Benzene Market Size, Share, Trends, Industry Analysis Report: By Production Process (Steam Cracking, Catalytic Reforming, and Others), Derivative, End-Use, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Mar-2025

- Pages: 119

- Format: PDF

- Report ID: PM1495

- Base Year: 2024

- Historical Data: 2020-2023

Benzene Market Overview

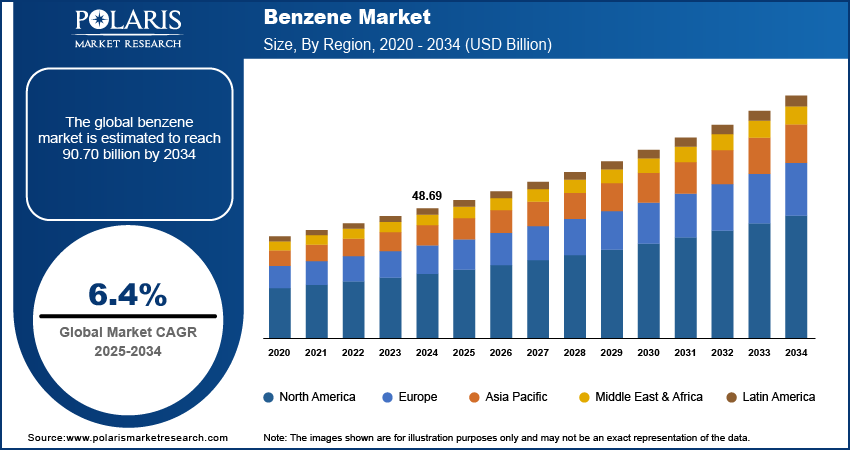

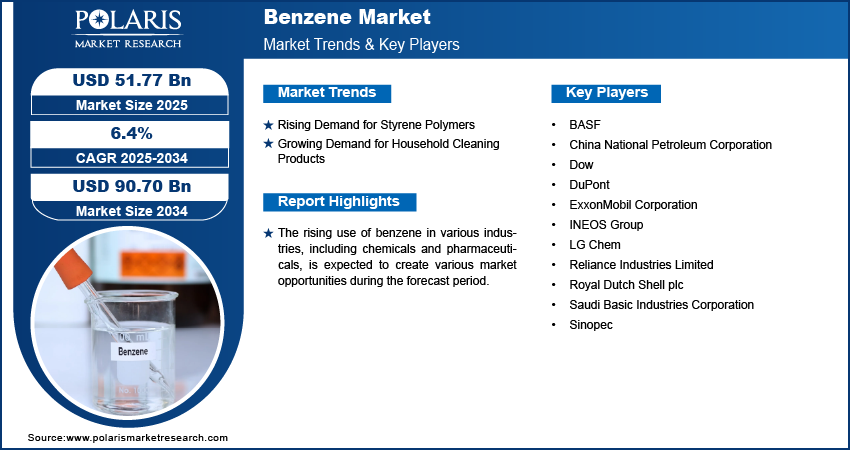

The global benzene market size was valued at USD 48.69 billion in 2024. The market is projected to grow from USD 51.77 billion in 2025 to USD 90.70 billion by 2034, at a CAGR of 6.4% from 2025 to 2034.

Benzene is a colorless or light-yellow colored chemical compound composed of carbon and hydrogen atoms. It is liquid at room temperature, highly flammable, and evaporated quickly in the air. Benzene is used in various industrial and consumer products, including as a solvent in the chemical and pharmaceutical sectors, as well as in gasoline, adhesives, cleaning products, paint thinners, and as a precursor for the production of other chemicals.

Styrene is made from ethylbenzene, a derivative of benzene, and its growing use in industries like packaging, automotive, and electronics is driving up the demand for benzene. The demand for benzene is increasing as the automotive industry expands, especially for electric vehicles; another compound, cumene, which is made from benzene, is also being used across the world in several industries such as chemical, construction, automotive, and aviation industries. Also, the extensive use of benzene in the pharmaceutical industry as a starting material or intermediate in the synthesis of various drugs and as a building block for more complex molecules is driving the market growth.

Benzene is primarily a starting material for producing other chemicals used in various consumer products. The benzene market demand is being driven by the rising need for medications that use intermediates derived from benzene. Additionally, the growing use of polystyrene packaging in culinary and e-commerce applications, an intermediate derived from benzene, is driving market development. Benzene is used to make epoxy resins and phenolic resins, which are used to make durable and safe construction materials, thereby creating several market opportunities.

To Understand More About this Research: Request a Free Sample Report

Benzene Market Dynamics

Rising Demand for Styrene Polymers

Industries such as electronics, packaging, automotive, and construction widely use styrene in its polymerized and co-polymerized forms. Most of the styrene produced globally comes in the form of polystyrene, a polymerized version available in solid, foam, and film forms. The packaging industry uses polystyrene due to its exceptional strength, flexibility, low weight, and resistance to moisture. E-commerce is significantly driving the polystyrene demand by increasing the demand for protective packaging materials, as online retailers rely heavily on polystyrene foam peanuts, trays, and other containers to safely ship fragile items across long distances.

Growing Demand for Household Cleaning Products

Linear alkyl benzene is primarily used as a raw material to produce linear alkyl benzene sulfonate (LAS), a widely used surfactant in both powdered and liquid detergents. With growing public awareness of the benefits of cleanliness, the demand for linear alkyl benzene is expanding into the home cleaning sector. The demand for industrial and residential cleaners is expected to increase, which will expand the benzene market. As LAS is fully biodegradable and environmentally safe, it remains one of the key products in the benzene market. Additionally, the increasing need for both industrial and household cleaners is expected to drive market growth over the forecast period.

Benzene Market Segment Insights

Benzene Market Assessment by Derivative Insights

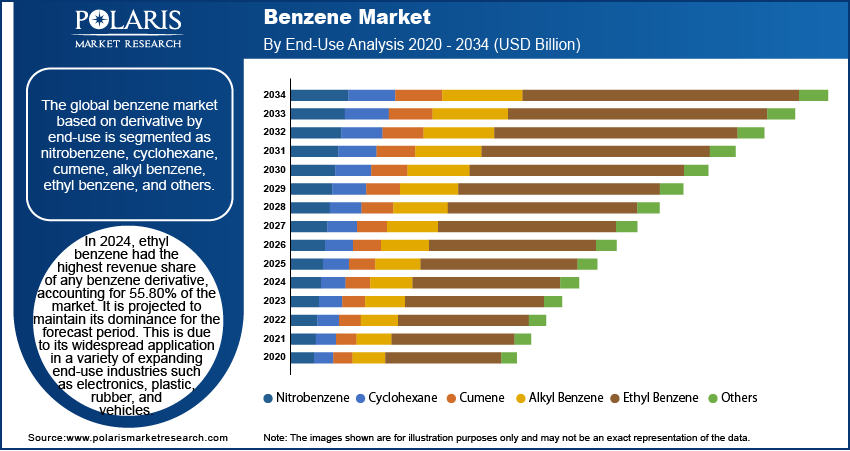

The global market for benzene based on derivative by end-use is segmented as nitrobenzene, cyclohexane, cumene, alkyl benzene, ethyl benzene, and others. The ethyl benzene segment led the market with a 55.80% revenue share in 2024, driven by its expanding applications in end-use industries such as electronics, plastic, rubber, and automobiles. Most of the styrene used in rubber tires, plastic packaging, car components, and electronic devices is derived from ethylbenzene.

The cumene segment accounted for the second-largest revenue share and is projected to witness the fastest growth during the forecast period. This growth is due to its widespread use in end-use industries like paints and coatings, chemicals, automotive, construction, and electronics.

Benzene Market Evaluation by Production Process Insights

The benzene market, based on production process, is segmented into steam cracking, catalytic reforming, and others. The catalytic reforming segment dominated the market with a 52.6% revenue share in 2024. This can be attributed its ability to produce a high yield of aromatic hydrocarbons such as benzene and toluene, making it a key source for the benzene market. Additionally, the process also generates hydrogen as a byproduct, which can be utilized in other refinery operations. All these factors are helping the process to dominate the benezene market developments.

The steam cracking segment accounted for the second-largest revenue share in 2024. This can be attributed to benefits such as flexibility in feedstock options, relatively low capital investment, and high energy efficiency. Additionally, steam cracking can produce valuable byproducts like hydrogen and is able to use renewable feedstocks. It enables a greater variety of products and eliminates the need for the costly distillation process. Due to these factors the process is expected to grow at a significant rate.

Benzene Market Regional Insights

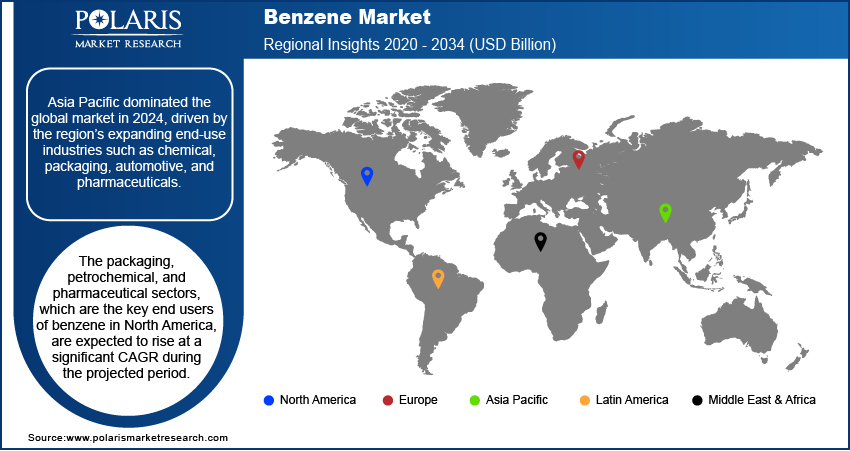

By region, the report provides the benzene market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Asia Pacific led the market with a 48.5% revenue share in 2024, driven by the growing end-use industries such as chemical, packaging, automotive, and pharmaceuticals in the region. South Korea is a major exporter of benzene, while China is one of the largest consumers. The rising demand and imports of benzene in China are due to its growing use in building and automotive products, including paints, flooring, fiberglass, adhesives, and tires.

The benzene market in North America is expected to grow at a significant rate over the forecast period. This can be attributed to the expanding petrochemical sector in the U.S. and North America, along with the accessibility of crude oil, which is influencing the rising demand for benzene in the region. The rising need for styrene in multiple end-use sectors such as packaging, automotive, electronics, and more is also driving the growth of the benzene market in the region.

Benzene Market – Key Players and Competitive Insights

The key players in the market are focusing on research and development to enhance their products and services offerings and drive market demand. Besides, they are adopting various strategic initiatives, including collaborations, mergers and acquisitions, new product launches, and increased investments, to improve their global footprint. To expand and survive in a more competitive environment, market participants must offer innovative solutions.

In recent years, the market for benzene has witnessed several innovations, with key players seeking to provide advanced solutions that help meet sustainability goals. The benzene market research report offers a market assessment of all the key players, including BASF, China National Petroleum Corporation, Sinopec, Dow, Saudi Basic Industries Corporation, ExxonMobil Corporation, DuPont, and Royal Dutch Shell plc.

List of Benzene Market Key Players

- BASF

- Chevron Phillips Chemical Company LLC

- China National Petroleum Corporation

- Dow

- DuPont

- ExxonMobil Corporation

- INEOS Group

- LG Chem

- Reliance Industries Limited

- Royal Dutch Shell plc

- SABIC

- Sinopec

Benzene Industry Developments

- In June 2024, Encina Development Group, LLC, which produces ISCC PLUS-certified circular chemicals, and BASF announced the supply of chemically recycled circular benzene made from post-consumer end-of-life plastics. By incorporating more chemically recycled, circular-based raw materials into its production processes, BASF aims to strengthen its circular economy.

- In March 2023, ExxonMobil Corporation announced the commencement of its long-planned project to expand the processing capacity of light crude oil by 250,000 barrels per day at the integrated refining and petrochemicals complex owned by ExxonMobil Product Solutions Co. in Beaumont, Texas, on the US Gulf Coast

Benzene Market Segmentation

By Derivative Outlook

- Nitrobenzene

- Cyclohexane

- Cumene

- Alkyl Benzene

- Ethyl Benzene

- Others

By End-Use Ourtlok

- Pharmaceuticals

- Agriculture

- Textile

- Automobile

- Paints & Coatings

- Pharmaceutical

- Personal Care

- Others

By Production Process Outlook

- Steam Cracking

- Catalytic Reforming

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Benzene Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 48.69 billion |

|

Market Size Value in 2025 |

USD 51.77 billion |

|

Revenue Forecast by 2034 |

USD 90.70 billion |

|

CAGR |

6.4% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

• The global benzene market was valued at USD 48.69 billion in 2024 and is expected to grow to USD 90.70 billion in 2034.

• The market is projected to register a CAGR of 6.4% from 2025 to 2034.

• Asia Pacific held the largest market share in 2024.

• Sinopec, BASF, China National Petroleum Corporation, Saudi Basic Industries Corporation, Dow DuPont, ExxonMobil Corporation, and Royal Dutch Shell plc. are some of the key players in the market.

• The catalytic reforming segment led the market in 2024.

• The ethyl benzene segment, based on derivative by end-use type, held the largest market share of 55.80% in the benzene market.

© 2025 Polaris Market Research and Consulting. All rights reserved