Automotive V2X Market Share, Size, Trends, Industry Analysis Report, By Offering (Hardware, Software), By Communication; By Connectivity, By Technology, By Vehicle Type, By Unit Type; By Region; Segment Forecast, 2022 - 2030

- Published Date:Jul-2022

- Pages: 119

- Format: PDF

- Report ID: PM1428

- Base Year: 2021

- Historical Data: 2018 - 2020

Report Outlook

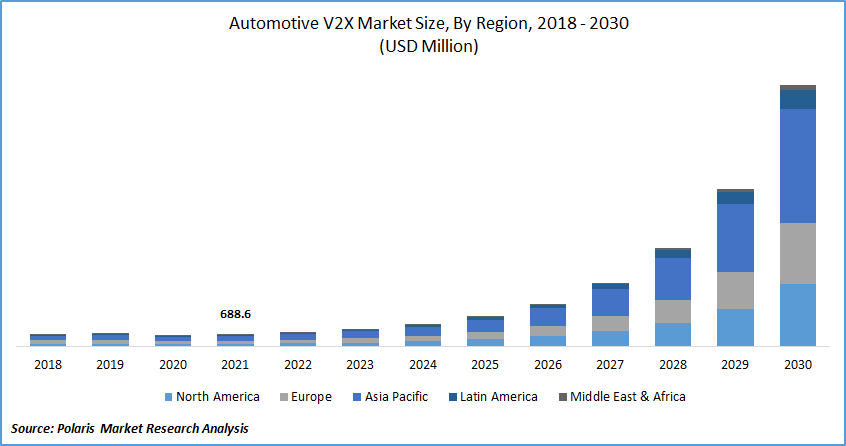

The global automotive V2X market was valued at USD 688.6 million in 2021 and is expected to grow at a CAGR of 44.3% during the forecast period. The major driving factors of the automotive V2X market include the growing automotive industry and increasing demand for high-end luxury vehicles. The increasing demand for real-time traffic alerts and the need for improved road safety supports the automotive V2X market growth.

Know more about this report: Request for sample pages

The introduction of government regulations for road & vehicular safety and improved traffic management also boosts the automotive V2X industry growth. The growing demand for autonomous and self-driving vehicles encourages manufacturers to integrate advanced V2X systems in vehicles. The rising environmental concerns, growing adoption of connected vehicles, and increasing demand for technologically advanced vehicles from countries such as China, the U.S, and Western Europe also increase the demand for automotive V2X systems.

The covid-19 pandemic has had a positive impact on the automotive V2X market. This escalation is because of the requirement for autonomous vehicles to deliver supplies. The enhanced safety of autonomous vehicles inflated demand for this technology and flourished the market growth. The investments in the technologies related to future mobility made during this pandemic have reinforced the automotive V2X growth. The automotive V2X industry is expected to observe exponential growth shortly.

Know more about this report: Request for sample pages

Industry Dynamics

Growth Drivers

As per the WHO report on road safety, incidents related to vehicular traffic result in more than 1.3 million causalities each year. Per the research executed by the US Department of Transportation (DOT), road accidents can be minimized by 80% with the assistance of vehicles to everything. It could assist lessen road traffic by determining and notifying the driver of objects that are invisible.

For instance, an automotive V2X application such as Emergency Brake Light could alarm the driver of the following vehicle in advance if it discovers an unforeseen announcement by leading the car in a blind turn, thereby circumventing an accident. According to the approximation by the US DOT, vehicles for everything would save more than 1000 lives per year and minimize 2.3 million nonfatal injuries. Thus, these factors will be responsible for the growth of the automotive V2X.

In Europe, congested roads could cost around USD 109 billion annually. Economic savings possible with more efficient and safer transportation systems are massive. As per the US DOT yearly round, about USD 871 billion can be saved in the US with the assistance of automotive V2X. Blocked roads cause supply chain delays.

Also, there is growing complexity, cost of doing a business, and lesser productivity. With this technology, factors that cause congestion can be discovered early, and the vehicles can react correspondingly. Integrating simulation models with data that is real-time and optimized routes can be recognized to increase the efficacy and speed of rides. These factors are credited with enhancing the demand for vehicles in the market.

Report Segmentation

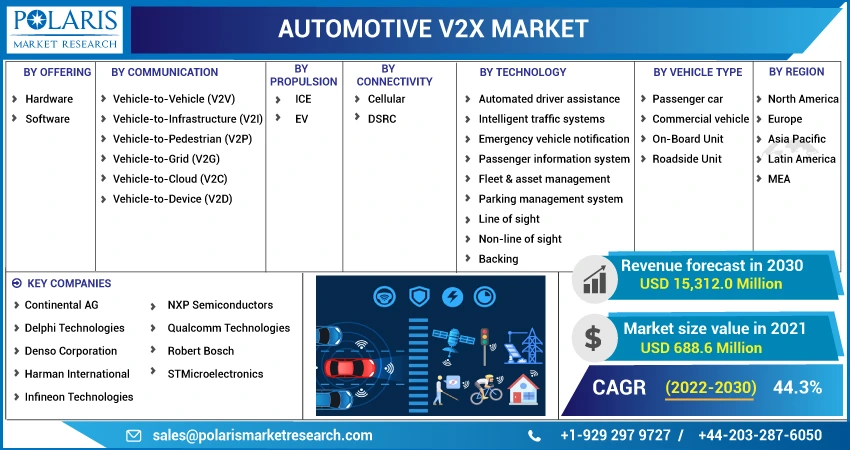

The market is primarily segmented on the basis of offering, communication, propulsion, connectivity, technology, vehicle type, unit type, and region.

|

By Offering |

By Communication |

By Propulsion |

By Connectivity |

By Technology |

By Vehicle Type |

By Unit Type |

By Region |

|

|

|

|

|

|

|

|

Know more about this report: Request for sample pages

Insight by Connectivity

By connectivity, the DSRC segment held the largest market share because of the moderation of implementation, fully designed technology, and verified data security standards. The cellular segment is anticipated to portray a higher CAGR in the automotive V2X market during the forecast period.

Cellular vehicle to everything is an inexpensive and multi-skilled solution that can offer stable short-range and long-range connectivity spanning an extensive area. It provides enhanced safety features and pronounced capacity and lessens the prospect of service disturbances. These factors will fuel the growth of this segment.

Insight by Communication

By communication type, the V2V segment held the largest share of the market. V2V can offer drivers alternative vehicle information, including direction, location, and speed, and apprise them of any probable dangers in frameworks such as heavy traffic, blind spots, intersection, and terrain issues, among other situations. This factor will propel the growth of the segment.

The V2I segment also portrays considerable growth over the forecast period. V2I can assist in developing driver assistant systems such as intelligent parking and autonomous driving that can improvise the future of traffic lanes and parking lots that handle exceptional traffic flow. This factor will drive the implementation of V2X technology.

Geographic Overview

Geographically, Asia Pacific held the largest market share as telecommunication technology providers and automotive OEMs are the leading players deciding vehicles for development in this region. Japan and China are anticipated to lead the Asia Pacific regarding technology development.

Likewise, Europe is expected to portray substantial growth in the market. This region observed several research initiatives, industrial associations, and collective testing for vehicle-to-everything communication. For instance, the CAR 2 CAR consortium, including multiple technology developers and automakers, concentrates on advancing intelligent transport systems and applying them on European roads.

Competitive Insight

Some of the major players operating in the global market include Continental AG, Delphi Technologies, Denso Corporation, Harman International, Infineon Technologies, NXP Semiconductors, Qualcomm Technologies, Robert Bosch, and STMicroelectronics.

Automotive V2X Market Report Scope

|

Report Attributes |

Details |

|

The market size value in 2021 |

USD 688.6 Million |

|

The revenue forecast in 2030 |

USD 15,312.0 Million |

|

CAGR |

44.3% from 2022 - 2030 |

|

Base year |

2021 |

|

Historical data |

2018 - 2020 |

|

Forecast period |

2022 - 2030 |

|

Quantitative units |

Revenue in USD Million and CAGR from 2022 to 2030 |

|

Segments covered |

By Offering, By Communication, By Propulsion, By Connectivity, By Technology, By Vehicle Type, By Unit Type; By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

|

Key companies |

Continental AG, Delphi Technologies, Denso Corporation, Harman International, Infineon Technologies, NXP Semiconductors, Qualcomm Technologies, Robert Bosch, STMicroelectronics. |

© 2025 Polaris Market Research and Consulting. All rights reserved