Forensic Imaging Market Share, Size, Trends, Industry Analysis Report, By Modality (X-ray, CT, MRI, Ultrasound); By Application (Death Investigations, Clinical Studies); By End-Use (Forensic Institutes, Hospitals, Others); By Regions; Segment Forecast, 2021 - 2028

- Published Date:Jan-2021

- Pages: 108

- Format: PDF

- Report ID: PM1793

- Base Year: 2020

- Historical Data: 2016 - 2019

Report Outlook

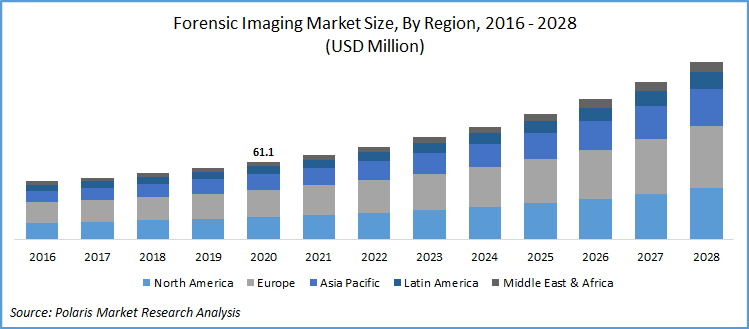

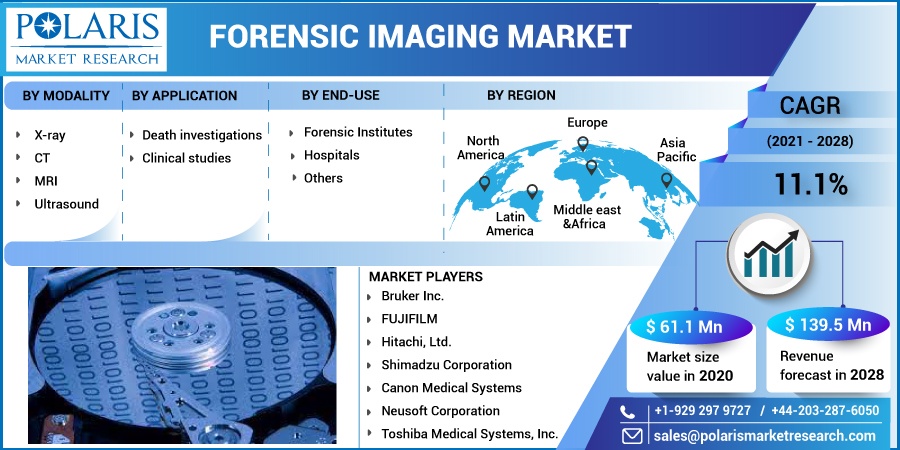

The global forensic imaging market was valued at USD 61.1 million in 2020 and is expected to grow at a CAGR of 11.1% during the forecast period. The prominent factors for the market growth include growing preference towards virtual autopsy, awareness among patients about the benefits of virtual autopsy as compared to traditional body opening autopsies, and the innovations in cross-sectional imaging procedures.

Innovations in medical imaging for the forensic areas have facilitated minimally invasive postmortem investigations. Moreover, the implementation of artificial intelligence in imaging modalities in the identification of death cause in case of murder or any crime is anticipated to open new avenues for the forensic imaging market.

Know more about this report: request for sample pages

Industry Dynamics

Growth Drivers

The rising usage of virtual autopsies in the judiciary systems is expected to drive the demand for forensic imaging modalities. In previous times, the photo evidence developed from traditional autopsy procedures was very disturbing for the lawyers, limiting its acceptability in the court proceedings.

In such cases, 3D constructed images with death marking highlighting major injuries developed via advanced imaging modalities are well appreciated by the judges. Furthermore, the digitalization of visual crime evidence, enables data storing for future reference and any vulnerability regarding evidence tempering.

Know more about this report: request for sample pages

Furthermore, the surge in crime rate, advances in advanced imaging techniques, and innovations in image analysis through automated software also favored the market growth. For instance, Virtobot, an advanced robotic system comprising of all MRI, angiography, and navigation systems with simulation software provide forensic services, without anybody mutilation.

A virtual autopsy is a non-invasive procedure, which became the preferred choice among wider communities, for instance, Japanese Buddhist culture does not allow an autopsy, but is now gaining popularity amongst growing acceptability of the virtual autopsy.

Forensic Imaging Market Report Scope

The market is primarily segmented on the basis of modality, application, end-use, and region:

|

By Modality |

By Application |

By End-Use |

By Region |

|

|

|

|

Know more about this report: request for sample pages

Insight by Modality

Based upon the modality, the global market is categorized into X-ray, CT, MRI, and ultrasound. In 2020, the x-ray segment accounted for the largest share in the global market. X-ray modality is considered as the gold standard in the identification of dead bodies in forensic medicine, primarily being used for air embolism, motor crashes, and gunshots. X-rays are highly used in emerging economies, owing to their high accessibility and affordability.

CT modality is projected to register a lucrative growth rate over the study period. The significant rise in post-mortem CT examination to properly locate fractures in the complex skeletal muscles such as the face, pelvis, neck, and spine of the corpse is the prime factor responsible for such growth.

Even, the ongoing practice of CT examination before autopsy has received a wider acceptance, owing to cost-effectiveness and time-saving attributes. For instance, CT scans signify death causes, such as whether the accident victim dies due to head injury or has pelvis and abdomen fracture.

Insight by Application

Based on the application, the global market is bifurcated as death investigations and clinical studies. In 2019, the death investigations accounted for the largest share in the global market. The rise in cases of un-reported deaths such as trauma, murder, and suicide was largely responsible for such high growth. Moreover, a compulsory requirement in court to know about the death cause also has fueled the use of virtual autopsy in death investigation related queries.

The clinical studies segment is expected to register lucrative growth over the study period. Increasing voluntary body donors for clinical studies, and the recent surge in COVID-19 have largely contributed to the segment’s growth. Moreover, demand for autopsies of corpses to decipher pathophysiology of new disease and also such radiological imaging could reduce the risk of infection.

Geographic Overview

Geographically, the global forensic imaging market is bifurcated into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa (MEA). North America region is the largest revenue contributor followed by Europe and the Asia Pacific region. In 2019, the Europe region accounted for over 35% of the global market.

Factors responsible for the growth of North America include the shift of coroner to advanced medical examiner system in the U.S. and Canada and the huge shortage of pathologists in the nation. Both countries are anticipated to witness a shortage of pathologists at the autopsy centers, owing to cope up with heavy workloads. This would lead to the adoption of advanced technologies at the autopsy centers, hence, lowering the count of un-necessary autopsies.

The Asia Pacific is projected to register the highest growth rate over the study period. Rapid usage of forensic imaging in countries such as Japan, India, South Korea, South Korea, and China. Most government-run hospitals often use advanced imaging tools for autopsy.

Countries like Japan have dedicated imaging centers for automated autopsies, which facilitates teleradiology in the forensic imaging field. Moreover, the rapid surge in COVID-19 cases in the region also complemented the region’s growth. As of September 2020, Asia accounted for over 30% of the COVID-19 cases.

Competitive Insight

The prominent players operating in the market are Shimadzu Corporation, Canon Medical Systems, Neusoft Corporation, Bruker Inc., FUJIFILM, Hitachi, Ltd., and Toshiba Medical Systems, Inc.

© 2025 Polaris Market Research and Consulting. All rights reserved