Chronic Care Management Software Market Share, Size, Trends, Industry Analysis Report, By Component (Software, Solution); By Deployment; By Disease Type; By End-user; By Region; Segment Forecast, 2024 - 2032

- Published Date:Mar-2024

- Pages: 119

- Format: PDF

- Report ID: PM4483

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

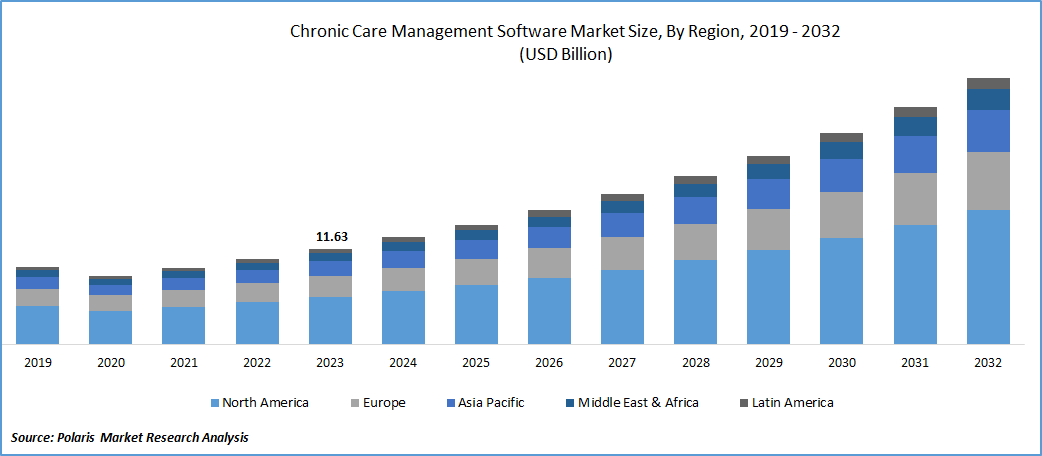

The global chronic care management software market was valued at USD 11.63 billion in 2023 and is expected to grow at a CAGR of 12.0% during the forecast period.

The worldwide initiatives that are implemented to shift the risk burden from payers to providers is one the major factor driving the market. Moreover, factors such as growing ageing population, need to reduce healthcare costs, and various regulations promoting patient-centric care boost the use of healthcare information technology (HCIT) solutions thereby, fuelling the market growth. The use of HCIT solutions can improve the efficiency of healthcare delivery and cut costs. Therefore, the healthcare professionals focus on the responsibility for the medical treatment that is being provided to the patients.

To Understand More About this Research:Request a Free Sample Report

- For instance, in June 2023, the University of Queensland has received USD 6.0 million from the Medical Research Future Fund (MRFF) National Critical Research Infrastructure scheme for data based better management of various diseases such as osteoarthritis, rheumatoid arthritis, & diabetes.

Chronic care management helps the patients with two or more chronic conditions in managing their disease. For instance, according to National Center for Chronic Disease Prevention and Health Promotion (NCCDPHP), 4 in 10 adults in the U.S. have two or more chronic diseases. Such high occurrence rate of chronic diseases is expected to increase the demand for chronic care management thereby, fostering the market growth.

However, a high risk of data breaches can result from several factors, including inadequate staff training, adherence to outmoded policies and procedures, lack of internal control over patient data, and non-adherence to current procedures and policies. Such factors leading to data breaches is likely to hinder the adoption of HCIT solutions, thereby hampering the market growth soon. Moreover, screen loads caused by an inadequate network and neglected server maintenance can slow down the clinical workflow. Such issues in the clinical workflow is expected to hamper the market to a certain extent.

Growth Drivers

- Worldwide initiatives to promote the adoption of HCIT solutions is anticipated to fuel the overall market

Many initiatives are being carried out globally to transfer the risk from healthcare payers to providers. This shift boosts the use of healthcare information technology (HCIT) solutions such as chronic care management solutions. The installation of chronic care management solutions helps to reduce the unnecessary costs and increase the effectiveness of healthcare delivery. Such benefits associated with the adoption of HCIT solutions are expected to propel the chronic care management software market growth in the long run.

For instance, the chronic care management solution from Medsien, Inc. offers various advantages such as remote patient outreach, reduced administrative burden, and automated billing & reporting. Moreover, the payment models of HCIT solutions aim to transfer to the risk from payers to providers by encouraging healthcare providers to take the responsibility for the care they offer. Such strong aim on encouraging healthcare providers on their accountability for the care is expected to contribute to the market growth during the forecast period.

Report Segmentation

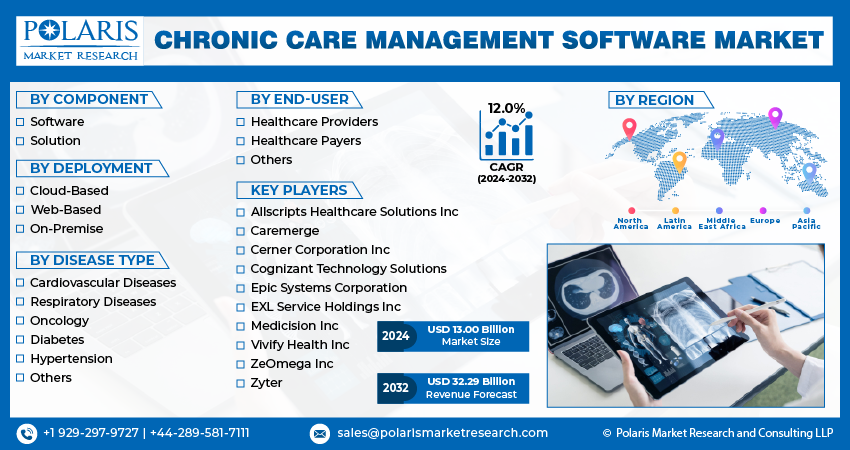

The market is primarily segmented based on component, deployment, disease type, end-user, and region.

|

By Component |

By Deployment |

By Disease Type |

By End-user |

By Region |

|

|

Diseases

|

|

|

To Understand the Scope of this Report:Speak to Analyst

By Component Analysis

- The software segment is expected to continue its dominance during the forecast period

In 2023, the software segment held the significant share. This share is attributed mainly attributed to the affordable price of the software and its ease of use. Software offers well-coordinated and effective medical care. It also helps healthcare professionals to avoid surgical errors, diagnose patients accurately, and monitor a patient’s vitals and medicines. Such benefits coupled with the increasing need for the management of chronic care are expected to propel the overall market growth during the forecast timeframe.

By Deployment Analysis

- Advantages of web-based software contributed to its largest market share in 2023

The web-based segment accounted for the largest market. This is primarily due to easy accessibility, less maintenance, simple deployment, and ease of use are mainly contributing to the large share of the segment. Moreover, cross-platform compatibility and lower cost of routine maintenance are also propelling the segmental growth.

The cloud-based segment will grow with substantial pace. This growth is due to accessibility to information from any device or place and minimal interaction of service providers. Moreover, advanced security and data loss prevention offered by cloud-based software is another factor attracting a large population pool.

By Disease Type Analysis

- Hypertension segment dominated the global market in 2023

Hypertension segment held the significant market share. This dominance is due to increasing geriatric population, large group of patients suffering from hypertension, and growing focus of market players on improving the treatment of hypertension though new product development and launches. For instance, according to Centers for Disease Control and Prevention (CDC), nearly half of adults in the U.S. have hypertension. Such large group of patients is expected to increase the adoption of chronic care management software in the upcoming years.

By End-user Analysis

- The healthcare providers segment dominated the market in 2023

The healthcare providers segment accounted for the largest share of the market in 2023. The large share is attributed to the factors such as the need for faster services, better healthcare quality, a growing patient base, and an increasing demand for patient-centric care. Moreover, the rising prevalence of chronic disease is stimulating the healthcare providers to provide better treatment options for the management of chronic diseases. This, in turn, will increase the adoption of software among healthcare providers.

Regional Insights

- North America held the largest market share in 2023

North America region dominated the global market. The growing number of patients suffering from chronic diseases such as heart failure, hypertension, cancer, diabetes, and COPD is one of the major factors contributing to the market growth across the region. For instance, according to the data published by the Heart and Stroke Foundation of Canada in February 2022, 100,000 people are diagnosed with heart failure each year.

Moreover, the initiatives to improve the overall health management across this region is also supporting the market growth. For instance, in September 2023, the Centers for Medicare & Medicaid Services (CMS) announced a new alternative, state total cost of care (TCOC) model named All-Payer Health Equity Approaches and Development (AHEAD) model. This model aims to work with states to reduce the disparities in the health outcomes, enhance population health, and control the growth in health care costs.

The market in Asia Pacific region will grow rapidly. Rise in geriatric population coupled with increasing number of people diagnosing with chronic diseases such as asthma, diabetes and COPD are expected to fuel the market growth across the region. For instance, according to the ‘India Ageing Report 2023’, the United Nations Population Fund (UNFPA) in collaboration with the International Institute for Population Sciences (IIPS), as on July 1, 2022, the persons aged more than 60 comprised around 10.5% of the country’s total population and is expected to reach 20.8% of the country’s population by 2050. Moreover, increasing focus of healthcare facilities towards the adoption and installation of HCIT solutions across India and Southeast Asia are expected to further propel the region’s growth.

Key Market Players & Competitive Insights

Market is fragmented due to the presence of many small and medium-sized companies. The companies operating in the market are constantly focusing on the strategic initiatives such as product portfolio expansion, collaborations, and partnerships to strengthen their share in the global market. For instance, in January 2023, Cadence and Ardent Health Services introduced a remote care management service to enhance patient outcomes and care outside of clinic settings.

Some of the major players operating in the global market include:

- Allscripts Healthcare Solutions Inc

- Caremerge

- Cerner Corporation Inc

- Cognizant Technology Solutions

- Epic Systems Corporation

- EXL Service Holdings Inc

- Medicision Inc

- Vivify Health Inc

- ZeOmega Inc

- Zyter

Recent Developments

- For instance, in April 2022, CareCloud, Inc. announced its new offering named CareCloud Wellness which is a software-based service for the chronic care management of high-risk patients with multiple chronic conditions.

Chronic Care Management Software Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 13.00 billion |

|

Revenue forecast in 2032 |

USD 32.29 billion |

|

CAGR |

12.0% from 2024 – 2032 |

|

Base year |

2023 |

|

Historical data |

2019 – 2022 |

|

Forecast period |

2024 – 2032 |

|

Quantitative units |

Revenue in USD billion and CAGR from 2024 to 2032 |

|

Segments covered |

By Component, By Deployment, By Disease Type, By End-user, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation. |

FAQ's

The key companies in Chronic Care Management Software Market include Allscripts Healthcare Solutions Inc, Caremerge, EXL Service Holdings Inc.

The global chronic care management software market is expected to grow at a CAGR of 12.0% during the forecast period.

Chronic Care Management Software Market report covering key segments are component, deployment, disease type, end-user, and region.

The key driving factors in Chronic Care Management Software Market are Worldwide initiatives to promote the adoption of HCIT solutions is anticipated to fuel the overall market.

Chronic Care Management Software Market Size Worth 32.29 Billion By 2032.

© 2025 Polaris Market Research and Consulting. All rights reserved