Carbon Capture and Storage Market Share, Size, Trends, Industry Analysis Report, By Capture Type (Pre-combustion, Industrial separation, Oxyfuel-combustion, Post-combustion); By Application; By Region, And Segment Forecasts, 2024-2032

- Published Date:Jan-2024

- Pages: 114

- Format: PDF

- Report ID: PM1619

- Base Year: 2023

- Historical Data: 2019-2022

Report Outlook

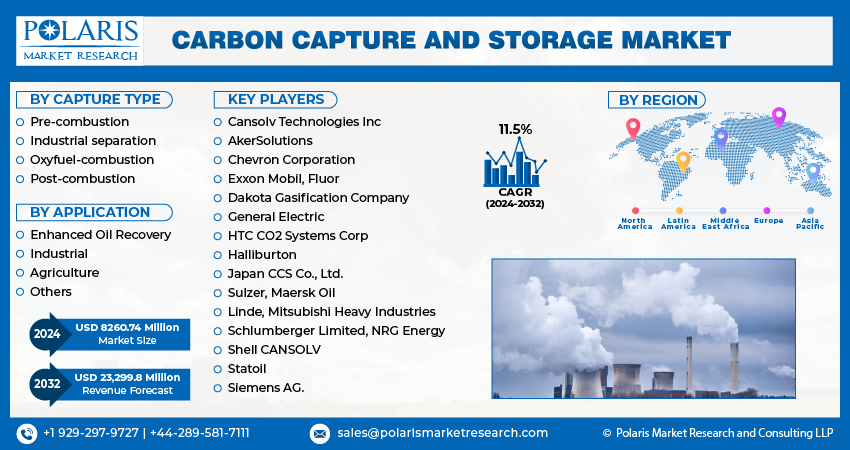

The global carbon capture and storage market was valued at USD 7388.85 million in 2023 and is expected to grow at a CAGR of 11.5% during the forecast period. The "Carbon Capture and Storage (CCS) Market" process involves capturing carbon dioxide emissions from sources such as coal-fired power plants, followed by the reuse or storage of the captured carbon dioxide gas. This approach aims to mitigate environmental impact, reduce pollution, and protect the environment.

The research report offers a quantitative and qualitative analysis of the Carbon Capture and Storage Market to enable effective decision-making. It covers the key trends and growth opportunities anticipated to have a favorable impact on the market. Besides, the study covers segment and regional revenue forecasts for market assessment.

To Understand More About this Research: Request a Free Sample Report

Growing environmental concerns over the harmful impact of carbon emissions have spurred the adoption of Carbon Capture & Storage (CCS) technology. Governments worldwide are actively promoting the implementation of this technology through pilot projects in various industries. CCS technology is recognized for its potential as a large-scale solution to achieve ambitious CO2 emission reduction targets and address climate control objectives.

With advancing technology, the offshore oil & gas industry is expected to expand due to increased utilization of gas injection Enhanced Oil Recovery methods. Carbon dioxide plays a crucial role in the extraction of crude oil. The demand for gas injection EOR techniques, both for onshore and offshore wells, is driven by the depletion of oil reservoirs. This trend is expected to fuel the growth of the Carbon Capture and Storage (CCS) market's development, as ERO is growing for CO2 activities in the gas & oil sector.

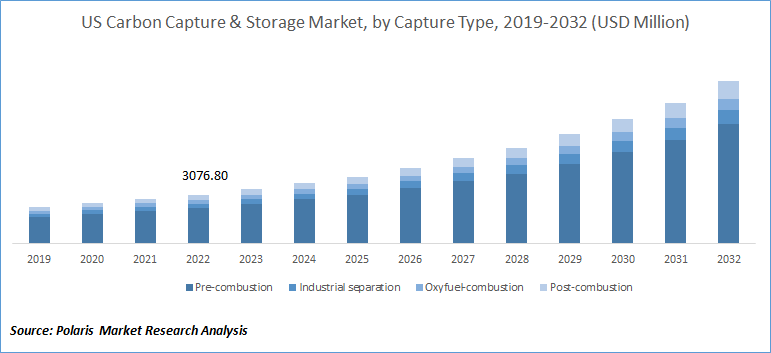

In 2022, the United States was projected to dominate the global industry due to high-capacity CCS plants and the increasing adoption of CO2 in EOR techniques. With the advancement of shale gas technology and the current government's reduced emphasis on carbon capture, the CCUS market in the country is projected to experience sluggish growth. Consequently, North America is anticipated to gain a larger market share. However, The Asia Pacific region is poised for a significant increase in the carbon capture, utilization, and storage (CCUS) market due to the large-scale development projects in the area.

Natural gas, gasoline, petroleum products, and diesel are the primary fuel origins. However, their production and exploration pose significant environmental risks. On the other hand, natural gas is considered an alternative fuel for sustainable development due to its lower carbon emissions, ability to slow global warming, and reduced greenhouse gas (GHG) emissions. The US government has implemented various laws and regulations to mitigate the risks associated with gasoline and diesel use and promote the use of natural gas. Countries with significant natural gas reserves are now considering the adoption of carbon capture and storage technologies to reduce carbon emissions further and promote sustainable practices.

Industry Dynamics

Growth Drivers

Implementing Sustainable Technologies for Manufacturing

The carbon capture and storage market are driven by several factors contributing to its growth and impact on substantial decarbonization. One key driver is the potential for carbon capture and storage technologies to facilitate large-scale decarbonization across various sectors within a relatively short period. These technologies can capture and store carbon dioxide emissions, reducing greenhouse gas emissions and mitigating climate change impacts.

Additionally, implementing sustainable technologies in industries such as manufacturing and chemicals drives the demand for carbon capture and storage solutions. These industries recognize the need to reduce their carbon footprint and comply with emission reduction targets. By adopting carbon capture and storage technologies, they can effectively capture and store CO2 emissions, enabling them to meet regulatory requirements and improve their environmental performance.

Furthermore, stringent government regulations on emissions play a significant role in driving the carbon capture and storage market. Governments worldwide impose stricter emission standards and restrictions to combat climate change and reduce carbon emissions. It creates a favorable environment for adopting carbon capture and storage technologies as industries strive to comply with these regulations and avoid penalties.

Report Segmentation

The market is primarily segmented based on capture type, application, and region.

|

By Capture Type |

By Application |

By Region |

|

|

|

To Understand the Scope of this Report: Speak to Analyst

The Pre-combustion Segment Held the Largest Market Share Over the Forecast Period

In 2022, the pre-combustion segment held the largest market share over the forecast period. This combustion CO2 captures, which involve water gas shift removal and reaction with the Acid Gas Removal (AGR) method, are being commercially implemented worldwide.

One of the advantages of employing this capture technology under pressure is its lower energy penalty compared to the current PCC (Post-Combustion Capture) technology. With approximately 90% CO2 capture, the energy penalty for pre-combustion capture is around 20%, whereas the current PCC technology incurs an energy penalty of roughly 30%.

Furthermore, post-combustion capture technology is expected to witness significant growth. Factors such as increased energy generation, the development of advanced amine systems, and the integration of heat systems are anticipated to drive the demand for post-combustion capture technology during the forecast period.

The Enhanced Oil Recovery Segment Held the Fastest Market Share in 2022

In 2022, the Enhanced Oil Recovery (EOR) segment held the fastest market share in the Carbon Capture and Storage (CCS) market. There is a rising demand for crude oil from various sectors, such as residential, industrial, and commercial end-use industries. For this, the oil and gas industry are exploring new ways to extract more oil from existing reservoirs, including using EOR techniques.

The growing demand for crude oil and the need to comply with government regulations has propelled the EOR segment to hold the fastest market share in the CCS market. The integration of CO2 capture and storage technologies in the oil and gas industry has not only helped enhance oil recovery but also reduced the environmental impact associated with the production and combustion of fossil fuels.

The North America Dominated the Global Market in 2022

North America dominated the global market in 2022 and is poised to maintain its dominance in the forecast period. Government initiatives and investments to reduce CO2 emissions will drive industry growth. For example, USAID's commitment to helping partner nations prevent six billion metric tons of CO2-equivalent pollution by 2030 demonstrates the region's dedication to environmental sustainability. This reduction is equivalent to the entire annual emissions of the United States or removing over one billion gasoline-powered cars from the streets for a year.

Asia Pacific is poised for significant growth in the forecast period, driven by increasing government investments to curb CO2 emissions. The region's robust manufacturing industries, particularly in countries like China and India, contribute to rising CO2 emissions, thereby creating lucrative opportunities for market expansion.

Competitive Insight

The major global market players include Cansolv Technologies Inc, AkerSolutions, Chevron Corporation, Exxon Mobil, Fluor, Dakota Gasification Company, General Electric, HTC CO2 Systems Corp, Halliburton, Japan CCS Co., Ltd., Sulzer, Maersk Oil, Linde, Mitsubishi Heavy Industries, Schlumberger Limited, NRG Energy, Shell CANSOLV, Statoil, and Siemens AG.

Recent Developments

- In December 2022, Petroleum Sarawak Bhd (Petros), a state-owned oil and gas company in Malaysia, entered into a partnership agreement with Posco Group, a South Korean steel-making company, to jointly develop the carbon capture and storage (CCS) business at a plant located in Sarawak, Malaysia.

- In August 2022, Shell PLC completed the acquisition of Sprang Energy Group, a renewable energy company dedicated to reducing carbon emissions. This strategic transaction aims to enhance Shell PLC's carbon capture and storage capabilities while expanding its market presence in the renewable energy sector.

- In June 2021, ExxonMobil Corporation, Shell, and the Guangdong Provincial Development and Reform Commission announced their collaboration to evaluate the feasibility of a carbon capture and storage project in the Dayawan petrochemical industrial park located in Huizhou, China. The project aims to assess the potential of capturing and storing carbon emissions in the region, contributing to environmental sustainability.

Carbon Capture and Storage Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 8260.74 million |

|

Revenue forecast in 2032 |

USD 23,299.8 million |

|

CAGR |

11.5% from 2024 - 2032 |

|

Base year |

2023 |

|

Historical data |

2019 - 2022 |

|

Forecast period |

2024 - 2032 |

|

Quantitative units |

Revenue in USD million and CAGR from 2024 to 2032 |

|

Segments covered |

By capture type, application, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Key companies |

Cansolv Technologies Inc, AkerSolutions, Chevron Corporation, Exxon Mobil, Fluor, Dakota Gasification Company, General Electric, HTC CO2 Systems Corp, Halliburton, Japan CCS Co., Ltd., Sulzer, Maersk Oil, Linde, Mitsubishi Heavy Industries, Schlumberger Limited, NRG Energy, Shell CANSOLV, Statoil, and Siemens AG |

Seeking a more personalized report that meets your specific business needs? At Polaris Market Research, we’ll customize the research report for you. Our custom research will comprehensively cover business data and information you need to make strategic decisions and stay ahead of the curve.

Browse Our Top Selling Reports

Calcium Formate Market Size, Share 2024 Research Report

Dental Insurance Market Size, Share 2024 Research Report

Advanced Therapy Medicinal Products CDMO Market Size, Share 2024 Research Report

Cell Therapy Market Size, Share 2024 Research Report

Animal Pregnancy Kit Market Size, Share 2024 Research Report

FAQ's

key companies in Carbon Capture and Storage Market are Cansolv Technologies Inc, AkerSolutions, Chevron Corporation, Exxon Mobil, Fluor, Dakota Gasification Company, General Electric.

The global carbon capture and storage market expected to grow at a CAGR of 11.5% during the forecast period.

The Carbon Capture and Storage Market report covering key are capture type, application, and region.

key driving factors in Carbon Capture and Storage Market are 1. Implementing sustainable technologies for manufacturing.

The global carbon capture and storage market size is expected to reach USD 23,299.8 million by 2032.

© 2025 Polaris Market Research and Consulting. All rights reserved