Diagnostic Imaging Services Market Share, Size, Trends, Industry Analysis Report, By Application (Neurology, Orthopedics, Cardiovascular, Oncology, Ultrasound, Obstetrics & Gynecology, and Other Applications); By End-Use; By Type; By Region; Segment Forecast, 2022 – 2030

- Published Date:Sep-2022

- Pages: 114

- Format: PDF

- Report ID: PM2584

- Base Year: 2021

- Historical Data: 2018 - 2020

Report Outlook

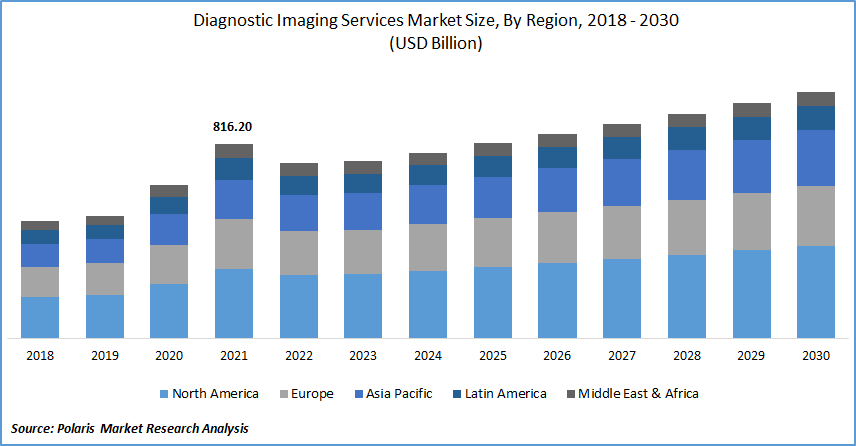

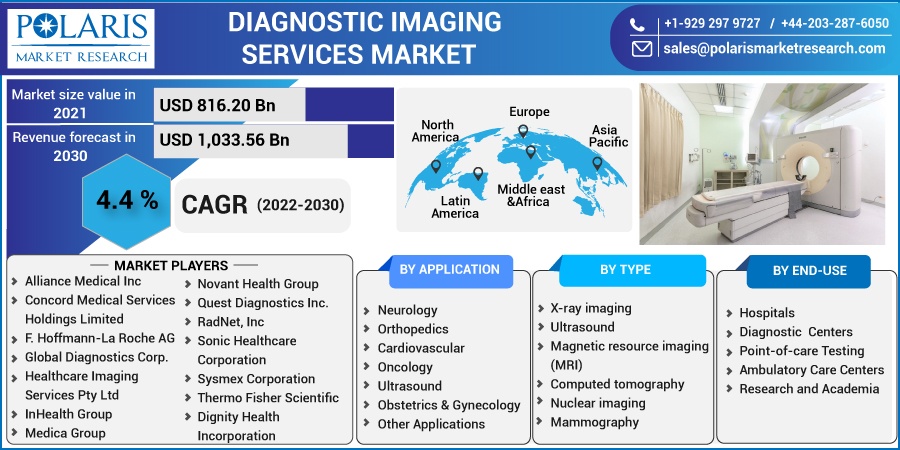

The global Diagnostic Imaging Services market was valued at USD 816.20 billion in 2021 and is expected to grow at a CAGR of 4.4% during the forecast period. Imaging is an appropriate procedure because it provides vital information safely and efficiently. Image processing services include sonograms, nuclear medicine scans, X-Ray, MRIs, and Computed imaging, all of which are non-invasive procedures for diagnosing various diseases.

Know more about this report: Request for sample pages

Know more about this report: Request for sample pages

Growing technological developments in MRI modality and expanding the implementation of MRI in the healthcare profession are the key drivers supplementing the growth of the Diagnostic Imaging Services market, which has also boosted the global Diagnostic Imaging Services market. Furthermore, rising healthcare insurance for medical imaging offerings, as well as new service debuts by key players, will support Diagnostic Imaging Services market growth throughout the forecast period.

The increasing product launches for advanced testing services are the factor driving the Diagnostic Imaging Services market growth over the forecast period. For instance, in August 2022, PepiPets announced the introduction of new mobile testing services. The above new service, the announcement was made in a company release, will enable the customers to receive diagnostic procedures for their pets right at home. PepiPets hopes that the at-home relation to performance will make pets more pleasant with the methodology while also saving time on travel to and from an initial in-person appointment.

The COVID-19 bubonic plague had implications on the diagnostic imaging market globally, both positively and negatively. One of the most serious implications was that hospitals and imaging centers reduced the number of procedures performed.

Furthermore, as a result of the COVID-19 outbreak, the estimated price of these procedures will be enhanced in 2020. This decline, however, used to have a short-term negative impact on the Diagnostic Imaging Services market. The lengthy fundamental drivers influencing market demand for diagnostic equipment will change little or nothing. These factors contributed to a reduction in the number of procedures performed globally, resulting in negative growth in Diagnostic Imaging Services.

Know more about this report: Request for sample pages

Know more about this report: Request for sample pages

Industry Dynamics

Growth Drivers

The rising research and development funding by the public and private players for Diagnostic Imaging Services in the market is the factor boosting the market growth over the forecast period. For instance, in November 2021, the UK Government announced financial support for the National Health Service (NHS) of £248 million ($334.6 million) to digitize diagnostic testing care and address the issue of patient waiting times.

That financial support has been designated for efficient innovations to the NHS’ procedures, to improve the entire procedure of ordering, being able to perform, and evaluating tests to identify and treat health issues as quickly as possible.

Also, in May 2021, Truepill confirmed the systematic unveiling of its diagnostic testing service, a significant step toward the company’s goal of delivering 80% of healthcare digitally in the coming years. Truepill's API innovation underpins the new service, which can be fully integrated with the company's current telehealth and prescribing fulfillment Diagnostic Imaging Services. Therefore, the rising funding has expanded medical services, which are boosting the market growth over the forecast period.

Report Segmentation

The market is primarily segmented based on application, end-use, products, and region.

|

By Application |

By Type |

By End-Use |

By Region |

|

|

|

|

Know more about this report: Request for sample pages

Neurology Segment is Expected to Witness Fastest Growth

The rise in neurobiological disorder instances and stroke occurrences is most likely to contribute to the segment's dominance. Diagnostic Imaging Services may help doctors confirm and diagnose neurological disorders. Parkinson's disease, after Alzheimer's disease, is the most common disintegrating neurological disorder.

According to a Parkinson's Foundation article, approximately 1 million people in the United States have Parkinson's disease, with that amount expected to increase to 1.2 million by 2030. Because of the higher incidence of cancer in the United States, oncology is the second most dominant component and is anticipated to grow during the forecast period.

Because of the growing number of cardiovascular cases in the United States, the cardiology segment is expected to hold a significant market share during the forecast period. Following the CDC, one person dies from cardiovascular disease every 36 seconds in the United States, and approximately 659,000 individuals die from heart disease each year.

CT Scans Segment Industry Accounted for the Highest Market Share in 2021

The segment's overall dominant market share is due to computed imaging as a result of a rise in the amount of CT scan procedures, as well as its relatively high price. According to OECD data, the number of CT exams performed in the United States in 2017 was 83.3 million and 91.6 million in 2019.

CT exam processes increased by around 3.1% in 2019 compared to 2018. Furthermore, the rise in the aging population has been associated with an increase in the consumption of CT scan procedures. According to the United States Census Bureau, the aging population aged 65 and up accounts for approximately 16.5% of the nation's people.

Furthermore, the market demand for computed imaging has been steadily increasing. CT scanners ever since the beginning of the COVID-19 disease outbreak. CT scan of the chest is useful in getting diagnosed with COVID-19; almost every patient requires a CT scan to supervise disease progression.

As a result, even with the postponed procedures, the increased supply of disease treatment has favored the CT scanner segment. Because of product announcements with technologically advanced features, the X-ray segment will be the second most dominant segment.

Home Diagnosis is Expected to Hold the Significant Revenue Share

Home diagnostic tests have emerged as a protector for people restricted at home as a result of the disease outbreak last year, and great experiences have prompted a mindset change among the general public from lab visits to at-home doctor visits. Home diagnostics, like remote patient monitoring, is still in its infancy and lacks absorption at the moment, but this is likely to change as people recognize the comfort of at-home tests.

The prevalence of home health tests also enables patients to accomplish the overall healthcare management succession from home, from blood tests to teleconsultation with doctors to medication delivery. People would most likely only visit a lab in the future for complex and specialized tests. Home health screening tests for chronic health conditions are progressively becoming such a habit as people recognize the potential and convenience they provide.

The Demand in North America is Expected to Witness Significant Market Growth

The expanding geriatric population, growing patient knowledge and understanding of the significance of laboratory tests, and the increased incidences of infectious and chronic conditions are driving the clinical services market in the region. The rising number of COVID-19 infections has resulted in increased financial support and testing, which has bolstered overall market growth. According to the CDC, four out of every ten people in the United States have two or more long-term diseases, and 6 out of every 10 adults suffer from a chronic condition.

Chronic diseases, including cancer, cardiovascular disease, and obesity, are the foremost causes of death and disabilities in the United States, accounting for the majority of the USD 3.8 quadrillion spent on medical care each year. This has increased the demand for improved treatment with effective management, driving the marketplace in the region even further. As a result, the growing incidence of chronic diseases and infectious diseases, as well as increased recognition of the significance of laboratory tests, are expected to propel market expansion in the country.

APAC is expected to grow at the fastest CAGR over the forecast period, attributed to promoting health infrastructure, rising investments in medical testing, a continuing to improve reimbursement scenario, and expanding insurance benefits in several APAC countries. Further, in June 2022, Bertelsmann India Investments and General Catalyst led a $25 million Series B financing round for Orange Health.

Competitive Insight

Some of the major players operating in the global market include Alliance Medical Inc, Concord Medical Services Holdings Limited, Dignity Health Incorporation, F. Hoffmann-La Roche AG, Global Diagnostics Corp., Healthcare Imaging Services Pty Ltd, InHealth Group, Medica Group, Novant Health Group, Quest Diagnostics Inc., RadNet, Inc, Sonic Healthcare Corporation, Sysmex Corporation, and Thermo Fisher Scientific.

Recent Developments

- In June 2022, Orange Health must have announced the commencement of its services in New Delhi as a component of its optimistic geographical expansion strategy. Customers in the NCR region can now access a variety of Diagnostic Imaging Services in just 1 hour from the convenience of their homes, with the information provided in 6 hours.

- In March 2022, MedPlus Health Services opened a diagnoses hub in Gachibowli with PNDT and AERB authorizations. It is an expansion of the current Labs segment and would encompass radiology and pathophysiology services.

Diagnostic Imaging Services Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2021 |

USD 816.20 billion |

|

Revenue forecast in 2030 |

USD 1,033.56 billion |

|

CAGR |

4.4% from 2022 - 2030 |

|

Base year |

2021 |

|

Historical data |

2018 - 2020 |

|

Forecast period |

2022 - 2030 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2022 to 2030 |

|

Segments Covered |

By Application, By Type, By End-Use, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Alliance Medical Inc, Concord Medical Services Holdings Limited, Dignity Health Incorporation, F. Hoffmann-La Roche AG, Global Diagnostics Corp., Healthcare Imaging Services Pty Ltd, InHealth Group, Medica Group, Novant Health Group, Quest Diagnostics Inc., RadNet, Inc, Sonic Healthcare Corporation, Sysmex Corporation, and Thermo Fisher Scientific. |

© 2025 Polaris Market Research and Consulting. All rights reserved