Head and Neck Cancer Market Size, Share, Trends, Industry Analysis Report: By Therapy Type (Chemotherapy, Immunotherapy, and Targeted Therapy), Route of Administration, Distribution Channel, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Mar-2025

- Pages: 114

- Format: PDF

- Report ID: PM1330

- Base Year: 2024

- Historical Data: 2020-2023

Head and Neck Cancer Market Overview

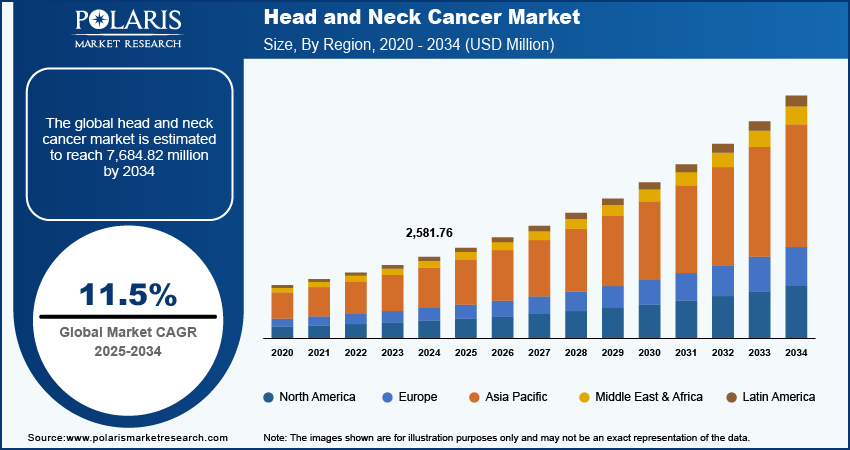

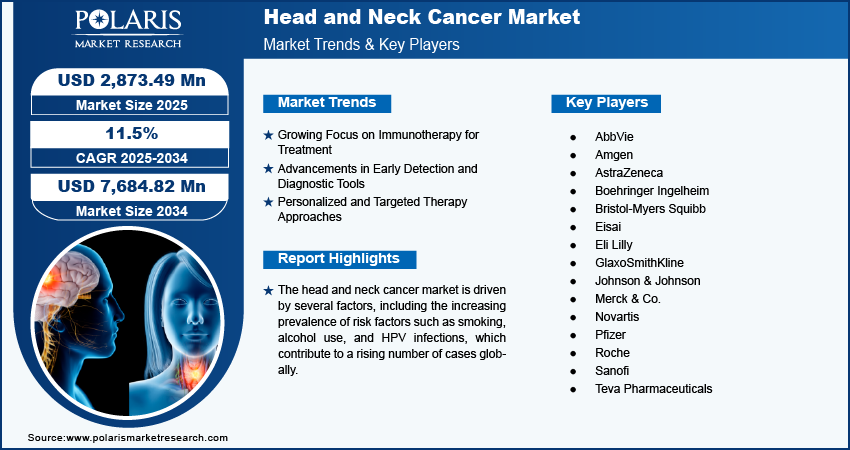

The head and neck cancer market size was valued at USD 2,581.76 million in 2024. The market is projected to grow from USD 2,873.49 million in 2025 to USD 7,684.82 million by 2034, exhibiting a CAGR of 11.5% during 2025–2034.

The head and neck cancer market refers to the segment of the healthcare industry focused on the prevention, diagnosis, treatment, and management of cancers affecting head and neck, including the oral cavity, pharynx, larynx, and sinuses. The increasing prevalence of risk factors such as smoking, alcohol consumption, and human papillomavirus (HPV) infections, which contribute to the rise in cancer cases, drives the market growth. Advances in diagnostic techniques, such as imaging and molecular testing, are improving early detection and treatment outcomes. Additionally, the development of targeted therapies, immunotherapies, and minimally invasive surgical procedures is driving growth in the market. Head and neck cancer market trends include a shift toward personalized treatment approaches, increased focus on combination therapies, and the integration of artificial intelligence in diagnosis and treatment planning.

To Understand More About this Research: Request a Free Sample Report

Head and Neck Cancer Market Dynamics

Growing Focus on Immunotherapy for Treatment

One of the significant trends in the head and neck cancer market is the increasing focus on immunotherapy as a treatment option. Immunotherapies, such as immune checkpoint inhibitors, have shown promising results in improving survival rates and reducing recurrence in patients with advanced head and neck cancers. Drugs such as pembrolizumab and nivolumab, which target PD-1/PD-L1 pathways, are gaining traction in the treatment of recurrent or metastatic squamous cell carcinoma of the head and neck (SCCHN). In a study published by the American Society of Clinical Oncology (ASCO), pembrolizumab demonstrated a survival benefit compared to traditional chemotherapy. This shift toward immunotherapy is attributed to its ability to offer more targeted treatment with fewer side effects, contributing to the growing adoption of these therapies in clinical settings.

Advancements in Early Detection and Diagnostic Tools

The head and neck cancer market players focus on the development of more advanced diagnostic tools that enable earlier detection of the disease. Early-stage head and neck cancers often present with vague symptoms, making timely diagnosis a challenge. However, innovations in molecular diagnostics, liquid biopsy, and advanced imaging techniques are improving detection rates. For instance, the use of biomarkers and genetic profiling in diagnosing head and neck cancers is helping to identify at-risk patients before clinical symptoms appear. According to a study in The Lancet Oncology, the use of liquid biopsy for detecting HPV-related oropharyngeal cancer has shown early promise. These advancements are crucial for improving outcomes, as earlier detection generally leads to better prognosis and less aggressive treatment. Hence, the advancements in early detection and diagnostics tools boost the head and neck cancer market demand.

Personalized and Targeted Therapy Approaches

Personalized medicine is becoming an essential component of treatment strategies for head and neck cancers. The integration of genomic profiling in treatment planning allows healthcare providers to tailor therapies to individual patients based on their genetic makeup and the molecular characteristics of their tumors. Targeted therapies, such as cetuximab and other monoclonal antibodies, are being increasingly used to address specific mutations found in head and neck cancer cells. This approach improves the precision of treatment and helps in managing the disease more effectively. For example, the targeting of the epidermal growth factor receptor (EGFR) in SCCHN has been shown to enhance treatment efficacy. According to data from the National Cancer Institute, targeted therapies have improved the overall survival and quality of life for many patients suffering from advanced forms of the disease. Thus, the rising personalized and targeted therapy approaches are expected to emerge as head and neck cancer market trends during the forecast period.

Head and Neck Cancer Market Segment Insights

Head and Neck Cancer Market Assessment – Therapy Type-Based Insights

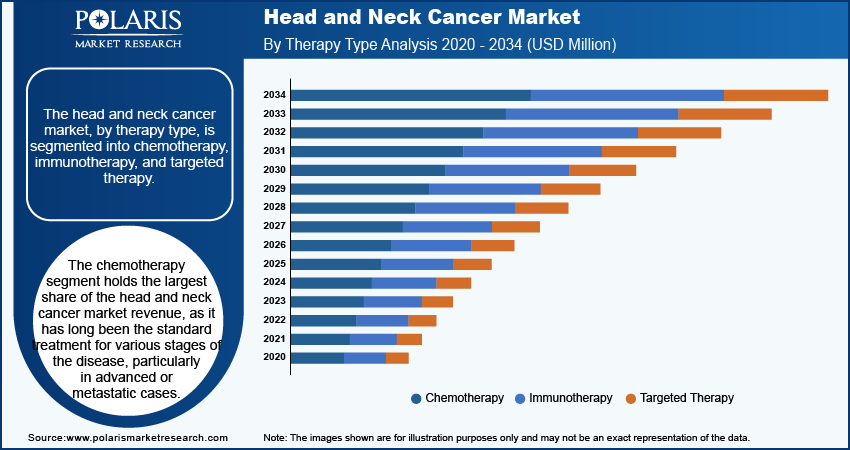

The head and neck cancer market, by therapy type, is segmented into chemotherapy, immunotherapy, and targeted therapy. The chemotherapy segment dominates the head and neck cancer market share, as it has long been the standard treatment for various stages of the disease, particularly in advanced or metastatic cases. It is widely used as a standalone treatment or in combination with radiation therapy. Despite newer therapies, chemotherapy continues to play a central role due to its broad applicability and established efficacy. However, the immunotherapy segment is registering the highest growth, driven by the increasing adoption of immune checkpoint inhibitors, which have shown significant improvements in survival rates for patients affected by recurrent or metastatic head and neck cancers.

The success of drugs such as pembrolizumab and nivolumab, particularly in HPV-positive cancer patients, is a key factor behind the growth of immunotherapy. While chemotherapy dominates in market share, immunotherapy and targeted therapies are expected to witness continued growth as advancements in precision medicine evolve and gain broader clinical acceptance.

Head and Neck Cancer Market Outlook – Route of Administration-Based Insights

The head and neck cancer market, by route of administration, is segmented into injectable and oral. The injectable segment holds a larger share of the head and neck cancer market revenue, primarily due to the widespread use of intravenous (IV) chemotherapy and immunotherapy treatments. Injectable therapies, including immune checkpoint inhibitors and targeted therapies, are commonly used in the treatment of advanced or metastatic cases of head and neck cancer, where efficacy and rapid absorption are critical. These treatments are typically administered in healthcare settings, ensuring careful monitoring of patients during the infusion process.

The oral segment is experiencing significant growth, driven by the increasing availability of oral formulations for targeted therapies and chemotherapy drugs. Oral drugs, offering convenience and improving patient compliance, are gaining popularity for maintenance therapy and in cases where long-term treatment is required, as they allow patients to manage their condition with less frequent hospital visits. The growth in oral administration is expected to continue as pharmaceutical companies focus on developing new oral therapies that match the efficacy of traditional injectables while enhancing the overall treatment experience for patients.

Head and Neck Cancer Market Evaluation – Distribution Channel-Based Insights

The head and neck cancer market, by distribution channel, is segmented into retail & specialty pharmacies, hospital pharmacies, and online pharmacies. The hospital pharmacies segment holds the largest market share, largely due to the specialized nature of cancer treatments, which require close monitoring and administration by healthcare professionals. Hospital pharmacies are critical in providing injectable treatments such as chemotherapy, immunotherapy, and targeted therapies, which are often used in inpatient or outpatient settings. The complex treatment regimens and the need for specialized care contribute to the dominance of this distribution channel. Additionally, the rising number of cancer treatment centers globally supports the continued importance of hospital pharmacies in distributing these drugs.

The online pharmacies segment is experiencing the highest growth, driven by the increasing adoption of e-commerce and home delivery services. The convenience and accessibility of online pharmacies are particularly beneficial for patients who require maintenance therapies or oral medications, offering a streamlined process for prescription fulfillment. The shift toward online platforms is further accelerated by the growing demand for telemedicine and remote healthcare services, allowing patients to receive treatment without needing to visit physical pharmacies.

Head and Neck Cancer Market Regional Insights

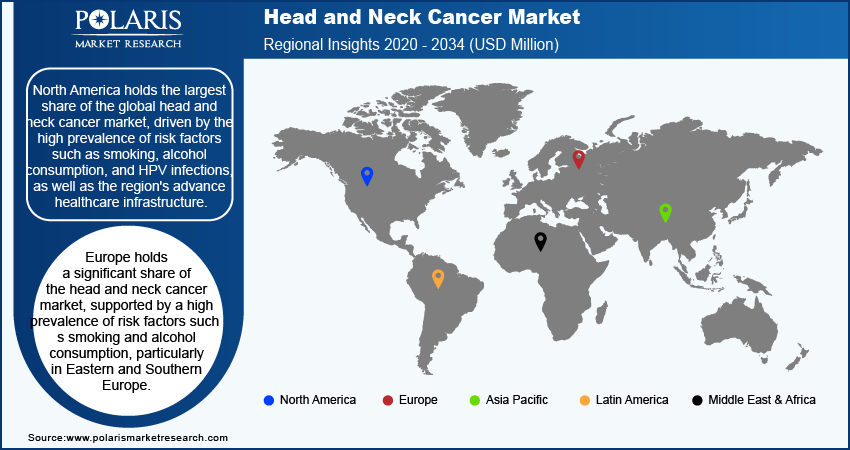

By region, the study provides head and neck cancer market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest share of the global head and neck cancer market revenue, driven by the high prevalence of risk factors such as smoking, alcohol consumption, and HPV infections, as well as the region's advanced healthcare infrastructure. The US, in particular, benefits from a well-established healthcare system, robust funding for cancer research, and the availability of innovative therapies, including immunotherapies and targeted treatments. Furthermore, the presence of key pharmaceutical companies and research institutions contributes to the rapid adoption of innovative treatment options in the region. While Europe and Asia Pacific also exhibit significant market potential, North America's market dominance is largely attributed to its strong healthcare policies, early adoption of new therapies, and high awareness of head and neck cancer prevention and treatment options.

Europe holds a significant share of the head and neck cancer market, supported by a high prevalence of risk factors such as smoking and alcohol consumption, particularly in Eastern and Southern Europe. The region benefits from a strong healthcare infrastructure, with advanced treatment options available, including immunotherapies and targeted therapies. Key countries such as Germany, France, and the UK are leading in terms of market size due to their robust healthcare systems and high adoption of advanced cancer treatments. Furthermore, Europe has a strong focus on early detection and prevention programs, which help improve treatment outcomes. The ongoing research initiatives and collaborations between pharmaceutical companies and academic institutions in Europe are also contributing to the development of innovative therapies for head and neck cancers.

The Asia Pacific head and neck cancer market is expected to experience significant growth, driven by increasing awareness of cancer prevention and improvements in healthcare access, particularly in countries such as China, India, and Japan. The rising prevalence of risk factors such as tobacco use and HPV infections is contributing to the growing cases of head and neck cancers in the region. Additionally, improvements in healthcare infrastructure and rising healthcare spending in emerging markets are enabling better access to advanced cancer treatments. Japan and Australia are among the leading markets in terms of the adoption of modern therapies, while India and China are witnessing increasing adoption of innovative treatments due to expanding healthcare access and the growing burden of cancer. The region is also seeing an increase in clinical trials and research efforts aimed at improving treatment outcomes and expanding the availability of immunotherapy and targeted therapy options.

Head and Neck Cancer Market – Key Players and Competitive Insights

A few key players in the head and neck cancer market include Bristol-Myers Squibb, Merck & Co., Eli Lilly, Roche, AstraZeneca, Novartis, Pfizer, Johnson & Johnson, Sanofi, Boehringer Ingelheim, Amgen, GlaxoSmithKline, AbbVie, Eisai, and Teva Pharmaceuticals. These companies are actively involved in the development, production, and distribution of therapies targeting head and neck cancer. They offer a wide range of treatment options such as chemotherapy, immunotherapy, and targeted therapies. Bristol-Myers Squibb, for example, is known for its immunotherapy offerings such as nivolumab, while Merck & Co. has contributed with pembrolizumab. Roche and AstraZeneca are also key players with their respective therapies for advanced stages of head and neck cancer, while Novartis and Pfizer continue to expand their oncology portfolios. Companies such as Boehringer Ingelheim and Amgen are involved in the development of biologic therapies that target specific cancer pathways, complementing traditional chemotherapy options.

The competitive landscape is shaped by a mix of large pharmaceutical companies with established oncology pipelines and smaller biotech firms focused on innovative treatment approaches. Companies such as Merck & Co. and Bristol-Myers Squibb are emphasizing immunotherapies, which have become a focal point due to their effectiveness in treating various cancers, including head and neck cancers. On the other hand, smaller companies are innovating with targeted therapies and are aiming to capture market share by addressing specific genetic mutations and patient subpopulations. The head and neck cancer market is also witnessing an increasing number of collaborations between pharmaceutical companies and academic institutions to advance the development of new therapies, particularly in the immunotherapy and personalized medicine segments.

There is significant emphasis on expanding the availability of head and neck cancer treatments in emerging markets where the incidence of the disease is rising. In these regions, pharmaceutical companies are focusing on increasing access to both advanced therapies and affordable treatment options. Companies such as Teva Pharmaceuticals are working on generic formulations to provide cost-effective solutions to patients. Additionally, with the rise in digital health tools and telemedicine, some companies are looking into enhancing patient monitoring and adherence to treatment regimens, offering a competitive advantage by integrating technology into the treatment process. As the market evolves, collaborations, research initiatives, and patient-centric approaches will be key factors in shaping the competition.

Bristol-Myers Squibb is a prominent player in the head and neck cancer market, particularly known for its contributions to immunotherapy. The company offers nivolumab (Opdivo), a checkpoint inhibitor used for treating recurrent or metastatic head and neck squamous cell carcinoma. Bristol-Myers Squibb has been focused on advancing cancer treatment options and expanding access to its therapies in various regions.

Merck & Co. is another key player, known for its immunotherapy drug pembrolizumab (Keytruda), which is used in the treatment of various cancers, including head and neck cancers. The company continues to be actively involved in the development of innovative treatments and expanding the indications for its existing therapies. Merck's focus has been on improving survival rates for patients suffering from advanced or metastatic head and neck cancers.

List of Key Companies in Head and Neck Cancer Market

- AbbVie

- Amgen

- AstraZeneca

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Eisai

- Eli Lilly

- GlaxoSmithKline

- Johnson & Johnson

- Merck & Co.

- Novartis

- Pfizer

- Roche

- Sanofi

- Teva Pharmaceuticals

Head and Neck Cancer Industry Developments

- In June 2024, Nivolumab received expanded approval from regulatory authorities in multiple countries for use in first-line treatment for patients affected by head and neck cancer, following positive clinical trial results. This approval is expected to broaden the use of nivolumab in the treatment of this disease.

- In March 2024, Merck announced the successful results of a clinical trial where pembrolizumab showed significant efficacy in combination with chemotherapy for patients suffering from locally advanced head and neck squamous cell carcinoma. This result further strengthened Merck's position in the oncology market and is expected to expand treatment options for patients.

Head and Neck Cancer Market Segmentation

By Therapy Type Outlook

- Chemotherapy

- Immunotherapy

- Targeted Therapy

By Route of Administration Outlook

- Injectable

- Oral

By Distribution Channel Outlook

- Retail & Specialty Pharmacies

- Hospital Pharmacies

- Online Pharmacies

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Head and Neck Cancer Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 2,581.76 million |

|

Market Size Value in 2025 |

USD 2,873.49 million |

|

Revenue Forecast by 2034 |

USD 7,684.82 million |

|

CAGR |

11.5% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy:

The head and neck cancer market has been segmented into detailed segments of therapy type, route of administration, and distribution channel. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy:

The head and neck cancer market growth and marketing strategy is centered around expanding the availability and accessibility of innovative treatments, particularly immunotherapies and targeted therapies. Companies are focusing on strategic collaborations, research partnerships, and clinical trials to advance treatment options and secure regulatory approvals. A key aspect of the strategy includes increasing awareness and education on the disease, particularly in emerging markets where the incidence is rising. Additionally, pharmaceutical companies are emphasizing personalized medicine, offering tailored treatments based on genetic profiling. Digital health tools and telemedicine are also being integrated to enhance patient management and improve treatment adherence.

FAQ's

The head and neck cancer market size was valued at USD 2,581.76 million in 2024 and is projected to grow to USD 7,684.82 million by 2034

The market is projected to register a CAGR of 11.5% during the forecast period.

North America held the largest share of the market in 2024.

A few key players in the head and neck cancer market include Bristol-Myers Squibb, Merck & Co., Eli Lilly, Roche, AstraZeneca, Novartis, Pfizer, Johnson & Johnson, Sanofi, Boehringer Ingelheim, Amgen, GlaxoSmithKline, AbbVie, Eisai, and Teva Pharmaceuticals

The chemotherapy segment accounted for the largest share of the market in 2024

The injectable therapies segment accounted for the largest share of the market in 2024

Head and neck cancer refers to a group of cancers that develop in the tissues and organs of the head and neck region, including the mouth, throat, voice box (larynx), sinuses, and nasal cavity. The most common type of head and neck cancer is squamous cell carcinoma, which arises from the flat cells lining these areas. Risk factors for head and neck cancer include smoking, alcohol consumption, and infection with the human papillomavirus (HPV). Symptoms can vary depending on the location of the cancer and may include a sore throat, difficulty swallowing, a persistent cough, and unexplained weight loss. Early detection and treatment are crucial for improving outcomes, and treatments typically involve a combination of surgery, radiation therapy, chemotherapy, and targeted therapies

A few key trends in the market are described below: Increased focus on immunotherapy: The use of immune checkpoint inhibitors, such as pembrolizumab and nivolumab, is gaining traction due to their ability to improve survival rates and offer better outcomes for patients with advanced cancer. Advancements in early detection: Enhanced diagnostic techniques, including liquid biopsy and advanced imaging, are improving early-stage detection, leading to better treatment outcomes. Personalized treatment approaches: The growing use of genomic profiling and targeted therapies allows for treatments tailored to the individual genetic makeup of patients, improving precision and effectiveness

A new company entering the head and neck cancer market could focus on developing innovative, personalized treatment options through genomic profiling and targeted therapies, which are increasingly in demand for precision medicine. Investing in immunotherapies, particularly immune checkpoint inhibitors, would allow the company to tap into the growing trend of immuno-oncology. Additionally, offering convenient and accessible oral therapies could improve patient compliance and differentiate the company in the market. Expanding into emerging markets with rising cancer rates, such as Asia Pacific, while focusing on early detection and diagnostic tools, could also provide a competitive advantage. Furthermore, leveraging digital health technologies for patient monitoring and treatment management could enhance patient outcomes and loyalty.

Companies manufacturing, distributing, or purchasing head and neck cancer therapy-related products and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved