Autoimmune Disease Diagnostics Market Size, Share, Trends, Industry Analysis Report: By Product, Type, Test Type, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Dec-2024

- Pages: 120

- Format: PDF

- Report ID: PM1299

- Base Year: 2024

- Historical Data: 2020-2023

Autoimmune Disease Diagnostics Market Overview

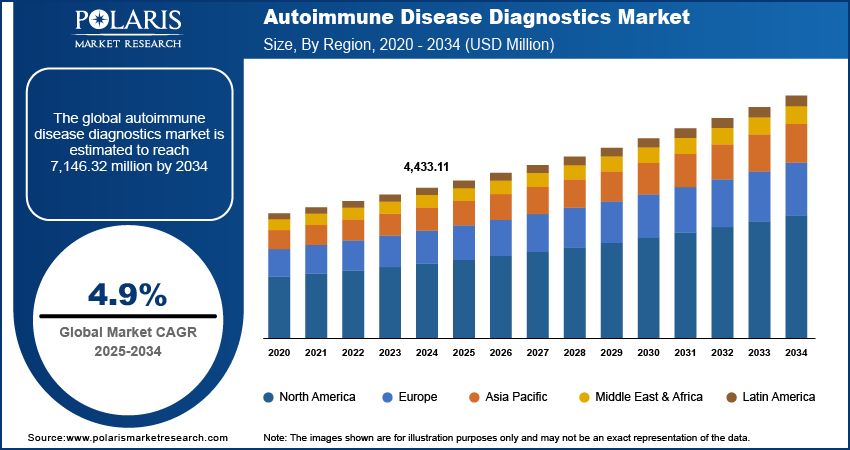

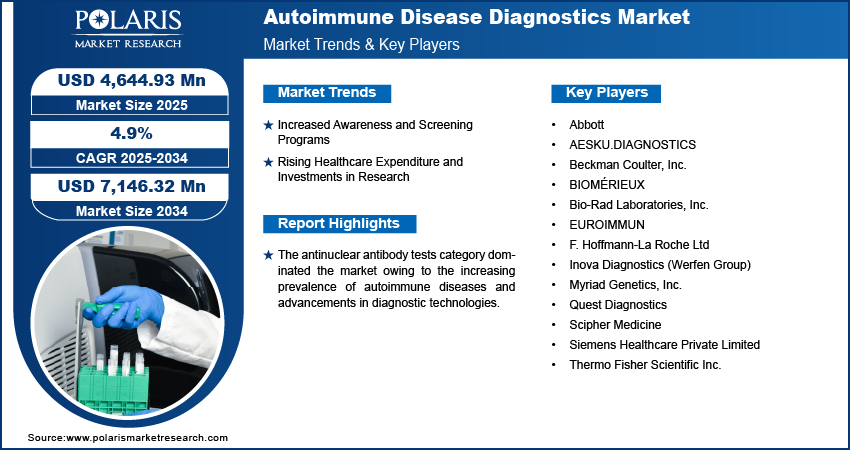

The global autoimmune disease diagnostics market size was valued at USD 4,433.11 million in 2024. The market is projected to grow from USD 4,644.93 million in 2025 to USD 7,146.32 million by 2034, exhibiting a CAGR of 4.9% during 2025–2034.

The autoimmune disease diagnostics market includes a range of diagnostic tests and tools used to identify and monitor autoimmune diseases. These include blood tests, imaging techniques, and biopsy procedures that detect specific autoantibodies, biomarkers, and inflammatory markers indicative of autoimmune activity.

The rise in the prevalence of autoimmune diseases is a significant driver of the autoimmune disease diagnostics market demand. Conditions such as rheumatoid arthritis, lupus, and multiple sclerosis are becoming more common, leading to a higher demand for diagnostic tests. This increase is due to better awareness and understanding of these diseases among both patients and healthcare providers. Additionally, environmental factors, such as pollution and dietary changes, as well as genetic predispositions, play significant roles in the rising incidence of these diseases. The growing number of diagnosed cases necessitates early and precise diagnostic methods to manage and treat these chronic conditions effectively, thereby driving the autoimmune disease diagnostics market expansion.

To Understand More About this Research: Request a Free Sample Report

In March 2024, according to the National Health Council, ∼50 million Americans suffer from autoimmune diseases; among them, 75% are women, highlighting the substantial and growing need for effective diagnostic solutions.

Technological advancements in diagnostics have significantly improved the accuracy, efficiency, and accessibility of tests for autoimmune diseases. Innovations such as multiplex assays, advanced imaging techniques, and next-generation sequencing (NGS) have enhanced the ability to detect autoimmune markers early and accurately, facilitating timely intervention and management. For instance, in September 2023, NeoDx Biotech Labs launched a REAL-TIME PCR Technology-driven in vitro diagnostic (IVD) kit designed for autoimmune disorders, enabling healthcare services to enhance their testing capabilities.

Autoimmune Disease Diagnostics Market Trends

Increased Awareness and Screening Programs

There is a growing awareness of autoimmune diseases among people and healthcare professionals, leading to increased screening and early detection efforts. Public health campaigns and educational programs are encouraging individuals to seek medical advice for symptoms that may indicate an autoimmune condition. This positive approach is driving the demand for diagnostic tests. The National Institutes of Health (NIH) has launched several initiatives aimed at raising awareness about autoimmune diseases, resulting in more individuals undergoing routine screenings and early diagnostic testing.

In March 2024, according to the National Heath Council, Autoimmune Awareness Month aims to increase awareness and understanding of autoimmune diseases. Recognizing autoimmune diseases as a serious health concern is more important than ever, given the rising incidence rates. This heightened awareness encourages more routine screenings and early diagnostic testing, boosting the demand for advanced diagnostic tools and technologies in the market.

Rising Healthcare Expenditure and Investments in Research

Increased investments in healthcare infrastructure and services are providing essential resources for the advancement of diagnostic technologies. The US government’s substantial funding for the National Institutes of Health (NIH) supports the development of advanced diagnostic tools and research on autoimmune diseases. This financial support enables the creation of sophisticated diagnostic systems and increases the range of available testing options, facilitating earlier and more accurate disease detection.

In July 2023, the National Organization for Rare Disorders (NORD) and its member organization, the APS Type 1 Foundation, funded a USD 50,000 grant for research into a rare autoimmune disorder. Such grants show how targeted funding fosters advancements in research and facilitates the development of new diagnostic tools and therapies, thereby driving progress in the field of the autoimmune disease diagnostics market.

Substantial investments in research and development by government and private sectors are driving advancements in autoimmune disease diagnostics. Collaborative efforts among various stakeholders, including public health agencies, research institutions, and industry leaders, are accelerating the development of novel biomarkers and improved diagnostic methods.

In June 2021, Progentec announced an 18-month collaborative research agreement with GlaxoSmithKline (GSK). This partnership aims to evaluate novel measurement and management tools for systemic lupus erythematosus (SLE), the most complex autoimmune disease. These collaborative initiatives are involved in advancing the field and ensuring that new diagnostic solutions are effectively brought to market. Therefore, the rising healthcare expenditure significantly contributes to the autoimmune disease diagnostics market development.

Autoimmune Disease Diagnostics Market Segment Insights

Autoimmune Disease Diagnostics Market Outlook – by Type Insights

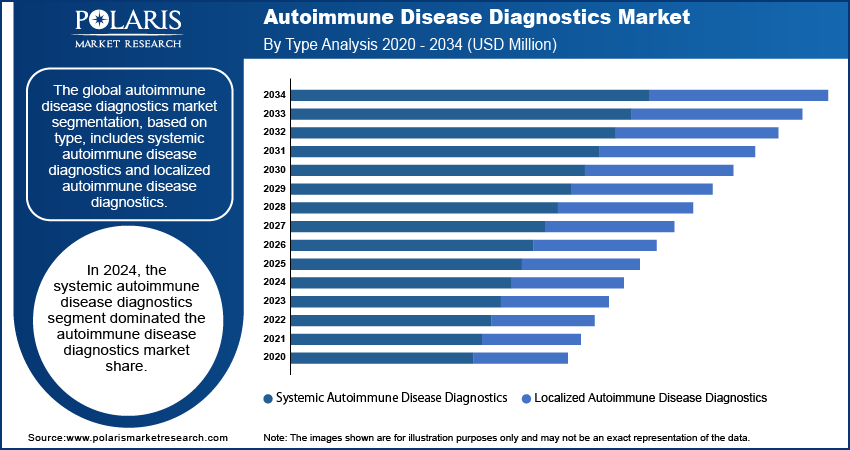

The global autoimmune disease diagnostics market segmentation, based on type, includes systemic autoimmune disease diagnostics and localized autoimmune disease diagnostics. In 2024, the systemic autoimmune disease diagnostics segment dominated the autoimmune disease diagnostics market share. Systemic autoimmune diseases, require comprehensive testing to detect a range of biomarkers and autoantibodies, driving significant demand for diagnostic tools and technologies in this segment.

The growing prevalence of systemic autoimmune diseases and increased awareness among healthcare providers and patients contribute to higher diagnostic activity in this segment. The growing adoption of high-throughput screening methods by laboratories to detect a range of autoantibodies associated with systemic autoimmune diseases.

In May 2024, the collaboration between Mayo Clinic Laboratories, a leading global reference laboratory, and Progentec Diagnostics, a company specializing in digital health and biomarker technologies, launched advanced biomarker testing services for autoimmune conditions. These innovative tests improve early and accurate diagnosis, enhancing disease management and treatment outcomes, which supports the growing demand for precise diagnostic tools in this segment.

Autoimmune Disease Diagnostics Market Assessment – by Test Type Insights

The global autoimmune disease diagnostics market segmentation, based on test type, includes antinuclear antibody tests, autoantibody tests, complete blood count, comprehensive metabolic panel, c-reactive protein, and others. The antinuclear antibody tests category dominated the market owing to the increasing prevalence of autoimmune diseases and advancements in diagnostic technologies. The market for ANA tests is expanding rapidly as they offer crucial insights for early diagnosis and management of these complex conditions.

The global autoimmune disease diagnostics market growth for the antinuclear antibody tests segment is driven by a rising awareness of autoimmune diseases, improvements in test accuracy, and a broader adoption of ANA testing in clinical settings. Additionally, the expansion of diagnostic laboratories and increasing healthcare investments in autoimmune disease diagnostics further contribute to the segment's growth. Antinuclear antibody (ANA) tests are used to detect the presence of antinuclear antibodies in the blood. Myasthenia gravis is a genetically predisposed autoimmune disease. The development of myasthenia gravis can also have an impact on this market.

In August 2022, according to NCBI, Myasthenia gravis (MG) is prevalent in the US, with 20 cases per 100,000 population. It shows a female predominance in individuals under 40 and a male predominance in those over 50. While childhood MG is rare in Western populations, it is prevalent in Asian countries, affecting around 50% of patients under 15 years old. The rising incidence of autoimmune diseases is driving the demand for Antinuclear Antibody (ANA) tests, contributing to the growth of the market.

Autoimmune Disease Diagnostics Market Regional Insights

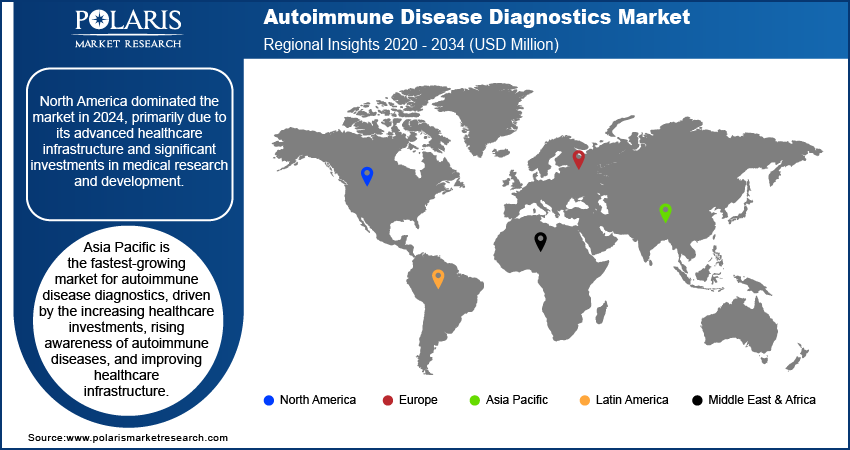

By region, the study provides the autoimmune disease diagnostics market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the market in 2024, primarily due to its advanced healthcare infrastructure and significant investments in medical research and development. The US, in particular, leads the market with its well-established healthcare system; high rates of autoimmune conditions such as rheumatoid arthritis, lupus, and multiple sclerosis; and a strong focus on precision medicine. The high prevalence of autoimmune diseases drives the autoimmune disease diagnostics market expansion in North America.

In March 2024, according to the National Health Council, about 50 million Americans have autoimmune diseases. Case of autoimmune conditions are increasing rapidly, with studies showing a 3-12% rise each year. Additionally, Type 1 diabetes cases have nearly doubled in adults over the past 40 years, and celiac disease cases have increased five-fold in the last 30 years, doubling every 15 years.

The presence of major diagnostic companies such as Quest Diagnostics, Thermo Fisher Scientific, and Abbott strengthens the region's dominance. Additionally, the substantial funding from public and private sectors for research and development contributes to continuous advancements in diagnostic technologies, reinforcing North America's leading position.

Asia Pacific is the fastest-growing market for autoimmune disease diagnostics, driven by the increasing healthcare investments, rising awareness of autoimmune diseases, and improving healthcare infrastructure. Countries such as China, India, and Japan are experiencing rapid growth in their healthcare sectors, leading to enhanced diagnostic capabilities and greater access to advanced testing technologies. The increasing prevalence of autoimmune diseases in these rapidly developing economies, coupled with a growing focus on improving healthcare standards, is contributing to the region's rapid market expansion.

The prevalence of Autoimmune Hepatitis (AIH) is increasing, with reported rates of 19.44, 22.80, and 12.99 per 100,000 people in different parts of Asia. A meta-analysis of AIH studies has shown consistent annual incidence rates, ranging from 1.00 to 1.37 per 100,000 people. This rise in incidence has led to greater awareness of the disease and improvements in diagnostic capabilities. These developments have contributed to the growth of the autoimmune disease diagnostics market.

The rising middle-class population with higher healthcare spending capacity and government initiatives to improve healthcare access further fuel the market's growth. The Asia Pacific region's fast-paced development in healthcare and rising demand for advanced diagnostic solutions position it as the most dynamic and rapidly expanding market in the autoimmune disease diagnostics sector.

Autoimmune Disease Diagnostics Market – Key Players and Competitive Insights

The autoimmune disease diagnostics market features a broad array of participants, including major diagnostic corporations, specialized biotechnology firms, and emerging startups. Major players in the market offer a wide range of advanced diagnostic technologies and extensive product portfolios, focusing on innovation to enhance early and accurate detection of autoimmune diseases. These companies invest significantly in research and development to maintain their market position. Specialized firms target niche areas within autoimmune diagnostics, such as novel biomarkers or personalized testing solutions, contributing to a diverse market offering. Emerging startups are introducing innovative technologies and approaches, often leveraging advancements in digital health and precision medicine.

The autoimmune disease diagnostics market is characterized by a dynamic environment driven by strategic collaborations, partnerships, and acquisitions, which help expand capabilities and reach. This continuous innovation and improvement in diagnostic technologies enhance the accuracy and efficiency of autoimmune disease testing. A few major players in the market are Abbott; AESKU.DIAGNOSTICS; Beckman Coulter, Inc.; BIOMÉRIEUX; Bio-Rad Laboratories, Inc.; EUROIMMUN; F. Hoffmann-La Roche Ltd; Inova Diagnostics (Werfen Group); Myriad Genetics, Inc.; Quest Diagnostics; Scipher Medicine; Siemens Healthcare Private Limited; and Thermo Fisher Scientific Inc.

Bio-Rad Laboratories, Inc. is a US-based company that develops and manufactures products for the life science research and clinical diagnostics markets. Bio-Rad was founded in 1952 in Berkeley. Their products are used in a variety of applications, including bioprocess analytics, cell research, gene expression analysis, immunology, and mutation detection. Bio-Rad's products are used by customers such as university and research institutions, hospitals, public health and commercial laboratories, biotechnology and pharmaceutical companies, and applied laboratories. The company is renowned for its expertise and innovation in autoantibody testing, which began with the introduction of the Kallestad IFA. The company provides comprehensive autoantibody testing solutions, including the BioPlex 2200 System, which enables laboratories to achieve greater results with reduced effort.

F. Hoffmann-La Roche Ltd, also known as Roche, is a Swiss multinational healthcare company that specializes in drugs and diagnostics. Roche's products and services are used by hospitals, healthcare professionals, researchers, pharmacists, and commercial laboratories. The company's research focuses on developing new treatments, medicines, and diagnostics to prevent, diagnose, and treat diseases. Roche operates worldwide under two divisions—pharmaceuticals and diagnostics. The company's portfolio includes a range of advanced immunoassays and molecular diagnostic tests designed to identify and manage autoimmune conditions with precision. Roche’s diagnostic platforms are renowned for their accuracy and reliability, providing critical insights that aid in the early detection and effective management of autoimmune diseases. There innovation and research for developing new diagnostic tools enhance patient outcomes and support personalized medicine approaches in autoimmune disease management.

List of Key Companies in Autoimmune Disease Diagnostics Market

- Abbott

- AESKU.DIAGNOSTICS

- Beckman Coulter, Inc.

- BIOMÉRIEUX

- Bio-Rad Laboratories, Inc.

- EUROIMMUN

- F. Hoffmann-La Roche Ltd

- Inova Diagnostics (Werfen Group)

- Myriad Genetics, Inc.

- Quest Diagnostics

- Scipher Medicine

- Siemens Healthcare Private Limited

- Thermo Fisher Scientific Inc.

Autoimmune Disease Diagnostics Industry Developments

January 2023: ScipherMedicine acquired Philadelphia-based CrossBridge to enhance its data and analytics capabilities. CrossBridge’s SaaS platform improves value-based care by bridging gaps among patients, providers, and payers; optimizing outcomes; and reducing costs for autoimmune disease patients.

May 2022: The Phadia 2500+ series instruments were made available for autoimmune testing in the US Supplied by Thermo Fisher Scientific, a global player in scientific solutions. This family of high-capacity, user-friendly lab instruments provides exceptional throughput for both allergy autoimmune testing and diagnostics.

November 2023: Quest Diagnostics, a global company offering diagnostic information services, and ScipherMedicine, a precision immunology company, announced a collaboration aimed at enhancing patient access to diagnostic services and advancing precision medicine for rheumatoid arthritis (RA), an autoimmune disorder.

Autoimmune Disease Diagnostics Market Segmentation

By Product Outlook

- Consumables and Assay Kits

- Instruments

By Type Outlook

- Systemic Autoimmune Disease Diagnostics

- Rheumatoid Arthritis

- Ankylosing Spondylitis

- Systemic Lupus Erythematosus (SLE)

- Others

- Localized Autoimmune Disease Diagnostics

- Multiple Sclerosis

- Type 1 Diabetes

- Hashimoto's Thyroiditis

- Idiopathic Thrombocytopenic Purpura

- Others

By Test Ty pe Outlook

- Antinuclear Antibody (ANA) Tests

- Autoantibody Tests

- Complete Blood Count (CBC)

- Comprehensive Metabolic Panel

- C-Reactive Protein (CRP)

- Others

By End User Outlook

- Hospitals

- Diagnostics Centers

- Research Laboratories

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Autoimmune Disease Diagnostics Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 4,433.11 million |

|

Market Size Value in 2025 |

USD 4,644.93 million |

|

Revenue Forecast by 2034 |

USD 7,146.32 million |

|

CAGR |

4.9% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global autoimmune disease diagnostics market size was valued at USD 4,433.11 million in 2024 and is projected to be valued at USD 7,146.32 million by 2034.

The global market is projected to register a CAGR of 4.9% during 2025–2034.

North America held the largest share of the global market in 2024 due to its advanced healthcare infrastructure and significant investments in medical research and development.

A few key players in the market are Abbott; AESKU.DIAGNOSTICS; Beckman Coulter, Inc.; BIOMÉRIEUX; Bio-Rad Laboratories, Inc.; EUROIMMUN; F. Hoffmann-La Roche Ltd; Inova Diagnostics (Werfen Group); Myriad Genetics, Inc.; Quest Diagnostics; Scipher Medicine; Siemens Healthcare Private Limited; and Thermo Fisher Scientific Inc.

The systemic autoimmune diseases segment dominated the market in 2024 due to the growing prevalence of systemic autoimmune diseases and increased awareness among healthcare providers

The antinuclear antibody (ANA) tests segment held the largest share of the global market in 2024 due to advancements in diagnostic technologies.

© 2025 Polaris Market Research and Consulting. All rights reserved