Europe Non-Automotive Rubber Transmission Belts Market Share, Size, Trends, Industry Analysis Report, By Product (Raw Edged Belts, V-Belts, Timing Belts, Specialty Belts, Others); By Application; By Country; Segment Forecast, 2024 - 2032

- Published Date:May-2024

- Pages: 115

- Format: PDF

- Report ID: PM4896

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

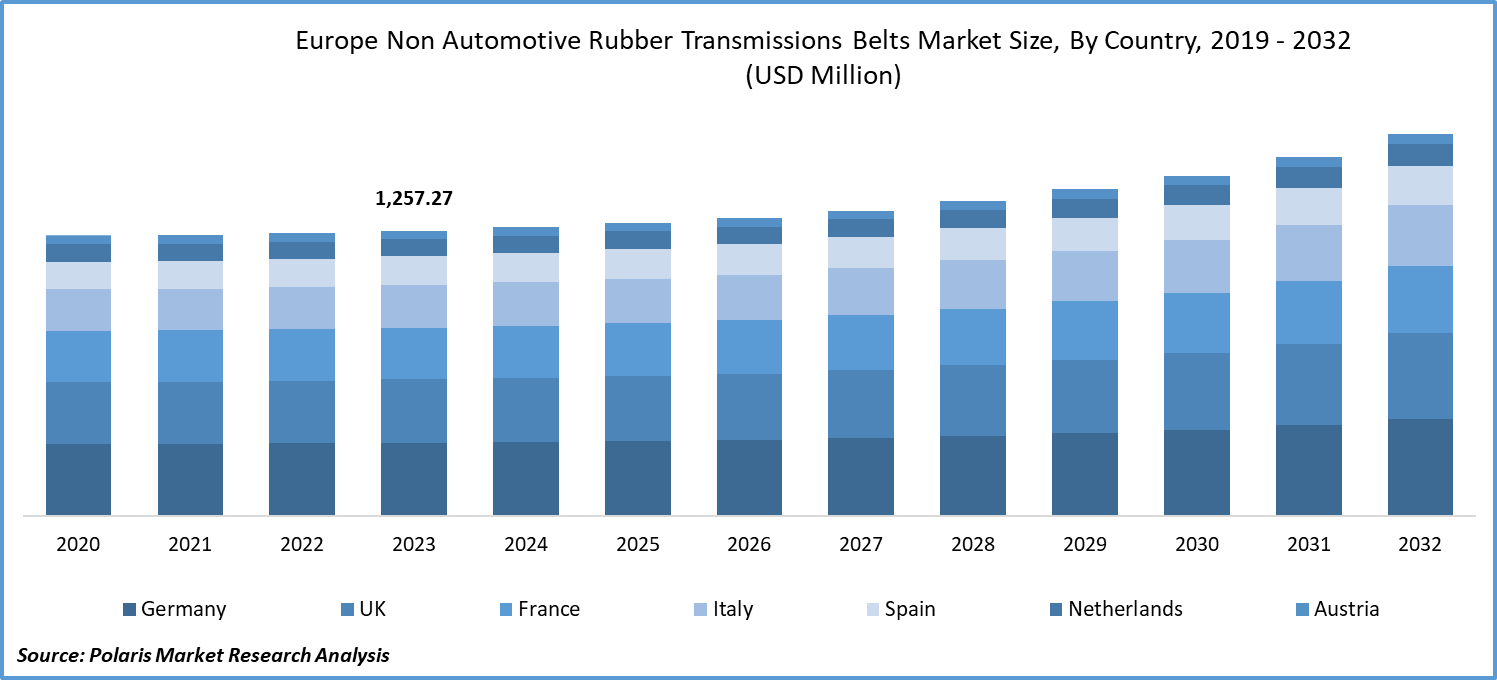

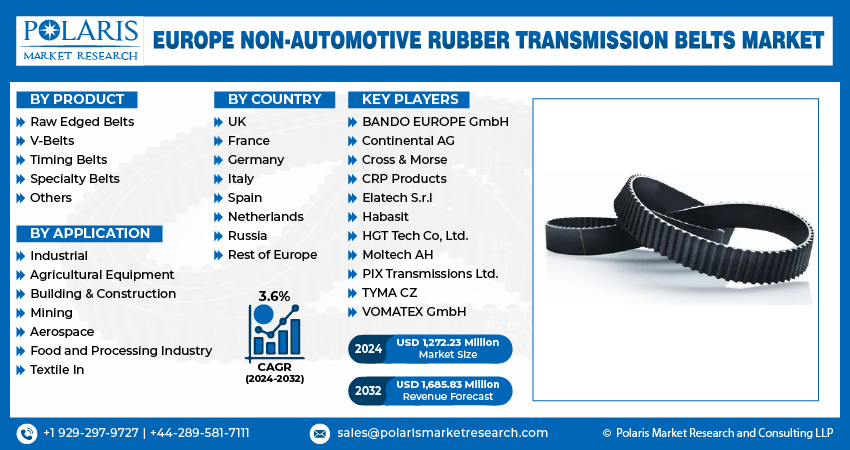

Europe non-automotive rubber transmission belts market size was valued at USD 1,257.27 million in 2023. The market is anticipated to grow from USD 1,272.23 million in 2024 to USD 1,685.83 million by 2032, exhibiting the CAGR of 3.6% during the forecast period.

Industry Trends

The Europe non-automotive rubber transmission belts market is growing due to industrialization and Europe's rising need for manufactured goods. The market is expanding due to automation trends and technological advancements such smart functions and increased energy efficiency to fulfil the need for material handling processes efficiently across a range of sectors is propelling the European market's notable expansion and development. Moreover, Europe is considered as trade hub for export for various countries having full connectivity is fueling the growth of this market.

Over the projected period, rising mining activity along with urbanization and industrialization are expected to propel the non-automotive rubber transmission belts market. The food and processing industry, building and construction sectors' rising need for non-automotive rubber transmission belts is anticipated to drive the market. The industrial sector is growing as a result of the deployment of robotic systems. European manufacturers are increasing their manufacturing capabilities in order to fulfill the growing expectations of consumers in marketplaces.

To Understand More About this Research:Request a Free Sample Report

Despite the growth prospects, the market faced challenges during COVID-19 linked to the major interruptions in supply-chain and manufacturing activities which suffered from a variety of preventive lockdowns and other limitations that were imposed by international regulatory bodies. Furthermore, because Europe’s overall economic condition was negatively impacted by this outbreak, manufacturers cut on non-essential spending, to increase consumer demand. However, the Europe’s market for non-automotive rubber transmission belts rebounded with time.

Key Takeaways

- Germany dominated the market and contributed highest market share with 3.4% in Europe non-automotive rubber transmission belts market.

- By application category, mining segment accounted for the fastest CAGR of 4.4% in the Europe non-automotive rubber transmission belts market.

- By product category, the V-belt segment is dominant and anticipated to grow with a lucrative CAGR of 4% in the Europe non-automotive rubber transmission belts market forecast period

What are the market drivers driving the demand for market?

Rising demand for non-automotive transmission belts in Europe

The market is experiencing significant growth due to the escalating demand for alternative rubber solutions for the manufacturing of rubber transmission belts. This is leading to innovation of alternatives which are sustainable than the traditional substances and contribute to reduced carbon footprint in the ecosystem. For instance, in September 2023, Continental AG has created a new synthetic rubber drive belt that it claims is based on a more sustainable material, in an effort to further enhance climate protection. The organic fibers and biopolymers used in the fabric and tension elements of the belt are derived from sustainable raw sources. In addition, the device has technical advancements over its predecessors, allowing for greater power transfer and better resilience to heat and cold.

Which factor is restraining the demand for market?

Raw material volatility affects the European market growth

The expansion of the rubber market is significantly impeded by the volatility of raw material prices. Rubber tree latex and synthetic polymers are two major natural resource inputs in the rubber production process. Variations in the cost and availability of these materials affect the cost of manufacturing and, eventually, the price of the final product. Supply chains can be disrupted and pricing instability can result from environmental concerns, geopolitical causes, and economic upheavals. Long-term planning may be disbalanced and manufacturers find it difficult to sustain stable profit margins as a result of this uncertainty. The use of effective inventory management systems and diversification of supply sources are two examples of mitigation methods that are necessary to manage price volatility and preserve market stability. For instance, during July-September 2023, The total market for EPDM rubber was adversely impacted by a significant decline in mining and industrial operations in this region. During October-December 2023, After initially struggling, the mining and industrial sectors increased their procurement rates, and in the last month of the year, EPDM rubber prices rose. During Q1 of 2024, Due to weak market fundamentals and geopolitical concerns, EPDM rubber prices decreased despite high upstream and energy costs. Due to ordinary demand from the polymer sector and slow derivative orders, purchasers held back, causing a considerable decrease in the price of EPDM rubber in Germany.

Report Segmentation

The market is primarily segmented based on product, application and country.

|

By Product |

By Application |

By Country |

|

|

|

To Understand the Scope of this Report:Speak to Analyst

Category Wise Insights

By Product Insights

Based on product analysis, the market is segmented into raw edged belts, V-belts, timing belts, specialty belts and others. The V-belts segment has dominated the market with largest market share and is anticipated to grow at the fastest CAGR over the forecast period owing to its wide applications in Europe's all fields of mechanical engineering, particularly those involving small-sized compact drives, as those used in compressors, fans, lawn mowers, machine tools, and several other applications. The belts have a unique tension element and a very robust rubber substance. Their contoured teeth provide more flexibility, and their improved flanks offer a superior friction coefficient.

Even in challenging working environments such those brought on by dirt, dust, and dampness, they function well. It's also important to remember that no lubricant is needed. Also, these v-belts are perfect for use in temperate countries like Europe withstanding the temperature without deteriorating in standard quality.

By Application Insights

Based on application analysis, the market has been segmented into industrial, agricultural equipment, building & construction, mining, aerospace, food and processing industry, textile industry, others. The industrial segment held the largest market share and the mining segment is expected to experience significant growth with fastest CAGR over the forecast period in Europe's non-automotive rubber transmission belts market. A sizable amount of the iron ore and steel produced worldwide comes from Europe. Steel-consuming sectors, including construction, smelting, mining, and heavy machine tools require frequent usage of rubber transmission belts to transfer bulk material in the industrial sector. Labor is being replaced by automated industrial equipment to boost productivity and satisfy growing customer expectations.

Due to Europe’s strong marketplaces, dense populations, and comparatively high levels of living, the European nations engage in a significant amount of commerce with one another. For example, Germany gives chemicals and coking coal to France, which then delivers iron ore from Lorraine to Belgium.

Country-wise Insights

Germany

The Germany leads the non-automative rubber transmission belts market in Europe since the country has an access to some of the most cutting-edge materials and production techniques; as a result, its products are designed to exceed those of their competitors. Germany has collaborated with the majority of the world's best auto engineers to provide non-automative rubber transmission belts of original equipment quality that can be installed in almost any automobile on the road. Since many automobile mechanics rely on EPDM belts for their silent operation, wear-resistant design, and strictest tolerances in the business, Germany is the leader in innovation.

Italy

The Italy is the fastest growing country with healthy CAGR in the non-automative rubber transmission belts market in Europe owing to the significant investments made in human resources and technology have gradually moved toward production expansion, providing clients with specialized manufacturing solutions. with improved structure and focus to assist the OEM market, striving to satisfy its needs with competitively priced, high-quality solutions.

Competitive Landscape

The competitive landscape for the European non-automotive rubber transmission belts market is characterized by intense competition among key players striving to gain market share and differentiate themselves through innovation and strategic partnerships. Amidst this landscape, collaboration between technology vendors, service providers, and industry stakeholders remains crucial for driving innovation, expanding market reach, and addressing evolving customer demands in the European non-automotive rubber transmission belts market.

Some of the major players operating in the European market include:

- BANDO EUROPE GmbH

- Continental AG

- Cross & Morse

- CRP Products

- Elatech S.r.l

- Habasit

- Hangzhou Grand Transmission Tech Co, Ltd.

- Moltech AH

- PIX Transmissions Ltd.

- TYMA CZ

- VOMATEX GmbH

Recent Developments

- For instance, in December 2023, AMMEGA Group and Sonata Software signed a strategic partnership. AMMEGA will be able to standardize and optimize business processes, increase performance transparency, collaborate more effectively with the help of Sonata's modernization solution and guaranteed results and cut down on IT landscape complexity while promoting digital innovations for company expansion.

- For instance, in April 2023, Semperit A.G. holding headquartered in Austria shifted its streamlined focus to manufacturing of other rubber industrial products with a sale of $122.1 million units to expand their existing business.

Report Coverage

The Europe non-automotive rubber transmission belts market report emphasizes on key countries across the region to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the region. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, product, application, and their futuristic growth opportunities.

Europe Non-Automotive Rubber Transmission Belts Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 1,272.23 million |

|

Revenue forecast in 2032 |

USD 1,685.83 million |

|

CAGR |

3.6% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024 – 2032 |

|

Quantitative units |

Revenue in USD million and CAGR from 2024 to 2032 |

|

Segments covered |

By Product, By Application, By Country |

|

Regional scope |

UK, France, Germany, Italy, Spain, Netherlands, Russia, Rest of Europe |

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The Europe Non-Automotive Rubber Transmission Belts market size is expected to reach USD 1,685.83 Million by 2032

Key players in the market are Continental AG, Cross & Morse, CRP Products, Habasit, Hangzhou Grand Transmission Tech Co, Ltd

The Europe Non-Automotive Rubber Transmission Belts Market report covering key segments are product, application and country.

Europe non-automotive rubber transmission belts market exhibiting the CAGR of 3.6% during the forecast period.

© 2025 Polaris Market Research and Consulting. All rights reserved