Brain Monitoring Market Size, Share, Trends, Industry Analysis Report: By Product (EEG Devices, MEG Devices, TCD Devices, ICP Monitors, Cerebral Oximeters, MRI Devices, CT, Sleep Monitoring Devices, EMG Devices, and Others), Procedure, Disease, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Mar-2025

- Pages: 119

- Format: PDF

- Report ID: PM5431

- Base Year: 2024

- Historical Data: 2020-2023

Brain Monitoring Market Overview

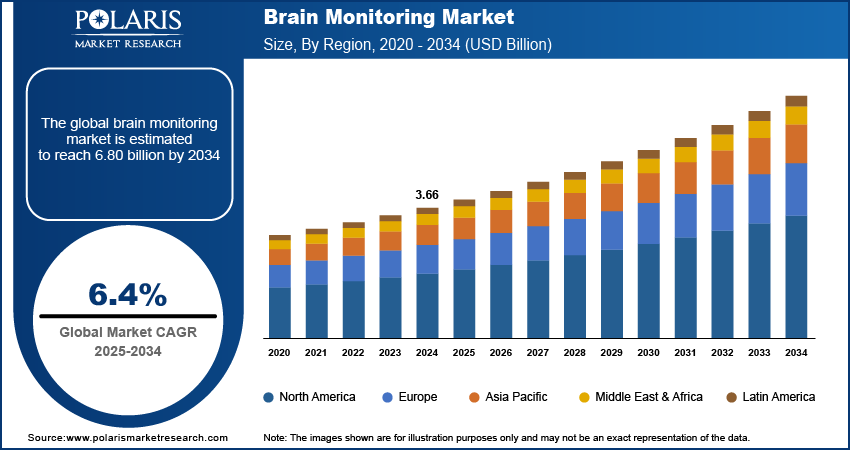

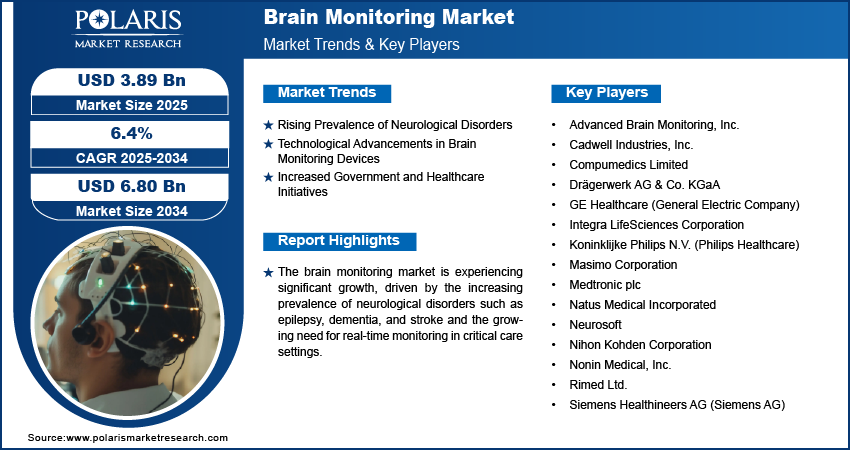

The brain monitoring market size was valued at USD 3.66 billion in 2024. The market is projected to grow from USD 3.89 billion in 2025 to USD 6.80 billion by 2034, exhibiting a CAGR of 6.4% during 2025–2034.

The brain monitoring market encompasses devices and technologies used to assess and track brain activity and neurological function, aiding in the diagnosis and management of conditions such as epilepsy, traumatic brain injuries, sleep disorders, and neurodegenerative diseases. Key drivers for market growth include the increasing prevalence of neurological disorders, rising demand for minimally invasive and noninvasive monitoring techniques, and advancements in wearable and portable brain monitoring devices. Technological developments, such as AI integration and multimodal monitoring systems, along with growing applications in clinical research and neurology, are a few significant brain monitoring market trends. Additionally, government initiatives to improve healthcare infrastructure and increase awareness of brain health support market expansion.

To Understand More About this Research: Request a Free Sample Report

Brain Monitoring Market Dynamics

Rising Prevalence of Neurological Disorders

Neurological conditions such as epilepsy, Parkinson’s disease, Alzheimer’s disease, and strokes are becoming more prevalent due to aging populations and lifestyle changes. According to the World Health Organization (WHO), ∼50 million people globally are affected by epilepsy, making it one of the most common neurological diseases. Additionally, Alzheimer’s Disease International estimates that over 55 million people across the world have dementia, a number expected to rise significantly by 2050. This growing disease burden has created a higher demand for advanced diagnostic and monitoring tools to improve patient outcomes. Therefore, the increasing prevalence of neurological disorders boosts the brain monitoring market demand.

Technological Advancements in Brain Monitoring Devices

Advancements in technology are driving innovation in brain monitoring devices, leading to improved diagnostic accuracy and patient comfort. Noninvasive methods such as electroencephalography (EEG) and functional magnetic resonance imaging (fMRI) have become more precise and efficient due to integration with artificial intelligence and machine learning algorithms. For example, AI-driven EEG systems can detect epileptic seizures with high accuracy, enabling faster treatment decisions. Additionally, wearable and portable devices are gaining traction, allowing continuous monitoring of brain activity in outpatient settings. These developments cater to both clinical and research applications. Hence, rising technological advancements in brain monitoring devices fuel the brain monitoring market development.

Increased Government and Healthcare Initiatives

Government and healthcare organizations are playing a pivotal role in promoting brain health and supporting the adoption of brain monitoring technologies. Initiatives aimed at early detection of neurological conditions and improving access to healthcare have driven the demand for such devices. For instance, the European Commission’s “Horizon Europe” program has prioritized funding for research on neurological disorders, encouraging innovation in diagnostic tools. Similarly, in the US, the National Institutes of Health (NIH) has invested significantly in brain research through its BRAIN Initiative, which aims to enhance understanding of brain function and improve treatments. These government and healthcare initiatives highlight the growing emphasis on brain health, further driving the brain monitoring market growth.

Brain Monitoring Market Segment Insights

Brain Monitoring Market Assessment – Product-Based Insights

By product, the brain monitoring market is segmented into EEG devices, MEG devices, transcranial Doppler (TCD) devices, intracranial pressure (ICP) monitors, cerebral oximeters, MRI devices, CT scanners, sleep monitoring devices, EMG devices, and others. The EEG devices segment holds the largest market share due to their widespread application in diagnosing epilepsy, sleep disorders, and other neurological conditions. The noninvasive nature, cost-effectiveness, and technological advancements such as portable and AI-integrated EEG systems have further driven their adoption in both clinical and homecare settings. The MRI devices segment also contributes significantly to the brain monitoring market share owing to their high-resolution imaging capabilities, which are critical in diagnosing structural abnormalities in the brain.

The sleep monitoring devices segment is expected to register the highest growth rate during the forecast period, driven by the increasing prevalence of sleep disorders such as insomnia and sleep apnea. Growing awareness about the impact of sleep health on overall well-being, coupled with advancements in wearable and wireless monitoring technologies, has fueled demand for these devices. Additionally, cerebral oximeters and TCD devices are gaining attention for their role in assessing cerebral blood flow and oxygenation levels, especially in critical care and surgical settings. The expansion of applications across various neurological and neurovascular conditions continues to drive innovation and growth across multiple product segments.

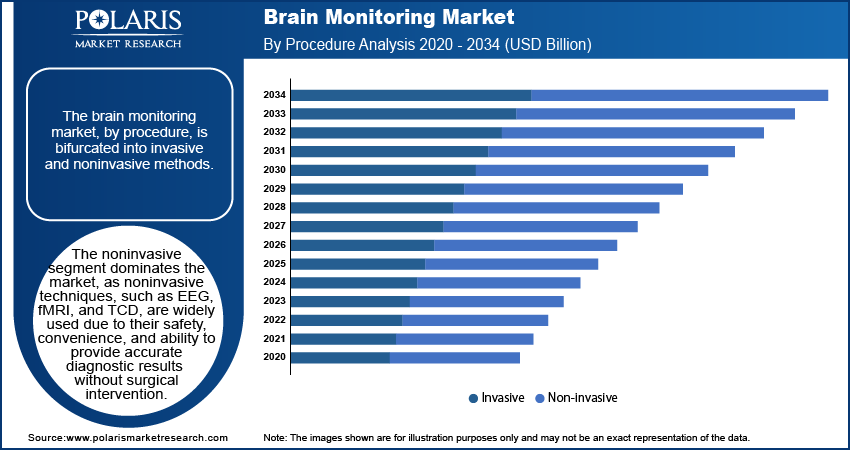

Brain Monitoring Market Outlook – Procedure-Based Insights

The brain monitoring market, by procedure, is bifurcated into invasive and noninvasive methods. The noninvasive segment dominates the brain monitoring market revenue share. Noninvasive techniques, such as electroencephalography (EEG), functional magnetic resonance imaging (fMRI), and transcranial Doppler (TCD), are widely used due to their safety, convenience, and ability to provide accurate diagnostic results without the need for surgical intervention. These procedures are particularly preferred for long-term monitoring and routine diagnosis of conditions such as epilepsy, stroke, and sleep disorders, contributing to their widespread adoption in clinical and outpatient settings. Advancements in portable and wearable noninvasive devices have enhanced their accessibility, broadening their use among patients and healthcare providers.

The invasive segment, while less common, is expected to register significant growth due to its critical role in managing severe neurological conditions. Techniques such as intracranial pressure (ICP) monitoring and deep brain stimulation (DBS) are essential for assessing and treating conditions such as traumatic brain injuries and Parkinson’s disease. The growing number of critical care cases and the increasing adoption of advanced neurosurgical practices are driving demand for these procedures. However, continuous innovation and integration of minimally invasive technologies are bridging the gap between invasive and noninvasive techniques, ensuring their relevance in addressing complex neurological conditions.

Brain Monitoring Market Evaluation – Disease-Based Insights

The brain monitoring market, by disease, is segmented into epilepsy, dementia, headache disorders, stroke, traumatic brain injuries, sleep disorders, and other diseases. The epilepsy segment holds the largest market share. Epilepsy is estimated to affect around 50 million individuals, according to the World Health Organization (WHO). The high prevalence of epilepsy worldwide drives significant demand for diagnostic tools such as electroencephalography (EEG). These devices are critical for detecting and monitoring epileptic seizures, enabling timely and effective treatment. Increasing awareness campaigns and research initiatives focused on epilepsy have boosted the adoption of brain monitoring technologies for this condition.

The sleep disorders segment is expected to register the highest growth rate, driven by the rising prevalence of conditions such as insomnia, sleep apnea, and restless leg syndrome. Growing recognition of the importance of sleep health, coupled with advancements in wearable sleep monitoring devices, has fueled demand in this segment. Sleep monitoring solutions are increasingly being used in clinical settings and homecare environments, making them more accessible to patients. Additionally, traumatic brain injuries and stroke continue to represent critical application areas, with the increasing global burden of these conditions necessitating advanced diagnostic and monitoring solutions to improve patient outcomes.

Brain Monitoring Market Regional Insights

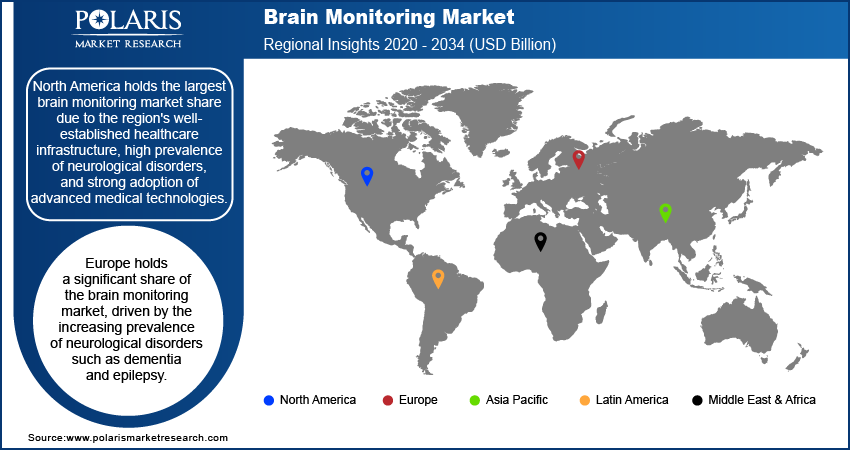

By region, the study provides brain monitoring market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America holds the largest market share. This dominance is attributed to the region's well-established healthcare infrastructure, high prevalence of neurological disorders, and strong adoption of advanced medical technologies. The US, in particular, has a significant demand for brain monitoring devices due to the rising incidence of conditions such as epilepsy, Alzheimer’s disease, and sleep disorders. Additionally, substantial government funding for neurological research, such as the NIH's BRAIN Initiative, and the presence of major market players contribute to the region's leadership.

Europe holds a significant share of the brain monitoring market revenue, driven by the increasing prevalence of neurological disorders such as dementia and epilepsy. The region benefits from robust healthcare infrastructure and government support for research and development in neuroscience. Initiatives such as the European Commission's Horizon Europe program have prioritized funding for innovations in brain monitoring technologies. Countries such as Germany, the UK, and France are leading contributors to the market, supported by advanced medical facilities and a growing focus on early diagnosis and treatment of neurological conditions.

The Asia Pacific brain monitoring market is expected to witness the highest growth rate, primarily due to the increasing prevalence of neurological diseases, rising healthcare expenditures, and improving access to advanced medical technologies. Rapidly growing economies such as China, India, and Japan are driving demand, supported by expanding healthcare infrastructure and government initiatives aimed at improving neurological care. The growing awareness of brain health and the adoption of portable and cost-effective monitoring devices are further fueling Asia Pacific brain monitoring market expansion.

Brain Monitoring Market – Key Players and Competitive Insights

The brain monitoring market features several prominent companies actively contributing to advancements in neurological diagnostics and patient care. Natus Medical Incorporated specializes in neurodiagnostic and neurocritical care products, offering solutions for various neurological disorders. Nihon Kohden Corporation, based in Japan, provides a range of medical electronic equipment, including EEG systems essential for brain monitoring. Philips Healthcare, a division of Koninklijke Philips N.V., delivers comprehensive imaging and monitoring solutions utilized in neurological assessments. GE Healthcare, a subsidiary of General Electric Company, offers advanced imaging technologies and monitoring systems integral to brain health evaluations. Siemens Healthineers AG, part of Siemens AG, provides innovative imaging and diagnostic tools supporting neurological examinations. Medtronic plc develops medical devices, including intracranial pressure monitors and other neuromodulation products. Compumedics Limited, an Australian company, focuses on sleep and neurological diagnostics, supplying EEG and sleep monitoring systems. Drägerwerk AG & Co. KGaA, headquartered in Germany, offers medical devices such as anesthesia machines and patient monitoring systems applicable in neuro-monitoring.

In the competitive landscape, these companies strive to enhance their product offerings through continuous innovation and strategic collaborations. These initiatives reflect a broader industry trend toward integrating advanced technologies such as artificial intelligence and machine learning into brain monitoring devices to enhance diagnostic accuracy and patient care.

The brain monitoring market is witnessing a rise in minimally invasive and noninvasive monitoring solutions, catering to the growing demand for patient-friendly diagnostic tools. Companies are focusing on developing portable and wearable devices that facilitate continuous monitoring, thereby improving patient compliance and expanding the applicability of brain monitoring in various clinical settings. Additionally, strategic acquisitions and partnerships are common as companies aim to broaden their product portfolios and geographic reach, further intensifying competition in the market.

Natus Medical Incorporated is a company that provides medical equipment, software, supplies, and services for diagnosing, monitoring, and treating disorders affecting the brain, neural pathways, and sensory nervous systems. Their products and services are used by healthcare providers worldwide to improve patient outcomes and quality of life.

Nihon Kohden Corporation develops, manufactures, and sells medical equipment, including devices for measuring physiological functions and diagnostic information systems. They aim to improve the quality of life with advanced technology.

List of Key Companies in Brain Monitoring Market

- Advanced Brain Monitoring, Inc.

- Cadwell Industries, Inc.

- Compumedics Limited

- Drägerwerk AG & Co. KGaA

- GE Healthcare (General Electric Company)

- Integra LifeSciences Corporation

- Koninklijke Philips N.V. (Philips Healthcare)

- Masimo Corporation

- Medtronic plc

- Natus Medical Incorporated

- Neurosoft

- Nihon Kohden Corporation

- Nonin Medical, Inc.

- Rimed Ltd.

- Siemens Healthineers AG (Siemens AG)

Brain Monitoring Industry Developments

- In December 2023, Nihon Kohden Corporation introduced the One View feature in its Neuromaster G1 intraoperative neuromonitoring system, integrating comprehensive patient data to improve surgical outcomes.

- In September 2023, Medtronic plc expanded its partnership with Viz.ai to distribute an AI software platform for stroke detection across Europe, the Middle East, and Africa, aiming to synchronize stroke care and reduce treatment times.

Brain Monitoring Market Segmentation

By Product Outlook

- EEG Devices

- MEG Devices

- TCD Devices

- ICP Monitors

- Cerebral Oximeters

- MRI Devices

- CT

- Sleep Monitoring Devices

- EMG Devices

- Others

By Procedure Outlook

- Invasive

- Noninvasive

By Disease Outlook

- Epilepsy

- Dementia

- Headache Disorders

- Stroke

- Traumatic Brain Injuries

- Sleep Disorders

- Other Diseases

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Brain Monitoring Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 3.66 billion |

|

Market Size Value in 2025 |

USD 3.89 billion |

|

Revenue Forecast by 2034 |

USD 6.80 billion |

|

CAGR |

6.4% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy

The brain monitoring market has been segmented into detailed segments of product, procedure, and disease. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy

The brain monitoring market growth and marketing strategy revolves around expanding the adoption of advanced and noninvasive technologies, such as wearable EEG devices and portable brain monitoring systems. Companies are focusing on product innovation, incorporating artificial intelligence, and improving user-friendliness to enhance diagnostic accuracy and patient compliance. Strategic partnerships, acquisitions, and collaborations with research institutions are also key to strengthening market presence and developing innovative solutions. Additionally, increasing awareness about neurological health and investing in emerging markets such as Asia Pacific, where healthcare infrastructure is rapidly improving, are essential elements of the growth strategy for key players.

FAQ's

The brain monitoring market size was valued at USD 3.66 billion in 2024 and is projected to grow to USD 6.80 billion by 2034.

The market is projected to register a CAGR of 6.4% during the forecast period.

North America held the largest share of the market in 2024.

A few key players in the brain monitoring market include Advanced Brain Monitoring, Inc.; Cadwell Industries, Inc.; Compumedics Limited; Drägerwerk AG & Co. KgaA; GE Healthcare (General Electric Company); Integra LifeSciences Corporation; Koninklijke Philips N.V. (Philips Healthcare); Masimo Corporation; Medtronic plc; Natus Medical Incorporated; Neurosoft; Nihon Kohden Corporation; Nonin Medical, Inc.; Rimed Ltd.; and Siemens Healthineers AG (Siemens AG).

The EEG devices segment held the largest market share in 2024 due to their widespread application in diagnosing epilepsy, sleep disorders, and other neurological conditions.

The noninvasive segment dominated the brain monitoring market revenue share in 2024.

Brain monitoring refers to the use of various diagnostic tools and technologies to assess and track brain activity, function, and health. These devices help in detecting neurological disorders, monitoring brain functions in real-time, and supporting the diagnosis and treatment of conditions such as epilepsy, traumatic brain injuries, strokes, and sleep disorders. Brain monitoring methods include noninvasive techniques such as electroencephalography (EEG), functional magnetic resonance imaging (fMRI), and transcranial Doppler (TCD), as well as invasive methods such as intracranial pressure (ICP) monitoring. These technologies are crucial for evaluating brain health and supporting critical care in both clinical and research settings.

A few key trends in the market are described below: Integration of Artificial Intelligence (AI): AI is being increasingly incorporated into brain monitoring devices to improve diagnostic accuracy and automate data analysis. Wearable and Portable Devices: The rise of compact, portable, and wearable devices is enabling continuous and real-time brain monitoring, enhancing patient comfort and compliance. Minimally Invasive Techniques: There is a growing preference for noninvasive and minimally invasive brain monitoring methods, reducing the risks and costs associated with traditional procedures. Increased Focus on Sleep Disorders: With the rising prevalence of sleep disorders, brain monitoring solutions tailored for sleep health are gaining significant market traction

A new company entering the brain monitoring market must focus on developing innovative, noninvasive, and portable devices that cater to the growing demand for remote and continuous monitoring. Leveraging AI and machine learning to enhance diagnostic accuracy and automate data analysis can provide a competitive edge. Additionally, prioritizing affordable solutions and targeting emerging markets with expanding healthcare infrastructure, such as Asia Pacific and Latin America, can offer significant growth opportunities. Collaborating with healthcare providers and research institutions to improve the accessibility and functionality of brain monitoring devices would also be crucial in staying ahead of the competition.

Companies manufacturing, distributing, or purchasing brain monitoring and related products, and other consulting firms must buy the report.

© 2025 Polaris Market Research and Consulting. All rights reserved