Cold Flow Improvers Market Size, Share, Trends, Industry Analysis Report: By Type (Ethylene Vinyl Acetate, Polyalkyl Methacrylate, and Polyalpha Olefin), Application (Diesel Fuel, Lubricating Oil, and Aviation Fuel), End User (Automotive, Aerospace & Defense, and Others), and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Nov-2024

- Pages: 119

- Format: PDF

- Report ID: PM5257

- Base Year: 2024

- Historical Data: 2020-2023

Cold Flow Improvers Market Overview

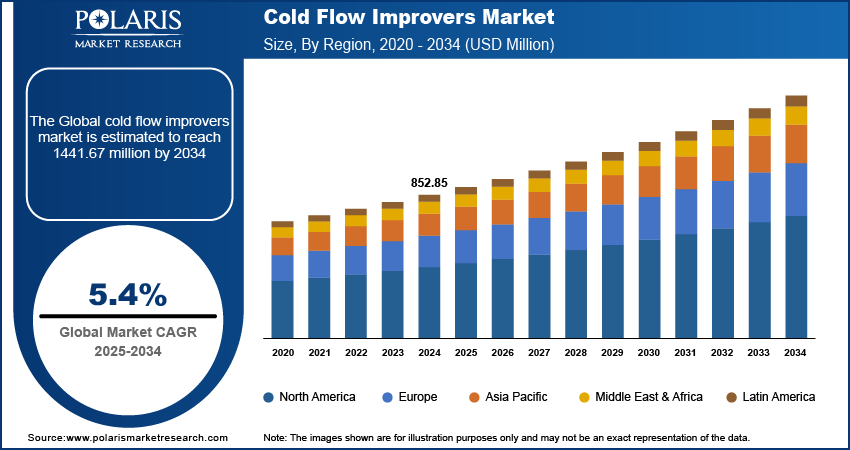

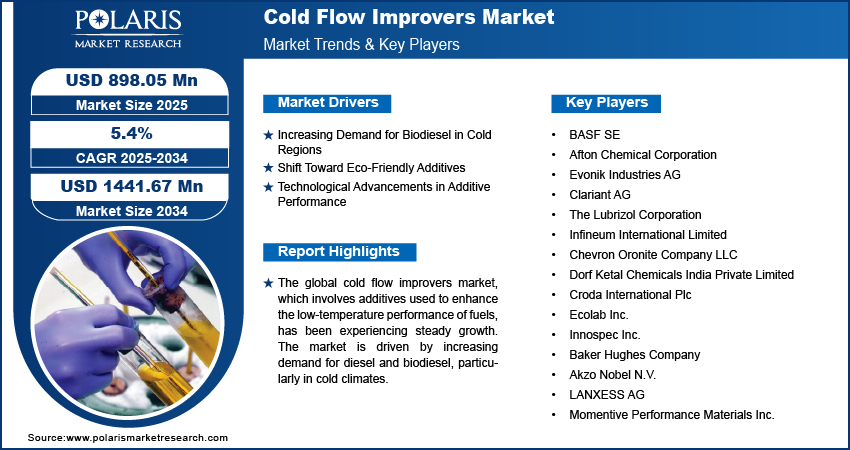

The cold flow improvers market size was valued at USD 852.85 million in 2024. The market is projected to grow from USD 898.05 million in 2025 to USD 1441.67 million by 2034, exhibiting a CAGR of 5.4% during 2025–2034.

The global cold flow improvers market, which involves additives used to enhance the low-temperature performance of fuels, has been experiencing steady growth. The market is driven by increasing demand for diesel and biodiesel, particularly in cold climates, where these additives are essential to prevent fuel gelling and maintain fluidity.

Trends in the market highlight a growing emphasis on the development of eco-friendly and bio-based cold flow improvers, driven by stringent environmental regulations and a rising preference for sustainable solutions. Additionally, advancements in additive technology are improving the efficacy of these products across diverse fuel types, further supporting market expansion.

To Understand More About this Research: Request a Free Sample Report

Cold Flow Improvers Market Drivers Analysis

Increasing Demand for Biodiesel in Cold Regions

Biodiesel, derived from renewable energy, is prone to gelling at low temperatures, making cold flow improvers essential for its effective use in cold climates. According to the US Energy Information Administration (EIA), the global biodiesel production reached 44 million liters in 2022, with significant consumption in Europe and North America. The heightened environmental awareness and regulations promoting biodiesel use have boosted the demand for cold flow improvers to ensure the fuel's operability during winter months. Thus, the increasing use of biodiesel, especially in colder regions, drives the cold flow improvers market growth.

Shift Toward Eco-Friendly Additives

There is a noticeable shift toward eco-friendly cold flow improvers as environmental regulations become stricter worldwide. For instance, the European Union's REACH regulation has prompted a move toward additives that comply with environmental safety standards. Traditional additives, while effective, often raise concerns due to their chemical composition and environmental impact. As a result, manufacturers are increasingly focusing on developing bio-based and less harmful cold flow improvers. This trend aligns with the broader push for sustainability in the chemical industry, encouraging innovation in cold flow improvers that minimize environmental footprints.

Technological Advancements in Additive Performance

Advancements in technology are significantly enhancing the performance of cold flow improvers, making them effective across a wider range of fuels and environmental conditions. Innovations in the additive formulation are addressing challenges such as fuel compatibility and performance consistency at varying temperatures. According to a report by the International Energy Agency (IEA), research and development efforts are leading to next-generation additives that can improve fuel efficiency and reduce emissions, particularly in the automotive sector. These technological advancements are improving the efficacy of cold flow improvers and driving their adoption across different fuel types, including ultra-low sulfur diesel (ULSD) and biodiesel blends.

Cold Flow Improvers Market Segment Analysis

Cold Flow Improvers Market Breakdown by Type

The cold flow improvers market, by type, is segmented into Ethylene Vinyl Acetate (EVA), Polyalkyl Methacrylate (PAMA), and Polyalpha Olefin (PAO), with each offering distinct benefits in enhancing the low-temperature performance of fuels. The Ethylene Vinyl Acetate (EVA) segment holds the largest market share, driven by its widespread application in diesel and biodiesel fuels due to its effective cold flow properties and cost-efficiency. EVA's versatility and compatibility with various fuel types make it a preferred choice among end users, particularly in colder climates where maintaining fuel fluidity is critical.

The Polyalkyl Methacrylate (PAMA) segment is registering the highest growth rate in the market. The increasing demand for biodiesel and ultra-low sulfur diesel (ULSD), which require advanced cold flow improvers, is fueling the adoption of PAMA-based additives. PAMA's superior performance in improving cold filter plugging points and pour points, especially in biodiesel blends, is driving its rapid market expansion. Moreover, its adaptability to different fuel compositions and the ongoing shift toward more environmentally friendly additives contribute to the segment's growth.

Cold Flow Improvers Market Breakdown by Application

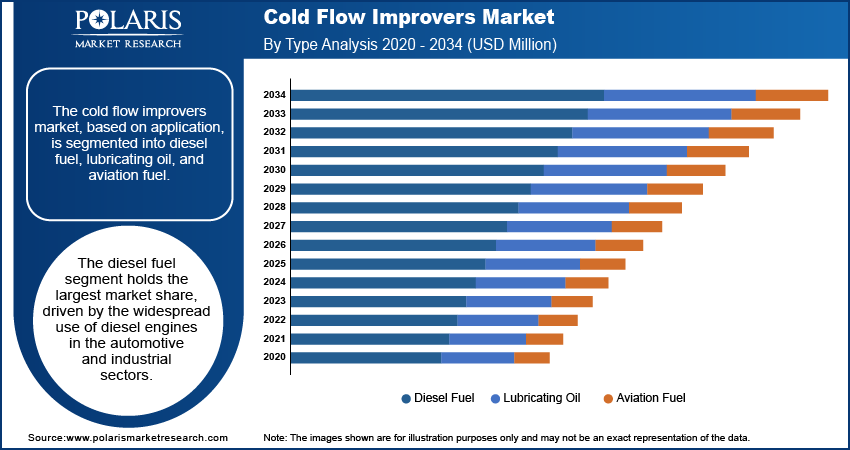

The cold flow improvers market, based on application, is segmented into diesel fuel, lubricating oil, and aviation fuel. The diesel fuel segment holds the largest market share, driven by the widespread use of diesel engines in automotive and industrial sectors, particularly in regions with harsh winters. The need to prevent fuel gelling and ensure smooth engine operation in cold climates has made cold flow improvers essential for diesel applications. This segment's dominance is further supported by the increasing consumption of diesel in emerging markets.

The aviation fuel segment is registering the highest growth rate within the market, as the aviation industry places a strong emphasis on fuel performance and safety under extreme conditions. Cold flow improvers are crucial in aviation fuels to prevent fuel line blockages and ensure reliable engine performance at high altitudes and low temperatures. The growing air travel demand and expansion of airline fleets, particularly in Asia Pacific and the Middle East, are driving the adoption of cold flow improvers in this segment. Additionally, the industry's focus on maintaining stringent safety standards and improving fuel efficiency is further contributing to the segment's rapid growth.

Cold Flow Improvers Market Breakdown by End User

The cold flow improvers market, by end user, is segmented into automotive, aerospace & defense, and others. The market showcases varying demands based on the unique requirements of each industry. The automotive segment holds the largest market share, largely due to the extensive use of diesel engines in passenger vehicles, commercial trucks, and heavy-duty machinery. Cold flow improvers are essential in this sector to prevent fuel issues in low-temperature environments, ensuring consistent engine performance and fuel efficiency. The rising production of vehicles and increasing diesel consumption, particularly in regions with cold climates, further solidify the automotive segment's dominant position in the market.

The aerospace & defense segment is registering the highest growth rate, driven by the critical need for fuel reliability and safety in extreme conditions. Cold flow improvers are vital in the aerospace & defense sector to maintain the operability of aviation fuels and lubricants under high-altitude and cold-weather conditions. The expansion of military operations in diverse geographies and the growth of the global aviation industry, particularly in emerging markets, are key factors contributing to the increasing demand for cold flow improvers in this segment. Additionally, the industry's stringent regulatory standards and focus on enhancing fuel performance are accelerating the market growth for this segment.

Cold Flow Improvers Market Share by Region

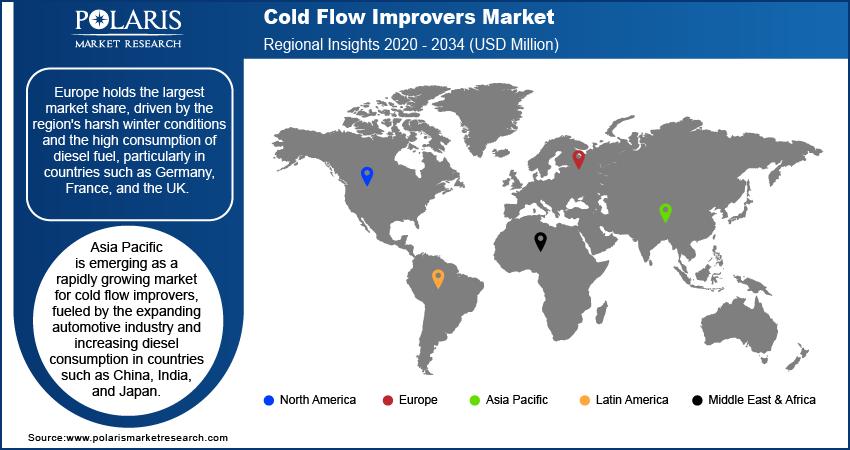

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Europe holds the largest market share, driven by the region's harsh winter conditions and the high consumption of diesel fuel, particularly in countries such as Germany, France, and the UK. The stringent environmental regulations in Europe promote the use of biodiesel and ultra-low sulfur diesel (ULSD), which further fuels the demand for cold flow improvers. The region's focus on reducing emissions and enhancing fuel efficiency is also propelling market growth.

Europe holds a significant position in the cold flow improvers market, driven primarily by its harsh winter conditions and the extensive use of diesel vehicles. Countries such as Germany, France, and the UK are major contributors to the market, where the adoption of diesel and biodiesel fuels is prevalent. The stringent environmental regulations across the European Union, particularly those aimed at reducing greenhouse gas emissions and promoting cleaner fuels, have further propelled the demand for cold flow improvers. The region's focus on sustainability and fuel efficiency, coupled with advanced automotive and industrial sectors, ensures continued growth and dominance in the market.

Asia Pacific is emerging as a rapidly growing market for cold flow improvers, fueled by the expanding automotive industry and increasing diesel consumption in countries such as China, India, and Japan. The region's diverse climate, which includes colder areas in the northern regions, drives the need for cold flow improvers to ensure fuel efficiency and reliability. Additionally, the growing adoption of biodiesel in response to rising environmental concerns and the push for cleaner energy alternatives boost the demand for cold flow improvers. The region's dynamic industrial growth and the expansion of the aviation sector further contribute to the increasing market opportunities in Asia Pacific.

Cold Flow Improvers Market – Key Players and Competitive Insights

BASF SE, Afton Chemical Corporation, Evonik Industries AG, Clariant AG, The Lubrizol Corporation, Infineum International Limited, Chevron Oronite Company LLC, Dorf Ketal Chemicals India Private Limited, Croda International Plc, Ecolab Inc., Innospec Inc., Baker Hughes Company, Akzo Nobel N.V., LANXESS AG, and Momentive Performance Materials Inc are among the key players in the cold flow improvers market. These companies remain active in the market, focusing on the development and distribution of cold flow improvers for various fuel applications, including diesel, aviation, and lubricating oils.

The competitive landscape of the cold flow improvers market is characterized by continuous innovation and product development, driven by the need to meet evolving regulatory standards and customer demands. Companies such as BASF SE and Clariant AG are known for their extensive research and development efforts, leading to the introduction of more efficient and environmentally friendly cold flow improvers. Afton Chemical Corporation and Evonik Industries AG focus on expanding their product portfolios to cater to different fuel types and applications, while also enhancing their global distribution networks to reach a broader customer base.

The cold flow improvers market is witnessing increasing collaborations and strategic partnerships among key players to leverage technological advancements and strengthen their market presence. For instance, Chevron Oronite and Infineum International have been actively involved in joint ventures and alliances aimed at optimizing their additive technologies. Companies such as Croda International and LANXESS AG are also expanding their production capacities and investing in new technologies to improve the performance of cold flow improvers across various climatic conditions. This competitive environment encourages innovation and ensures that the market continues to evolve, meeting the demands of various industries and applications.

BASF SE is a global player in the cold flow improvers market, known for its extensive chemical product portfolio, which includes cold flow additives for diesel and biodiesel fuels. The company is focused on research and development, particularly in creating more efficient and environmentally friendly solutions.

Afton Chemical Corporation is another significant company in the market, specializing in the production of fuel additives, including cold flow improvers. Afton’s products are widely used in automotive and industrial applications to ensure fuel reliability in cold climates.

Key Companies in Cold Flow Improvers Market

- BASF SE

- Afton Chemical Corporation

- Evonik Industries AG

- Clariant AG

- The Lubrizol Corporation

- Infineum International Limited

- Chevron Oronite Company LLC

- Dorf Ketal Chemicals India Private Limited

- Croda International Plc

- Ecolab Inc.

- Innospec Inc.

- Baker Hughes Company

- Akzo Nobel N.V.

- LANXESS AG

- Momentive Performance Materials Inc.

Cold Flow Improvers Market Developments

- In April 2023, BASF announced the launch of a new bio-based cold flow improver designed to enhance the low-temperature performance of biodiesel, aligning with global trends toward sustainability.

- In March 2023, Afton Chemical introduced a new generation of cold flow improvers aimed at improving fuel efficiency and reducing emissions, which reflects the company’s commitment to innovation and compliance with changing environmental regulations.

Cold Flow Improvers Market Segmentation

By Type Outlook (Revenue – USD Million, 2020–2034)

- Ethylene Vinyl Acetate

- Polyalkyl Methacrylate

- Polyalpha Olefin

By Application Outlook (Revenue – USD Million, 2020–2034)

- Diesel Fuel

- Lubricating Oil

- Aviation Fuel

By End User Outlook (Revenue – USD Million, 2020–2034)

- Automotive

- Aerospace & Defense

- Others

By Regional Outlook (Revenue – USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Cold Flow Improvers Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 852.85 million |

|

Market Size Value in 2025 |

USD 898.05 million |

|

Revenue Forecast in 2034 |

USD 1441.67 million |

|

CAGR |

5.4% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD Million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global cold flow improvers market size was valued at USD 852.85 million in 2024 and is projected to grow to USD 1441.67 million by 2034.

The global market is projected to register a CAGR of 5.4% during 2025–2034.

Europe accounted for the largest share of the global market.

Key players in the cold flow improvers market are BASF SE, Afton Chemical Corporation, Evonik Industries AG, Clariant AG, The Lubrizol Corporation, Infineum International Limited, Chevron Oronite Company LLC, Dorf Ketal Chemicals India Private Limited, Croda International Plc, Ecolab Inc., Innospec Inc., Baker Hughes Company, Akzo Nobel N.V., LANXESS AG, and Momentive Performance Materials Inc.

The Polyalkyl Methacrylate segment accounted for the largest share of the global market.

The diesel fuel segment accounted for the largest share of the global market.

© 2025 Polaris Market Research and Consulting. All rights reserved