District Heating Market Size, Share, Trends, Industry Analysis Report: By Energy Source (Renewable Energy, Fossil Fuels, and Waste Heat), Application, Technology, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Feb-2025

- Pages: 129

- Format: PDF

- Report ID: PM3146

- Base Year: 2024

- Historical Data: 2020-2023

District Heating Market Overview

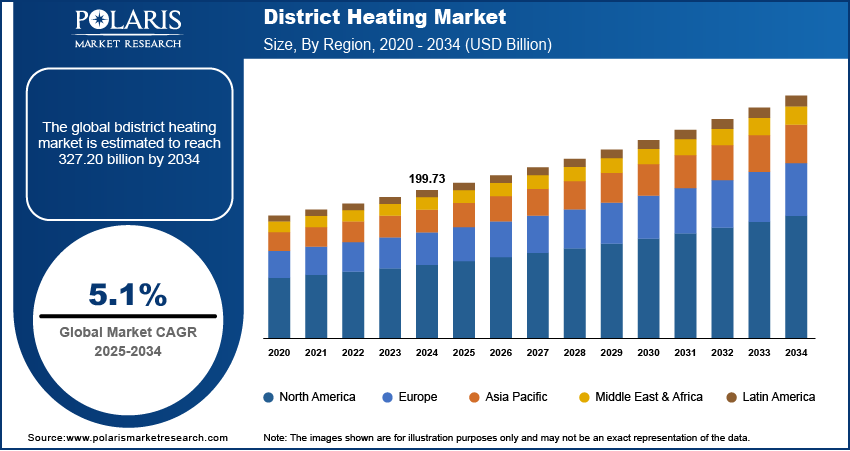

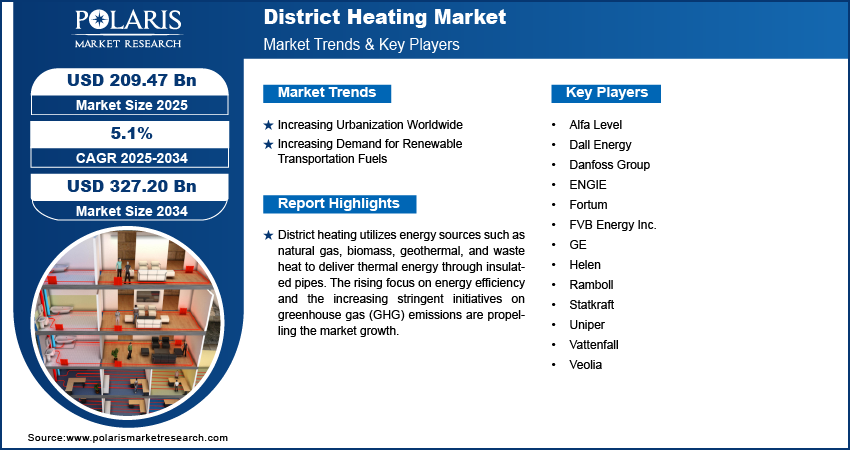

The global district heating market size was valued at USD 199.73 billion in 2024. The market is projected to grow from USD 209.47 billion in 2025 to USD 327.20 billion by 2034, exhibiting a CAGR of 5.1 % from 2025 to 2034.

District heating, also known as community heating, utilizes energy sources such as natural gas, biomass, geothermal, and waste heat to deliver thermal energy through insulated pipes. This heating solution reduces the reliance on individual heating systems. It is widely adopted in developed countries such as Denmark, Sweden, and Germany, where efficient energy use and sustainability are prioritized.

The rising stringent initiatives on greenhouse gas (GHG) emissions are propelling the district heating market growth. Governments globally are introducing stringent policies and incentives to reduce GHG emissions by promoting district heating as a low-carbon alternative for heating solutions in residential, commercial, and industrial spaces. For instance, the European Union has set ambitious targets to achieve net-zero carbon emissions by 2050, encouraging the deployment of district heating systems powered by renewable energy sources.

To Understand More About this Research: Request a Free Sample Report

The district heating market demand is driven by the growing focus on energy efficiency. District heating systems deliver thermal energy from a centralized source to multiple buildings, ensuring optimized energy use and minimizing wastage compared to individual heating systems. Governments and organizations worldwide are setting energy efficiency targets to combat climate change, which has led to increased adoption of district heating systems powered by renewable energy sources and waste heat recovery.

District Heating Market Dynamics

Increasing Urbanization Worldwide

Rapid urbanization is driving the demand for efficient and reliable heating solutions in residential and commercial spaces. For instance, a report from the United Nations states that 55% of the world's population currently lives in urban areas, a figure expected to rise to 68% by 2050. District heating provides a cost-effective way to meet heating demands in residential and commercial spaces, minimizing energy losses and carbon footprints. Countries such as China and India, with growing urban populations, are witnessing high investments in district heating infrastructure. Additionally, the scalability of district heating systems enables governments worldwide to address the heating requirements of urban centers by integrating advanced technologies such as IoT for real-time monitoring and optimization. Thus, the rising urbanization globally is driving the district heating market revenue.

Technological Advancements in Heating Systems

Innovative technologies are contributing to the district heating market expansion by improving energy efficiency and operational flexibility. Smart heating systems equipped with sensors, data analytics, and artificial intelligence enable efficient energy distribution and predictive maintenance. Additionally, advancements in pipe insulation and heat exchanger designs minimize energy loss, further enhancing system efficiency. These developments are fueling the continued adoption of district heating systems.

District Heating Market Segment Insights

District Heating Market Evaluation by Energy Source Insights

Based on energy source, the district heating market is divided into renewable energy, fossil fuels, and waste heat. The renewable energy segment is expected to grow at a rapid pace during the forecast period, owing to the stringent environmental regulations and a global commitment to reduce greenhouse gas emissions. The ongoing deployment of modern heating technologies, such as fourth-generation district heating systems that rely heavily on renewable sources, plays a crucial role in driving the segment's growth. Additionally, the prioritization of energy security and sustainability by major countries worldwide is contributing to the rapid growth of the segment.

District Heating Market Assessment by Application Insights

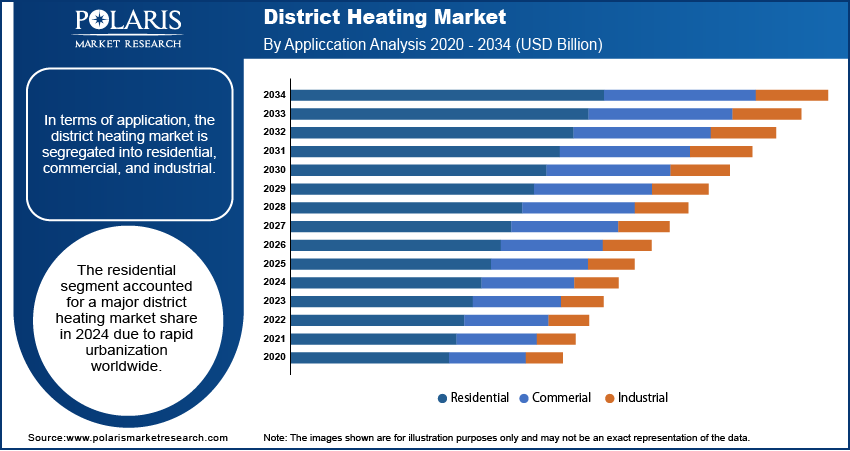

In terms of application, the district heating market is segregated into residential, commercial, and industrial. The residential segment accounted for a major district heating market share in 2024 due to rapid urbanization worldwide. Governments and municipal authorities are prioritizing providing efficient and reliable heating solutions to urban housing developments, especially in colder climates where heating needs are essential. Subsidies and funding initiatives for sustainable heating systems in countries such as China, Germany, and Sweden have further boosted the adoption of district heating systems in the residential segment. Rising awareness of energy efficiency among homeowners, along with the integration of advanced technologies such as smart meters and energy management systems, has also contributed to the segment’s dominance.

District Heating Market Regional Analysis

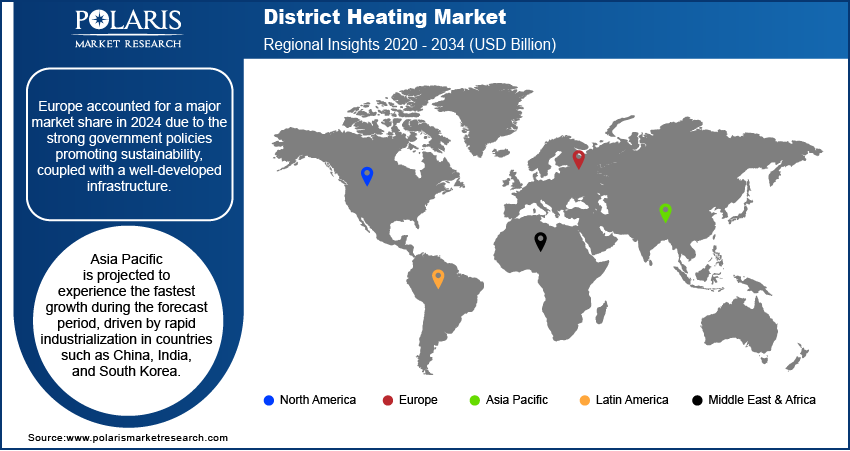

By region, the report provides the district heating market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Europe accounted for a major market share in 2024 due to the strong government policies promoting sustainability, coupled with a well-developed infrastructure. Countries such as Denmark, Germany, and Sweden have made significant investments in integrating renewable energy sources and waste heat recovery technologies into their energy systems, which has propelled the growth of the market. Sweden emerged as the dominating country in Europe due to its heavy reliance on biomass and waste heat, supported by tax incentives and subsidies that prioritize low-carbon technologies.

The Asia Pacific district heating market is projected to experience the fastest growth during the forecast period, driven by rapid industrialization in countries such as China, India, and South Korea. China is estimated to hold the largest share within the region due to its large-scale adoption of centralized heating networks aimed at improving energy efficiency and reducing urban air pollution. Furthermore, the rising urban populations and the expansion of residential and commercial infrastructure are contributing significantly to the demand for efficient heating solutions, including district heating, in the region. For instance, as per the data published by UN-Habitat, 54% of the global urban population, more than 2.2 billion people, live in Asia. By 2050, the urban population in Asia is expected to grow by 50%.

District Heating Market – Key Players and Competitive Insights

Major market players are investing heavily in research and development in order to expand their offerings, which will help the district heating market grow even more. These market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments including innovative launches, international collaborations, higher investments, and mergers and acquisitions between organizations.

The district heating market is fragmented, with the presence of numerous global and regional market players. Major players in the market include Alfa Level, Dall Energy, Danfoss Group, ENGIE, Fortum, FVB Energy Inc., GE, Helen, Ramboll, Statkraft, Uniper, Vattenfall, and Veolia.

Alfa Laval AB, founded in 1883 by Gustaf de Laval and Oscar Lamm, has evolved into a global company providing specialized products and solutions for heat transfer, separation, and fluid handling. Headquartered in Lund, Sweden, the company operates in over 100 countries. Alfa Laval's diverse product portfolio includes heat exchangers, pumps, valves, and centrifuges, which are essential in district heating and various industries such as energy, food processing, pharmaceuticals, and waste treatment.

Danfoss Group, established in 1933 by Mads Clausen in Nordborg, Denmark, has grown into a prominent multinational corporation specializing in engineering solutions that enhance energy efficiency across various sectors. Danfoss operates in more than 100 countries, focusing on technologies that empower industries to create sustainable and efficient systems. The company is structured into three main business segments: Danfoss Climate Solutions, Danfoss Drives, and Danfoss Power Solutions. It provides advanced solutions that optimize the efficiency of district heating systems.

List of Key Companies in District Heating Market

- Alfa Level

- Dall Energy

- Danfoss Group

- ENGIE

- Fortum

- FVB Energy Inc.

- GE

- Helen

- Ramboll

- Statkraft

- Uniper

- Vattenfall

- Veolia

District Heating Industry Developments

February 2024: Evonik and Uniper launched a sustainable district heating project, Technical Options for Thermal Energy Recovery (TORTE), for Germany’s Ruhr region.

March 2022: Fortum and Microsoft collaborated to heat services, homes, and businesses with sustainable waste heat from new data center region through district heating system.

August 2023: Europroject Ltd., introduced LIFE Low2HighDH, new district heating project. The project is dedicated to promoting the utilisation of waste heat technologiesor low-grade in District Heating and highlighting their benefits.

District Heating Market Segmentation

By Energy Source Outlook (Revenue – USD Billion, 2020–2034)

- Renewable Energy

- Fossil Fuels

- Waste Heat

By Application Outlook (Revenue – USD Billion, 2020–2034)

- Residential

- Commercial

- Industrial

By Technology Outlook (Revenue – USD Billion, 2020–2034)

- Conventional District Heating

- Smart District Heating

By Regional Outlook (Revenue – USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

District Heating Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 199.73 billion |

|

Revenue Forecast in 2025 |

USD 209.47 billion |

|

Revenue Forecast by 2034 |

USD 327.20 billion |

|

CAGR |

5.1% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global district heating market size was valued at USD 199.73 billion in 2024 and is projected to grow to USD 327.20 billion by 2034.

• The global market is projected to grow at a CAGR of 5.1% during the forecast period.

• Europe had the largest share of the global market in 2024.

• Some of the key players in the market are Alfa Level, Dall Energy, Danfoss Group, ENGIE, Fortum, FVB Energy Inc., GE, Helen, Ramboll, Statkraft, Uniper, Vattenfall, and Veolia.

• The residential segment dominated the market in 2024.

© 2025 Polaris Market Research and Consulting. All rights reserved