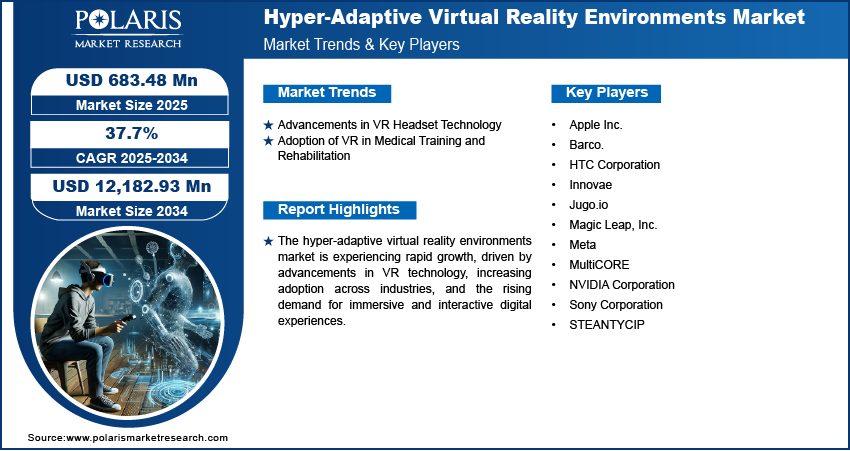

The global hyper-adaptive virtual reality environments market size was valued at USD 500.17 million in 2024. It is expected to grow from USD 683.48 million in 2025 to USD 12,128.29 million by 2034, at a CAGR of 37.7% during 2025–2034.

Hyper-adaptive virtual reality (VR) environments refer to immersive digital spaces that dynamically adjust to user behavior, preferences, and real-time data inputs, improving interactivity and personalization. The hyper-adaptive virtual reality environments market demand is expanding rapidly due to the increasing intersection of VR with the metaverse, a virtual universe where users can engage in social, professional, and entertainment experiences. The integration of VR in metaverse applications is driving the hyper-adaptive virtual reality (VR) environments market demand for more adaptive environments, allowing for real-time content modifications and intelligent interactions. Additionally, businesses and developers are leveraging this technology to create hyper-realistic digital experiences, enabling deeper engagement and interaction across various sectors, such as gaming, education, and retail. In September 2023, Meta launched the Quest 3 mixed reality headset, which allows for immersive experiences such as playing a virtual piano on a coffee table. It offers a 30% increase in visual resolution and a 40% louder audio range compared to Quest 2, while also being thinner and more comfortable to wear.

To Understand More About this Research: Request a Free Sample Report

The development of virtual workspaces for remote collaboration is reshaping the way organizations operate in a digitally connected world, which boosts the hyper-adaptive virtual reality environments market growth. Companies are investing in VR-driven solutions that improve real-time collaboration, spatial computing, and interactive meetings as hybrid and remote work models gain traction. In June 2024, AWS launched Amazon WorkSpaces Pools, allowing cost savings by sharing virtual desktops among users, with fresh desktops upon login. Ideal for training labs and contact centers, it supports personalization via central storage. The features include simplified management, Microsoft 365 integration, auto-scaling, and pay-as-you-go pricing for flexibility and efficiency. These environments allow seamless integration of digital tools, creating immersive virtual offices that replicate physical workspaces while improving productivity and engagement. The growing emphasis on flexible work solutions is fueling innovation in hyper-adaptive VR environments, making them a crucial component of the evolving digital workplace.

Hyper-Adaptive Virtual Reality Environments Market Dynamics

Advancements in VR Headset Technology

The advancements, such as the development of high-resolution displays, wider fields of view, reduced latency, and improved motion tracking, have especially increased consumption and realism in virtual environments, as they improve the overall user experience through improved hardware capabilities. In May 2022, Zero Latency collaborated with HTC to launch a multiplayer VR platform. Using the HTC VIVE Focus 3 headset, up to eight players can enjoy 5K VR experiences without backpacks or sensors, offering a highly immersive gaming experience. These advancements enable hyper-adaptive systems to respond more effectively to user interactions, ensuring a seamless and real experience. Additionally, the integration of AI-driven features, lightweight designs, and wireless capabilities has made VR more accessible and practical for various industries, ranging from gaming and enterprise solutions to education and training. Therefore, as hardware continues to evolve, the potential for creating highly responsive and adaptive virtual environments grows. Thus, advancements in VR headset technology are accelerating the hyper-adaptive virtual reality (VR) environments market development.

Adoption of VR in Medical Training and Rehabilitation

The adoption of VR in medical training and rehabilitation revolutionizes the way healthcare professionals and patients engage with virtual environments. For instance, in June 2022, MediSim VR launched India’s first fully automated VR lab at PIMS, improving medical student's medical skills. The lab combines VR, simulation, and AI-powered assessments, offering immersive training modules such as virtual patients and situational scenarios for healthcare professionals. Additionally, hyper-adaptive VR systems provide dynamic and interactive simulations, allowing students and professionals to practice procedures, refine skills, and improve decision-making in a risk-free setting. In rehabilitation, VR-based therapy adapts to patient progress, offering personalized treatment plans and real-time feedback to improve recovery outcomes. The ability to create immersive, data-driven environments tailored to individual needs is transforming medical education and patient care, making hyper-adaptive VR an essential tool in modern healthcare solutions.

Hyper-Adaptive Virtual Reality Environments Market Segment Assessment

Hyper-Adaptive Virtual Reality Environments Market Assessment by Application Outlook

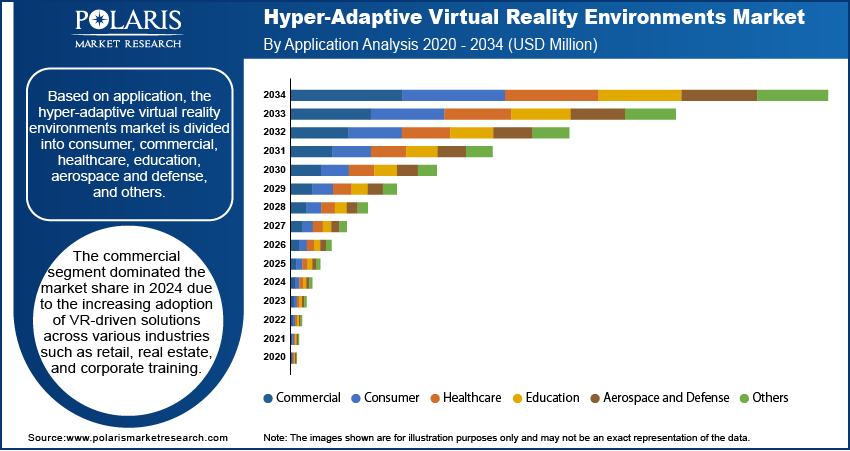

The global hyper-adaptive virtual reality environments market segmentation, based on application, includes consumer, commercial, healthcare, education, aerospace and defense, and others. The commercial segment dominated the hyper-adaptive virtual reality environments market share in 2024 due to the increasing adoption of VR-driven solutions across industries such as retail, real estate, and corporate training. Businesses are leveraging hyper-adaptive VR environments to create immersive customer experiences, improve employee engagement, and optimize operational efficiency. Virtual showrooms, interactive product demonstrations, and AI-driven VR simulations have gained traction as companies seek innovative ways to engage consumers and streamline workflows. Additionally, the integration of VR into enterprise collaboration tools and training modules has accelerated its adoption, positioning the commercial sector as the leading contributor to the hyper-adaptive virtual reality environments market growth.

Hyper-Adaptive Virtual Reality Environments Market Evaluation by Technology Outlook

The global hyper-adaptive virtual reality environments market segmentation, based on technology, includes non-immersive, semi-immersive, and fully-immersive. The non-immersive segment is expected to witness substantial growth during the forecast period driven by its accessibility, cost-effectiveness, and ease of integration. Unlike fully immersive VR, which requires specialized headsets and advanced hardware, non-immersive VR solutions operate through standard computer interfaces, making them more practical for widespread use. Industries such as education, corporate training, and healthcare are increasingly utilizing non-immersive VR applications for simulations, remote learning, and data visualization. The ability to deliver adaptive virtual experiences without requiring extensive infrastructure investments makes this technology attractive for organizations seeking scalable and efficient solutions.

Hyper-Adaptive Virtual Reality Environments Market Outlook by Region

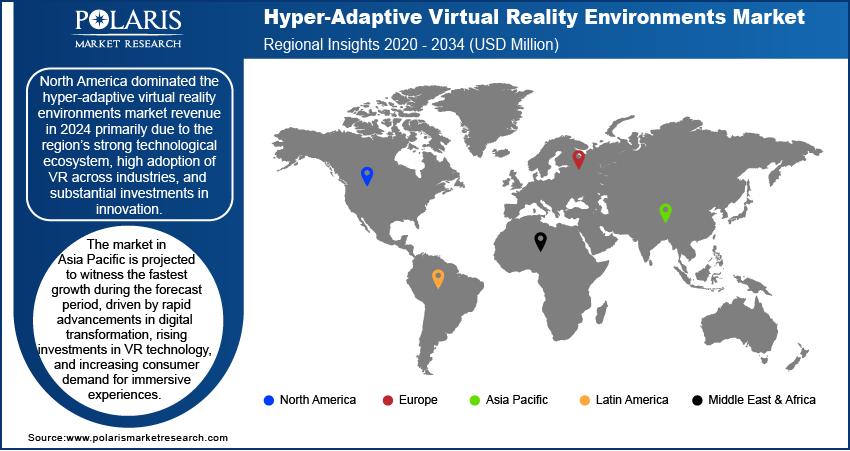

By region, the report provides the hyper-adaptive virtual reality environments market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the market share in 2024 primarily due to the region’s strong technological ecosystem, high adoption of VR across industries, and substantial investments in innovation. The presence of leading VR technology developers, combined with advanced research and development capabilities, has driven the hyper-adaptive virtual reality environments market expansion in North America. In February 2025, Microsoft and Anduril Industries expanded their collaboration for the US Army’s IVAS program, integrating AR/VR to improve combat effectiveness. Anduril will oversee production and development, while Microsoft Azure supports AI and cloud infrastructure for real-time battlefield insights and mission command. Furthermore, the integration of VR in sectors such as healthcare, gaming, and enterprise solutions has been fueled by increasing demand for interactive and adaptive digital experiences. Supportive government initiatives, a well-established digital infrastructure, and the region’s strong consumer base further contribute to North America’s leadership in the market.

The Asia Pacific hyper-adaptive virtual reality environments market is projected to witness the fastest growth during the forecast period, driven by rapid advancements in digital transformation, rising investments in VR technology, and increasing consumer demand for immersive experiences. The expansion of industries such as gaming, education, and healthcare in countries such as China, Japan, and South Korea has created a strong demand for adaptive VR solutions. Additionally, government initiatives supporting smart infrastructure, coupled with the growing presence of tech startups and enterprises adopting VR for commercial applications, are accelerating market growth. Thus, as accessibility to advanced VR technologies improves, the region is expected to play a crucial role in shaping the future of hyper-adaptive virtual environments.

Hyper-Adaptive Virtual Reality Environments Market – Key Players & Competitive Analysis Report

The competitive landscape features a mix of global leaders and regional players aiming to hold a significant share of the hyper-adaptive virtual reality (VR) environments market through innovation, strategic partnerships, and geographic expansion. Global companies such as Meta (Oculus), Microsoft, HTC Vive, and others dominate the market with advanced R&D capabilities, advanced hardware, and software solutions. These players focus on delivering hyper-adaptive VR environments that dynamically adjust to user behavior, preferences, and real-time data, improving immersion and personalization. Hyper-adaptive virtual reality (VR) environments market trends highlight increasing demand for AI-driven adaptive systems, biometric integration, and real-time content generation, reflecting advancements in VR technology and user experience. The market is projected to grow, driven by rising adoption in gaming, healthcare, education, and enterprise applications. Regional players are gaining traction by addressing localized needs, particularly in emerging markets, due to growing tech adoption and investments in VR infrastructure. Competitive strategies include mergers and acquisitions, collaborations with tech innovators, and the launch of next-gen VR products tailored to diverse industries. These efforts emphasize the importance of technological innovation, market adaptability, and regional investments in fueling the hyper-adaptive VR environments market expansion. A few key major players are Meta; Sony Corporation; HTC Corporation; Apple Inc.; NVIDIA Corporation; Magic Leap, Inc.; MultiCORE; STEANTYCIP; Barco; Jugo.io; and Innovae.

Meta Platforms Inc., formerly known as Facebook, Inc., is a multinational technology company headquartered in Menlo Park, California. Meta owns and operates social media and messaging applications such as Facebook, Instagram, Threads, and WhatsApp. Meta's mission is centered around building the future of human connection and the technologies that facilitate these connections. Mark Zuckerberg, Meta's CEO, has outlined the company's direction for 2025, emphasizing advancements in artificial intelligence (AI), expansion of data centers, and metaverse development. Meta is focused on building the metaverse, described as a digital extension of the physical world through social media, virtual reality, and augmented reality features. The company is investing in data center infrastructure to position itself for long-term technological leadership, which could revolutionize how fashion brands engage with consumers through social commerce and virtual experiences.

HTC Corporation is a Taiwanese consumer electronics company that focuses on creating innovative products in the mobile and immersive technology space. Founded in 1997 by Cher Wang and H. T. Cho, HTC initially manufactured notebook computers before transitioning to designing touch and wireless handheld devices. The company is headquartered in Taoyuan District, Taoyuan, Taiwan. HTC's product portfolio includes smartphones, business solutions, virtual reality systems, extended reality ecosystems, 3D tracking systems, motion capture systems, digital art platforms, and healthcare technologies. In recent years, HTC has diversified its business beyond smartphones, partnering with Valve to produce the HTC Vive virtual reality platform. HTC is applying its innovative approach to connected devices as it enters the era of VIVERSE. VIVERSE is the convergence of VR, AR, 5G, AI, and blockchain technologies. HTC is dedicated to creating human-centered technology that improves imagination and provides powerful hardware, platforms, tools, and services to customers.

List of Key Companies in Hyper-Adaptive Virtual Reality Environments Market

- Apple Inc.

- Barco.

- HTC Corporation

- Innovae

- Jugo.io

- Magic Leap, Inc.

- Meta

- MultiCORE

- NVIDIA Corporation

- Sony Corporation

- STEANTYCIP

Hyper-Adaptive Virtual Reality Environments Industry Developments

In January 2024, Virtalis launched first multi-point of view (MPOV) VR experience on a fine pixel pitch LED display (1.2mm), enabling two users to interact simultaneously. It offers high-resolution, scalable, and sustainable immersive environments for collaboration, training, and design.

In May 2024, TD Bank Group (TD) launched new immersive virtual reality (VR) tools that allow colleagues to engage with peers and simulate everyday customer interactions.

Hyper-Adaptive Virtual Reality Environments Market Segmentation

By Component Outlook (Revenue, USD Million, 2020–2034)

- Hardware

- Software

By Technology Outlook (Revenue, USD Million, 2020–2034)

- Non-Immersive

- Semi-Immersive

- Fully-Immersive

By Device Type Outlook (Revenue, USD Million, 2020–2034)

- Head-Mounted Displays (HDMs)

- Gesture-Tracking Devices

- Projectors and Display Walls

By Application Outlook (Revenue, USD Million, 2020–2034)

- Consumer

- Commercial

- Healthcare

- Education

- Aerospace and Defense

- Others

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Hyper-Adaptive Virtual Reality Environments Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 500.17 million |

|

Market Size Value in 2025 |

USD 683.48 million |

|

Revenue Forecast in 2034 |

USD 12,182.93 million |

|

CAGR |

37.7% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD Million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global hyper-adaptive virtual reality environments market size was valued at USD 500.17 million in 2024 and is projected to grow to USD 12,128.29 million by 2034.

The global market is projected to register a CAGR of 37.7% during the forecast period.

North America dominated the market revenue in 2024.

A few of the key players in the market are Meta; Sony Corporation; HTC Corporation; Apple Inc.; NVIDIA Corporation; Magic Leap, Inc.; MultiCORE; STEANTYCIP; Barco; Jugo.io; and Innovae.

The commercial segment dominated the market share in 2024.

© 2025 Polaris Market Research and Consulting. All rights reserved