Blood Pressure Cuffs Market Size, Share, Trends, Industry Analysis Report: By Type (Automated and Manual), Size, Usage, Age Group, Distribution Channel, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Dec-2024

- Pages: 128

- Format: PDF

- Report ID: PM5260

- Base Year: 2024

- Historical Data: 2020-2023

Blood Pressure Cuffs Market Overview

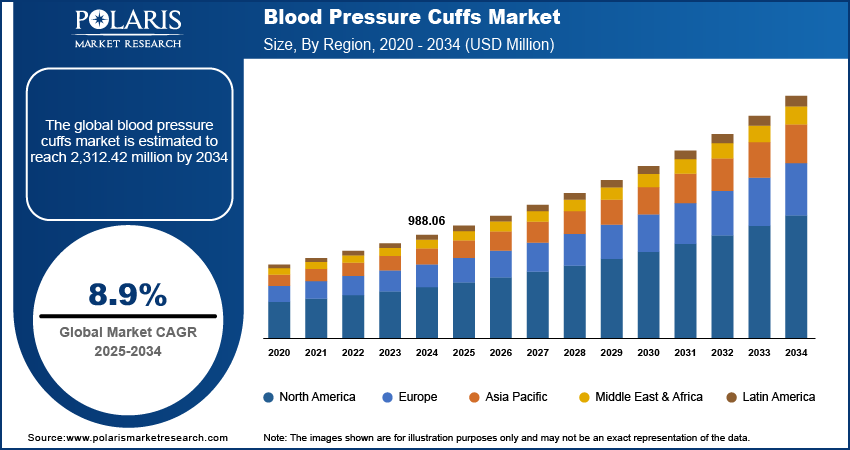

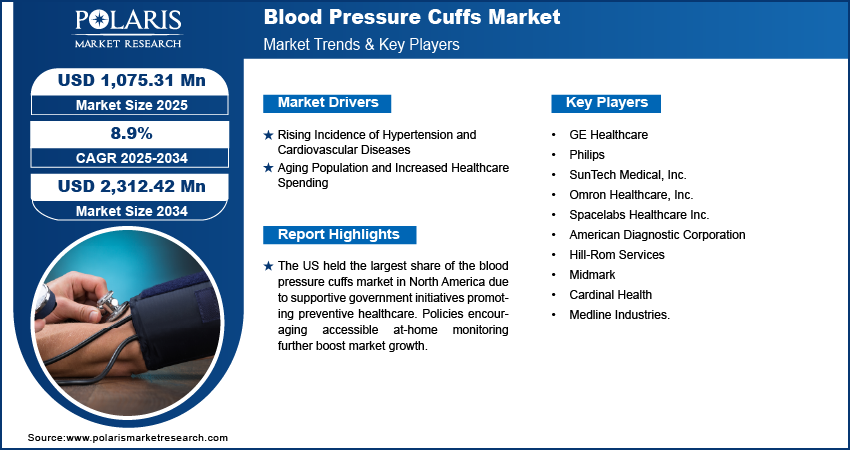

The blood pressure cuffs market size was valued at USD 988.06 million in 2024. The market is projected to grow from USD 1,075.31 million in 2025 to USD 2,312.42 million by 2034, exhibiting a CAGR of 8.9% during the forecast period.

Blood pressure cuffs are medical devices used to measure blood pressure. The rise of telemedicine has boosted demand for home-based diagnostic equipment, including blood pressure cuffs, which is further fueling the blood pressure cuffs market growth. Furthermore, public health campaigns focused on raising awareness about hypertension have contributed to a rise in screenings and monitoring, thereby fueling the market growth.

Individuals are investing in at-home blood pressure monitoring devices for the early detection and management of chronic diseases, which is driving the blood pressure cuffs market expansion. Moreover, innovations in digital and automated blood pressure cuffs have made monitoring easier, more accurate, and accessible for individuals and healthcare providers. The introduction of Bluetooth-enabled devices, wireless monitoring, and integrated smartphone applications has enhanced user experience, attracting a broader range of consumers, which is expected to provide lucrative market opportunities during the forecast period.

To Understand More About this Research: Request a Free Sample Report

Blood Pressure Cuffs Market Driver Analysis

Rising Incidence of Hypertension and Cardiovascular Diseases

Hypertension is one of the most common chronic health conditions worldwide caused by lifestyle factors such as high-stress levels, poor diet, and sedentary habits. According to the WHO, hypertension is a leading cause of early death globally, affecting over a billion people, about 1 in 4 men and 1 in 5 women. As more people are diagnosed with high blood pressure and related cardiovascular conditions, the demand for accurate and accessible blood pressure monitoring devices, including cuffs, has risen significantly.

Aging Population and Increased Healthcare Spending

The aging global population is more susceptible to hypertension and cardiovascular diseases, resulting in a higher demand for regular blood pressure monitoring. For instance, according to the Population Reference Bureau, the US population aged 65 and above is expected to grow from 58 million in 2022 to 82 million by 2050, increasing from 17% to 23% of the total population. Additionally, increased healthcare spending worldwide supports better access to diagnostic devices, including blood pressure cuffs, which is further boosting the blood pressure cuffs market demand.

Blood Pressure Cuffs Market Segment Analysis

Blood Pressure Cuffs Market Assessment by Type

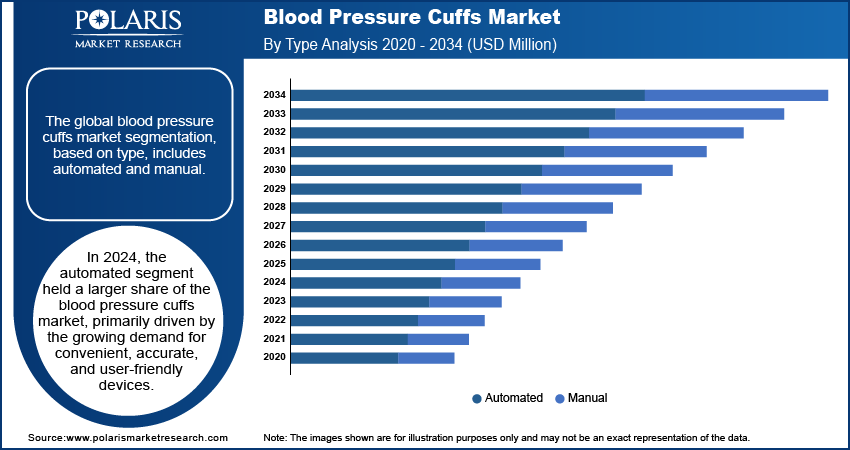

The global blood pressure cuffs market segmentation, based on type, includes automated and manual. In 2024, the automated segment held a larger market share, primarily driven by the growing demand for convenient, accurate, and user-friendly devices. Automated blood pressure cuffs have become increasingly popular in clinical and home settings due to their ease of use, as they require minimal training and offer quick, accurate readings with just the press of a button. Automated cuffs are especially beneficial for elderly patients and those with limited healthcare access, who easily monitor their blood pressure at home. Furthermore, advancements in technology, including Bluetooth connectivity and smartphone integration, have enhanced the appeal of automated devices, allowing users to track their health over time and share data with healthcare providers for improved disease management.

Blood Pressure Cuffs Market Evaluation by End User

The global blood pressure cuffs market, based on end user, is segmented into hospitals, clinics, homecare, and other end users. The homecare segment is expected to register the highest CAGR during the forecast period due to the increasing trend toward self-monitoring and preventive healthcare. Owing to the growing awareness of hypertension and cardiovascular diseases, more individuals are choosing to monitor their blood pressure at home, enabling early detection and better management of health conditions. The convenience and affordability of home-use blood pressure cuffs have made them an appealing choice for patients, particularly among the elderly population and those with chronic conditions requiring regular monitoring. Additionally, advancements in digital health technology, such as mobile apps that track and store blood pressure data, have made home-based monitoring more efficient and accessible.

Blood Pressure Cuffs Market Regional Outlook

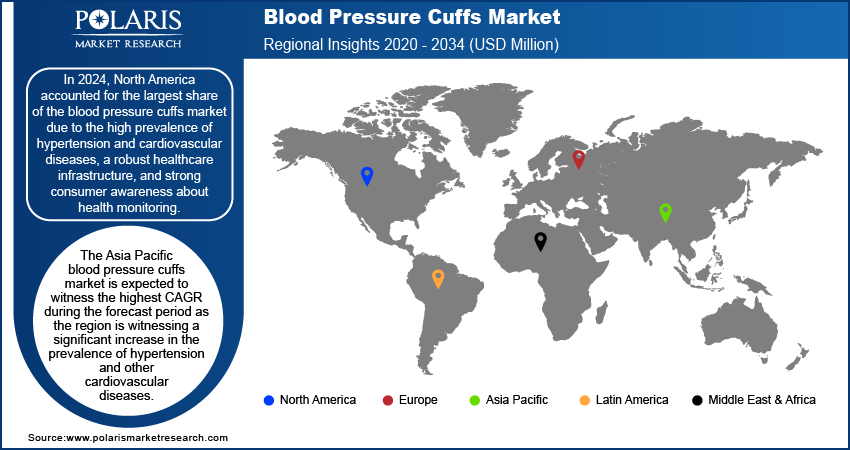

By region, the study provides blood pressure cuffs market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, North America accounted for the largest market share due to the high prevalence of hypertension and cardiovascular diseases, a robust healthcare infrastructure, and strong consumer awareness about health monitoring. North America’s aging population and rising incidence of lifestyle-related health conditions, such as obesity and diabetes, have increased the need for regular blood pressure monitoring in both clinical and homecare settings. According to the American Diabetes Association, in 2021, the prevalence of diabetes in the US was 11.6%, affecting 38.4 million Americans. Among them, 2 million people had type 1 diabetes, with ∼304,000 being children and adolescents. Additionally, the widespread adoption of advanced healthcare technologies, including automated and digital blood pressure cuffs, has further fueled market growth. Favorable healthcare policies and insurance coverage for at-home patient monitoring devices have also made blood pressure cuffs more accessible, solidifying North America’s leading position in the market.

The US accounted for the largest share of the blood pressure cuffs market in 2024. Supportive government initiatives promoting preventive healthcare and policies encouraging accessible at-home monitoring boost the market growth in the US.

The Asia Pacific blood pressure cuffs market is expected to witness the highest CAGR during the forecast period. The region is witnessing a significant increase in the prevalence of hypertension and other cardiovascular diseases, primarily due to rising urbanization, sedentary lifestyles, and unhealthy dietary habits. This surge in health concerns has led to an increased demand for regular monitoring and management of blood pressure, thus boosting the blood pressure cuffs market. Additionally, the growing awareness of preventive healthcare and the emphasis on early diagnosis are driving healthcare providers and patients alike to invest in reliable blood pressure monitoring devices. Government initiatives aimed at improving healthcare infrastructure and access to medical devices also contribute to market expansion. For instance, the India Hypertension Control Initiative, launched in November 2017, aims to reduce hypertension by 25% by 2025. This initiative is supported by India's Ministry of Health and Family Welfare, ICMR, WHO-India, and international partner Resolve to Save Lives.

The China blood pressure cuffs market is expected to see significant growth during the forecast period, driven by technological advancements. The introduction of smart blood pressure cuffs, equipped with digital connectivity and user-friendly features, enhances patient engagement and promotes adherence to treatment protocols. This innovation is propelling market growth as more consumers and healthcare providers recognize the benefits of modern monitoring devices.

Blood Pressure Cuffs Market – Key Players and Competitive Analysis Report

The competitive landscape of the blood pressure cuffs market is characterized by a diverse range of players, including established medical device manufacturers, emerging startups, and technology companies. Major players such as Omron Healthcare, A&D Medical, and Welch Allyn dominate the market, leveraging their strong brand recognition, extensive distribution networks, and commitment to research and development. Major companies continuously innovate and introduce advanced products, such as smart and digital blood pressure cuffs, which enhance user experience and improve accuracy in measurements. Additionally, the market is witnessing an influx of startups focused on developing user-friendly and affordable monitoring solutions, thereby intensifying competition. Strategic partnerships, mergers, and acquisitions are common as companies seek to expand their market presence and product offerings. Regulatory approvals and compliance with international standards also play a crucial role in shaping the competitive dynamics as players strive to gain consumer trust and ensure product quality. A few key market players are GE Healthcare; Philips; SunTech Medical, Inc.; Omron Healthcare, Inc.; Spacelabs Healthcare Inc.; American Diagnostic Corporation; Hill-Rom Services; Midmark; Cardinal Health; and Medline Industries.

GE Healthcare, a subsidiary of GE, was founded in 1994 and headquartered in the US. The company operates in four major segments such as healthcare, aviation, energy, and power. It is one of the major industrial companies. The company offers solutions across more than 170 countries. GE Healthcare has manufacturing and services operations located across 94 countries particularly in the US, and around 190 manufacturing plants are based out in 37 countries. The healthcare segment offers biopharmaceutical manufacturing technologies, patient monitoring and diagnostics, digital solutions, drug discovery, performance enhancement solutions, and medical imaging.

Koninklijke Philips N.V., commonly recognized as Philips, operates in various industries, including healthcare technology, consumer electronics, and lighting. Philips provides medical equipment, software, and services in healthcare, including imaging systems, patient monitoring systems, and clinical informatics solutions. The company provides a range of other medical imaging and diagnostic solutions, including ultrasound systems, MRI scanners, CT scanners, and nuclear medicine systems. It operates in more than 100 countries worldwide.

Key Companies in Blood Pressure Cuffs Market

- GE Healthcare

- Philips

- SunTech Medical, Inc.

- Omron Healthcare, Inc.

- Spacelabs Healthcare Inc.

- American Diagnostic Corporation

- Hill-Rom Services

- Midmark

- Cardinal Health

- Medline Industries.

Blood Pressure Cuffs Market Segmentation

By Type Outlook (Revenue, USD Million; 2020–2034)

- Automated

- Manual

By Size Outlook (Revenue, USD Million; 2020–2034)

- 8–19 cm

- 19 cm and Above

By Usage Outlook (Revenue, USD Million; 2020–2034)

- Reusable

- Disposable

By Age Group Outlook (Revenue, USD Million; 2020–2034)

- Adults

- Infants & Children

By Distribution Channel Outlook (Revenue, USD Million; 2020–2034)

- Offline

- Online

By End User Outlook (Revenue, USD Million; 2020–2034)

- Hospitals

- Clinics

- Homecare

- Other End Users

By Regional Outlook (Revenue, USD Million; 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Blood Pressure Cuffs Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 988.06 million |

|

Market Size Value in 2025 |

USD 1,075.31 million |

|

Revenue Forecast by 2034 |

USD 2,312.42 million |

|

CAGR |

8.9% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD million and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global blood pressure cuffs market value reached USD 988.06 million in 2024 and is projected to grow to USD 2,312.42 million by 2034.

The global market is projected to register a CAGR of 8.9% during the forecast period.

In 2024, North America dominated the blood pressure cuffs market share due to the high prevalence of hypertension and cardiovascular diseases, a robust healthcare infrastructure, and strong consumer awareness about health monitoring.

A few key players in the market are GE Healthcare; Philips; SunTech Medical, Inc.; Omron Healthcare, Inc.; Spacelabs Healthcare Inc.; American Diagnostic Corporation; Hill-Rom Services; Midmark; Cardinal Health; and Medline Industries.

In 2024, the automated segment dominated the market share due to the growing demand for convenient, accurate, and user-friendly devices.

The homecare segment is expected to register the highest CAGR during the forecast period due to the increasing trend toward self-monitoring and preventive healthcare.

© 2025 Polaris Market Research and Consulting. All rights reserved