Generative AI Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Generative AI Market Summary

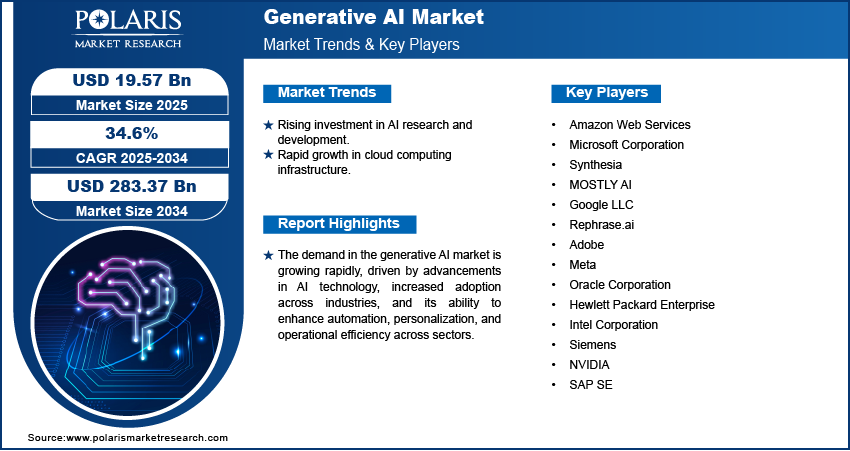

The global generative AI market size was USD 19.74 billion in 2025 and is expected to grow at a CAGR of 34.6% over the forecast period. The market is driven by higher expenditures on AI research, growing cloud infrastructure, increased adoption in the healthcare and financial sectors, and the utilization of AI in processes such as data processing and medical imaging.

Market Statistics

Key Takeaways

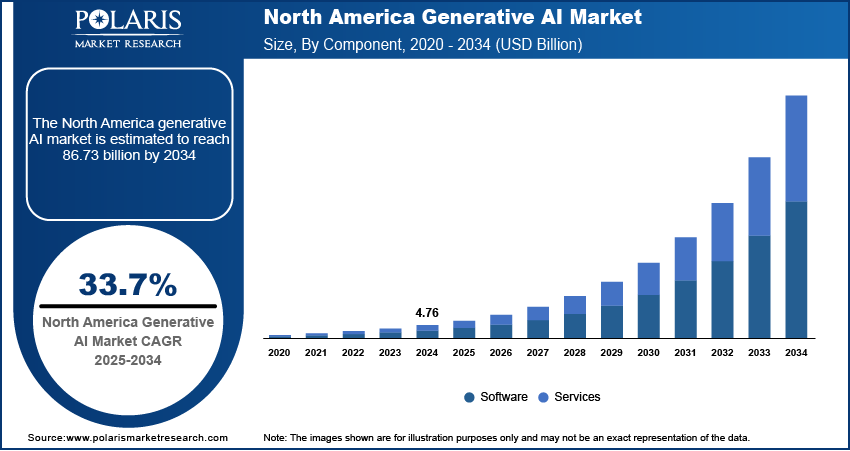

- North America led the market with 40.8% to 48.70% in 2025 due to strong investment, a solid tech ecosystem, and top research institutions.

- Asia Pacific is experiencing the fastest growth rate of CAGR 41.7% in the generative AI market, driven by substantial investments in AI research and infrastructure in countries such as China, Japan, India, and South Korea.

- The U.S. led the regional market with a 40.8% CAGR in 2025. Rapid enterprise adoption across industries and strong cloud infrastructure fueled the dominance.

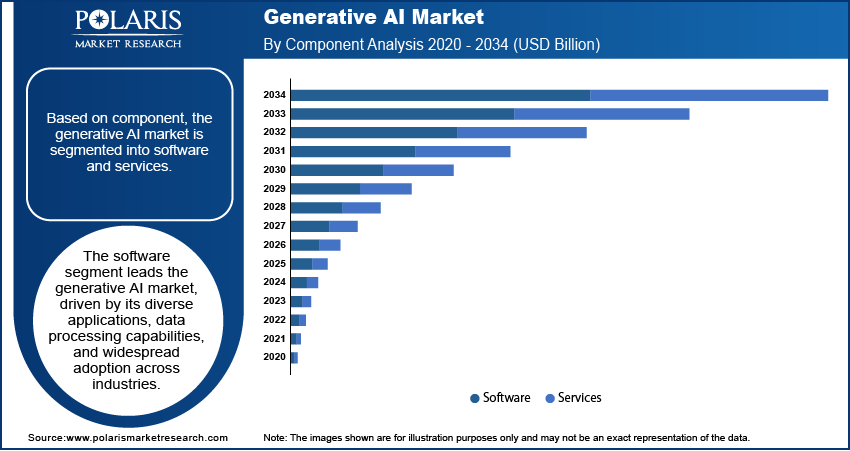

- In 2025, the software segment accounted for approximately 59% of the market share in generative AI due to its widespread adoption and ability to efficiently handle enormous volumes of data.

- The diffusion networks segment is expected to grow at the fastest rate, with a 39.1% CAGR, driven by the increasing demand for image generation and synthesis across numerous industries.

Industry Dynamics

- One of the key drivers of the market is its increasing use in applications such as spam filtering, data processing, image compression, and noise reduction in visual data.

- Growing global investments in AI development and innovation, such as the EU's significant investment in generative AI, are driving innovation and expanding its use, leading to substantial market growth for generative AI.

- Cloud infrastructure provides the processing and storage capacity necessary for creating and deploying generative AI, driving its increasing adoption across industries such as healthcare, finance, and entertainment.

- Advanced AI model development and upkeep are expensive, restricting access for small organizations.

AI Impact on Generative AI Market

- AI advancements are improving generative models, making them more accurate and versatile.

- Generative AI is leveraging AI's ability to handle large datasets and identify intricate patterns, thereby enhancing content creation.

- The incorporation of AI-based tools is rendering generative AI more accessible to other industries, increasing creativity and operational effectiveness.

- AI is helping automate tasks such as data preparation and image creation, driving its adoption in industries such as healthcare, entertainment, and finance.

Source: Polaris Market Research Analysis

What is Generative AI?

Generative AI refers to a subset of artificial intelligence that focuses on creating new data, such as text, images, audio, or video, by learning patterns and structures from existing datasets. This technology leverages advanced models such as Generative Adversarial Networks (GANs) and transformers to generate content, making it an essential tool for various applications. The global demand for generative AI is experiencing exponential growth, driven by its diverse use cases and transformative potential across industries.

What are Generative AI Output Types?

Generative AI outputs vary across text, image, video, and code generation. They vary in terms of functionality and business impact. Their differences also extend to cost structure, technical complexity, processing speed, and overall market adoption. The table below consolidates all key aspects into a single comparative view for clearer analysis. The following comparison matrix highlights how each type performs across key evaluation parameters used in AI market analysis.

Comprehensive Comparison of Generative AI Output Types

| Output Type | Description | Common Applications | Cost | Complexity | Speed | Adoption Level |

| Text Generation | Produces human-like written content such as articles, summaries, emails, and conversational responses | Content creation, chatbots, customer support, translation, and documentation | Low | Low | Very High | Very High |

| Image Generation | Creates visual content such as illustrations, realistic images, and design concepts from text prompts | Advertising, digital art, product design, gaming assets,and branding | Medium | Medium | High | High |

| Video Generation | Generates or edits video content combining visuals, motion, and audio using AI models | Marketing videos, film production, training modules, social media content, and animation | High | High | Medium to Low | Medium |

| Code Generation | Produces programming code from natural language instructions or assists in debugging and optimization | Software development, automation scripts, app prototyping, DevOps, and API integration | Medium | Medium to High | High | High |

Source: Polaris Market Research Analysis

How is AI Creating Human-Like Content?

AI creates human-like content by learning patterns from large datasets of text, images, audio, and code generated by humans. It uses deep learning models such as transformer architectures. It predicts the most contextually relevant next words, pixels, or frames. This enables it to generate responses that mimic human tone, structure, and reasoning. Therefore, the output often appears natural, coherent, and context-aware like human-created content.

One of the key factors propelling the generative AI market revenue is its increasing utilization in tasks such as spam detection, data preprocessing, image compression, and noise reduction in visual data. Additionally, its growing adoption in medical imaging equipment and image classification has further solidified its significance in critical domains such as healthcare. Generative AI’s ability to enhance operational efficiency and foster innovation has made it indispensable for businesses seeking AI-driven solutions. For instance, in March 2023, Microsoft Corporation introduced Visual ChatGPT, an innovative model integrating multiple visual foundation models. This breakthrough allows users to interact with ChatGPT via graphical user interfaces, expanding the scope of AI-powered tools in creative and professional workflows.

Market Dynamics

Rising Investment in AI Research and Development

Governments and organizations worldwide are allocating substantial funds to accelerate advancements in artificial intelligence, recognizing its transformative potential across industries. For instance, the EU has heavily invested in AI through initiatives such as Horizon Europe and the Digital Europe Programme, committing EUR 2.6 billion for 2021-2022 and an additional EUR 4 billion for generative AI development by 2027 through the AI Innovation Package. These investments are enhancing the capabilities of generative AI and also broadening its applications in areas such as data preprocessing, image compression, and medical imaging. As a result, rising investments in AI research and development are significantly driving generative AI market growth.

Rapid Growth in Cloud Computing Infrastructure

Cloud platforms provide the scalable computing power and storage necessary to train and deploy advanced generative AI models, enabling organizations to harness AI-driven solutions more effectively. The demand for generative AI continues to rise across various sectors, including healthcare, finance, and entertainment, as businesses increasingly adopt cloud-based services.

For instance, in October 2024, Oracle invested over $6.5 billion to establish a public cloud region in Malaysia, emphasizing the critical role of cloud infrastructure in enhancing AI innovation and digital transformation. This expansion of Oracle Cloud Infrastructure (OCI) in Asia Pacific highlights advancements in cloud computing are empowering organizations to deploy generative AI applications more efficiently, thereby driving generative AI market demand. The synergy between cloud computing and AI is expected to continue fueling the adoption and evolution of generative AI technologies globally.

Source: Polaris Market Research Analysis

Segment Analysis

Market Assessment by Component Outlook

The global generative AI market segmentation, based on component, includes software and services. The software segment accounted for ∼ 59% of the generative AI market share in 2025 due to its diverse applications and ability to quickly process vast amounts of data. AI software is particularly valued for its capacity to synthesize data from various hardware systems and generate intelligent responses, making it essential across industries. It is increasingly used in applications such as smartphone assistants, ATMs, ad-serving software, and voice and image recognition, all of which are driving the demand for advanced AI solutions. The ability of AI software to improve operational efficiency, automate tasks, and deliver personalized experiences further propels its growth. This rapid surge in research and development of AI software such as NLP, ML & DL,etc, along with the integration of AI into everyday technology, solidifies the software segment's dominance in the market.

Market Evaluation by Technology Outlook

The global generative AI market segmentation, based on technology, includes generative adversarial networks, transformers, variational auto-encoders, and diffusion networks. The diffusion networks segment is expected to register the highest CAGR of 39.1% during the forecast period due to the growing demand for image synthesis and generation across various industries. Diffusion networks, which employ advanced generative models to create high-quality images, are increasingly utilized in sectors such as healthcare, BFSI, automotive, transportation, defense, media & entertainment, and IT & telecommunication. These networks offer significant value by enhancing operational efficiency, enabling faster decision-making, and providing better customer experiences. For instance, in healthcare, diffusion networks generate medical images for analysis, improving diagnostic accuracy. The demand for diffusion networks is expected to surge as businesses and governments continue to recognize the benefits of this technology, making it one of the fastest-growing segments in the market.

Source: Polaris Market Research Analysis

Regional Analysis

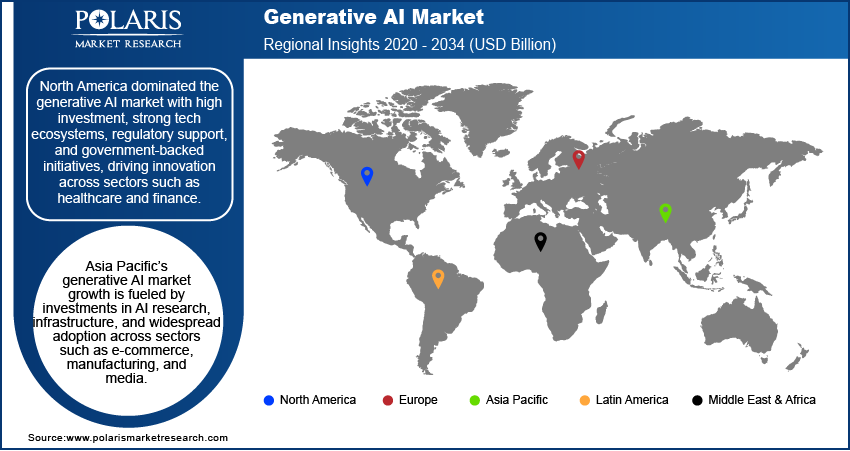

By region, the study provides generative AI market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the market due to its high investment levels, a robust ecosystem of technology companies, and leading research institutions. The region’s rapid adoption of generative AI across sectors such as healthcare, finance, and entertainment reflect its growing recognition of AI’s potential to enhance productivity and foster innovation. North America’s commitment to developing AI technologies is supported by substantial funding and a thriving startup culture, particularly in the US. For instance, in 2022, the US government allocated $4.8 billion to AI research, focusing on smart health, data science, astronomical sciences, and materials research through NSF-led initiatives. Additionally, regulatory frameworks on data privacy and AI ethics are helping shape responsible AI adoption, further encouraging its growth. In Canada, government-backed initiatives are promoting AI research and innovation, creating an environment conducive to generative AI development. This combination of investment, talent, and regulatory support positions North America as a global leader in generative AI technology.

Asia Pacific is experiencing the fastest growth in the generative AI market, driven by substantial investments in AI research and infrastructure across major economies such as China, Japan, India, and South Korea. These countries are advancing in sectors such as autonomous systems, robotics, and digital transformation. The widespread adoption of generative AI in e-commerce, manufacturing, and media is further propelling growth as businesses seek automation and personalization. For instance, AWS's $8.3 billion investment in cloud infrastructure in Maharashtra by 2030 will boost India’s GDP by $15.3 billion, reinforcing the region's rapidly expanding AI capabilities.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis Report

The competitive landscape of the generative AI market is characterized by a mix of global leaders and regional players competing for market share through innovation, strategic partnerships, and regional expansion. Key players such as Amazon Web Services, Microsoft Corporation, and others in the market leverage their robust research and development capabilities along with extensive distribution networks to offer advanced generative AI solutions tailored for various applications. These major companies focus on continuous product innovation to improve efficiency, reliability, and scalability to meet the evolving needs of industries that require advanced power management solutions. At the same time, smaller regional firms are entering the market with specialized generative AI solutions targeting local market demands, often focusing on customized and cost-effective applications. A few competitive strategies in the generative AI industry include mergers and acquisitions, collaborations with technology firms, and expanding product portfolios to enhance market presence and cater to the growing demand for advanced grid solutions. Amazon Web Services, Microsoft Corporation, Synthesia, MOSTLY AI, Google LLC, Rephrase.ai, Adobe, Meta, Oracle Corporation, Hewlett Packard Enterprise, Intel Corporation, Siemens, NVIDIA, and SAP SE are among the key major players.

Adobe offers digital media and marketing solutions, including creative tools such as Photoshop and Premiere Pro, integrating generative AI for enhanced workflows and providing security solutions across sectors. In June 2023, Adobe partnered with Omnicom Group, leveraging joint generative AI capabilities to empower shared clients to craft on-brand content for improved marketing outcomes

Hewlett Packard Enterprise provides intelligent solutions across six segments, including HPC & AI, storage, intelligent edge, and financial services. It helps clients capture, analyze, and act on data from edge to cloud. In June 2023, Hewlett Packard Enterprise launched HPE GreenLake for Large Language Models, an AI cloud service enabling enterprises to privately train and deploy large-scale AI models using HPE's supercomputing platform and partnering with Aleph Alpha for field-proven LLM capabilities.

List of Key Companies

- Amazon Web Services

- Microsoft Corporation

- Synthesia

- MOSTLY AI

- Google LLC

- Rephrase.ai

- Adobe

- Meta

- Oracle Corporation

- Hewlett Packard Enterprise

- Intel Corporation

- Siemens

- NVIDIA

- SAP SE

Generative AI Industry Developments

April 2026: Avid and Google Cloud formed a multi-year partnership to integrate agentic and generative AI into Avid’s media production tools. The companies will embed Google’s Gemini models and Vertex AI into platforms like Media Composer and Content Core. The collaboration aims to automate and enhance video editing workflows. (Source: avid.com)

In April 2025: OpenAI launched two new reasoning models: o3, its most advanced model for coding, math, science, and visual analysis with significantly fewer errors, and o4-mini, a faster, smaller, and more affordable model optimized for math, coding, and visual tasks. (Source: openai.com)

Generative AI Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Software

- Services

By Technology Outlook (Revenue, USD Billion, 2021–2034)

- Generative Adversarial Networks

- Transformers

- Variational Auto-encoders

- Diffusion Networks

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Media & Entertainment

- BFSI

- IT & Telecommunication

- Healthcare

- Automotive & Transportation

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Generative AI Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 19.74 billion |

| Market Size Value in 2026 | USD 26.45 billion |

| Revenue Forecast by 2034 | USD 283.37 billion |

| CAGR | 34.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Generative AI Market FAQ's

• The global generative AI market size was valued at USD 19.74 billion in 2025 and is projected to grow to USD 283.37 billion by 2034.

• The global market is projected to register a CAGR of 34.6% during the forecast period.

• North America dominated the generative AI market in 2025

• A few key players in the market are Amazon Web Services, Microsoft Corporation, Synthesia, MOSTLY AI, Google LLC, Rephrase.ai, Adobe, Meta, Oracle Corporation, Hewlett Packard Enterprise, Intel Corporation, Siemens, NVIDIA, and SAP SE.

• The software segment led the market share in 2025.

• The diffusion networks segment of the generative AI market is anticipated to register the highest growth rate during the forecast period.

Healthcare, finance, media and entertainment, and retail are among the largest adopters of generative AI. The technology is widely used for medical imaging, fraud detection, content creation, and personalized customer experiences, driving rapid adoption across these high-growth sectors.

Download Sample Report of Generative AI Market

Please fill out the form to request a customized copy of the research report.