Automotive Lead-Acid Battery Market Size, Share, Trends, Industry Analysis Report: By Type (Flooded Batteries and VRLA Batteries), Product, Vehicle Type, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Apr-2025

- Pages: 129

- Format: PDF

- Report ID: PM5463

- Base Year: 2024

- Historical Data: 2020-2023

Automotive Lead-Acid Battery Market Overview

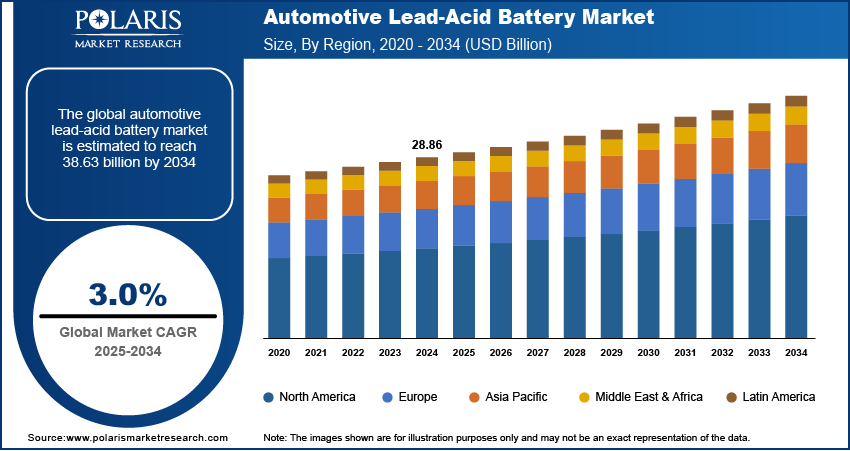

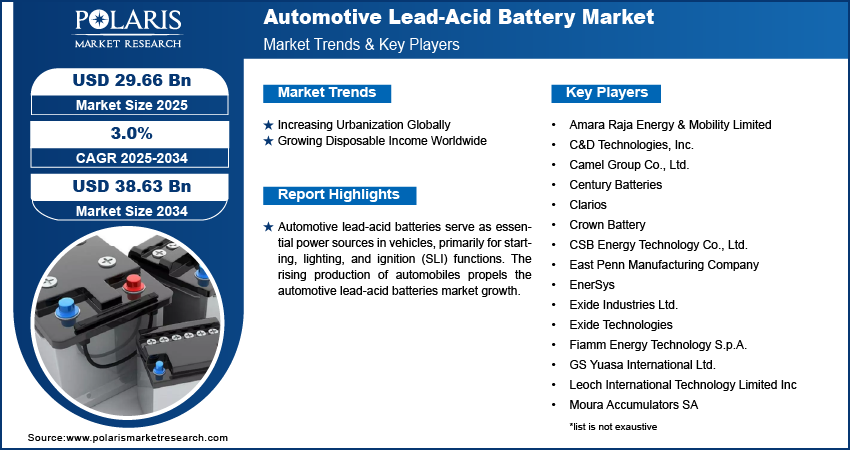

The global automotive lead-acid battery market size was valued at USD 28.86 billion in 2024. The market is projected to grow from USD 29.66 billion in 2025 to USD 38.63 billion by 2034, exhibiting a CAGR of 3.0 % during 2025–2034.

Automotive lead-acid batteries serve as essential power sources in vehicles, primarily for starting, lighting, and ignition (SLI) functions. These batteries consist of lead dioxide (PbO₂) at the positive plate and spongy lead (Pb) at the negative plate, immersed in a sulfuric acid electrolyte. The design of automotive lead-acid batteries allows for high surge currents, making them particularly effective for starting engines that require significant power at ignition.

The rising production of automobiles is propelling the automotive lead-acid batteries market growth. As per the report published by the European Automobile Manufacturers' Association in 2022, 85.4 million motor vehicles were produced around the world, an increase of 5.7% compared to 2021. Automakers order more lead-acid batteries to keep up with the rising production of automobiles, as these batteries are utilized in vehicles to power SLI functions. The expansion of commercial vehicle fleets, including trucks and buses, further amplifies this demand, as these vehicles rely on powerful batteries, including lead-acid, for consistent performance. The increasing popularity of start-stop technology in luxury and electric vehicles (EVs) also drives higher adoption of advanced lead-acid batteries, such as enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries.

To Understand More About this Research: Request a Free Sample Report

The automotive lead-acid battery market demand is driven by the rising advancement in technology. Automakers are integrating modern features such as regenerative braking and advanced infotainment systems into their vehicles, which require reliable and efficient power sources. Battery manufacturers are developing enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries to meet these evolving energy demands, making lead-acid batteries more suitable for modern vehicles. Innovations in battery design also improve charge acceptance, extend lifespan, and reduce maintenance, making them a more attractive option for both automakers and consumers. Recycling technologies have also advanced, making lead-acid batteries more sustainable and cost-effective, which further encourages their adoption.

Automotive Lead-Acid Battery Market Dynamics

Increasing Urbanization Globally

Various regions across the world are witnessing rising urbanization. As per the data published by the World Bank, 56% of the world's population lives in cities, and is expected to double by 2050. Urbanization leads to a surge in automobile sales as people in urban areas rely on personal and public vehicles for daily commuting. This increases the need for reliable automotive batteries, such as lead-acid batteries, as these batteries provide essential power to operate various functions in vehicles, such as lighting, starting, and ignition. Traffic congestion and frequent stop-and-go driving in urban areas create greater demand for advanced lead-acid batteries, such as enhanced flooded batteries (EFB) and absorbent glass mat (AGM) batteries, which support start-stop vehicle systems. The rapid development of smart cities and infrastructure projects encourages more vehicle production and electrification, contributing to the demand for automotive lead-acid batteries. Therefore, rising urbanization across the globe boosts the automotive lead-acid battery market development.

Growing Disposable Income Worldwide

Increased disposable income drives people to prioritize vehicle ownership for convenience, status, and mobility, which leads to high adoption of lead-acid batteries as these batteries are deployed in vehicles. Increased spending power also encourages consumers to upgrade to newer models, which require reliable lead-acid batteries for ignition, lighting, and electronic systems. Additionally, higher disposable income allows vehicle owners to invest in battery replacements, choosing advanced lead-acid technologies such as absorbent glass mat (AGM) and enhanced flooded batteries (EFB) for better performance. As income levels rise, the overall demand for automobiles and the batteries that power them continues to grow. Hence, the rising disposable income of consumers propels the automotive lead-acid battery market growth.

Automotive Lead-Acid Battery Market Segmental Insights

Automotive Lead-Acid Battery Market Evaluation by Type

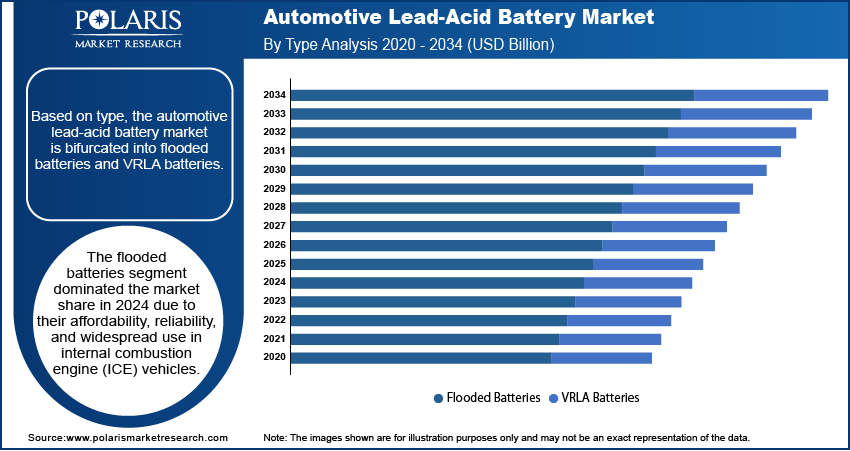

Based on type, the automotive lead-acid battery market is divided into flooded batteries and VRLA batteries. The flooded batteries segment dominated the automotive lead-acid battery market share in 2024 due to their affordability, reliability, and widespread use in internal combustion engine (ICE) vehicles. Flooded batteries are preferred for passenger cars, commercial vehicles, and two-wheelers as they offer a cost-effective solution for starting, lighting, and ignition (SLI) applications. The well-established manufacturing and recycling infrastructure for flooded batteries further contributed to their dominance, ensuring a steady supply and lower production costs. The ability of flooded batteries to withstand overcharging and deep cycling made them a preferred choice for conventional vehicles, especially in regions with high vehicle ownership, such as Asia Pacific and North America.

Automotive Lead-Acid Battery Market Outlook by End User

In terms of end user, the automotive lead-acid battery market is segregated into OEM and aftermarket. The aftermarket segment is expected to grow at a rapid pace during the forecast period owing to the high replacement rate of batteries in vehicles. Frequent battery wear and tear, exposure to extreme temperatures, and repeated charge-discharge cycles contributed to a steady demand for replacements. Vehicle owners and fleet operators replace old batteries periodically to ensure optimal performance, driving consistent demand in the segment. The increasing number of aging vehicles on the road also played a crucial role in the expansion of the aftermarket segment, as older vehicles required more frequent battery replacements. Additionally, the well-established distribution network of retailers, service centers, and e-commerce platforms made replacement purchases more accessible to aftermarket consumers, thereby propelling segment growth.

Automotive Lead-Acid Battery Market Regional Analysis

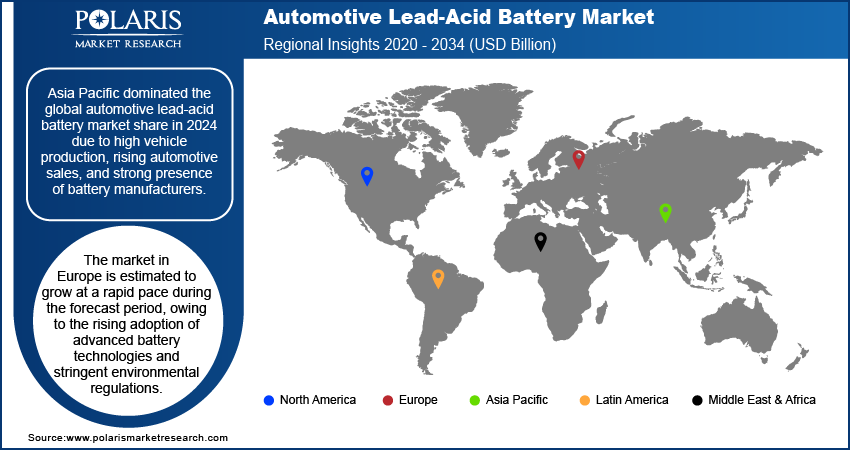

By region, the report provides automotive lead-acid battery market insight into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific dominated the global automotive lead-acid battery market revenue share in 2024 due to high vehicle production, rising automotive sales, and strong presence of battery manufacturers. Countries such as China, India, and Japan contributed significantly to the dominance of the region, with China leading as the largest producer and consumer of automobiles. Rapid urbanization, increasing disposable income, and expanding transportation infrastructure fueled vehicle demand, directly driving lead-acid battery sales. The well-established automotive supply chain in China, supported by government initiatives and large-scale battery recycling facilities, ensured a supply of cost-effective and sustainable lead-acid batteries. The growing demand for two-wheelers and commercial vehicles in India further boosted the automotive lead-acid battery market expansion in the country. Additionally, favorable policies promoting local manufacturing and foreign investments in the automotive sector contributed to the market growth in the region.

The Europe automotive lead-acid battery market is estimated to grow at a rapid pace during the forecast period, owing to the rising adoption of advanced battery technologies and stringent environmental regulations. Countries such as Germany, France, and the UK are dominating this shift by focusing on fuel-efficient vehicles equipped with start-stop technology and hybrid systems. Germany, with its strong automotive industry and presence of major vehicle manufacturers, is expected to dominate the region. Automakers in Europe are increasingly integrating absorbent glass mat (AGM) and enhanced flooded batteries (EFB) to comply with strict emission standards and improve fuel efficiency. The push for sustainability and the well-developed recycling infrastructure in the region are further driving demand for lead-acid batteries. Additionally, the growing popularity of hybrid and electric vehicles, which require auxiliary lead-acid batteries for onboard electronics and safety systems, is contributing to the rising demand for lead-acid batteries in the region.

Automotive Lead-Acid Battery Market – Key Players & Competitive Analysis Report

Prominent market players are investing heavily in research and development to expand their offerings, which will propel the automotive lead-acid battery market growth during the forecast period. These market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments such as innovative launches, international collaborations, higher investments, and mergers and acquisitions between organizations.

The automotive lead-acid battery market is fragmented, with the presence of numerous global and regional market players. A few major players in the market include Amara Raja Energy & Mobility Limited; C&D Technologies, Inc.; Camel Group Co., Ltd.; Century Batteries; Clarios; Crown Battery; CSB Energy Technology Co., Ltd.; East Penn Manufacturing Company; EnerSys; Exide Technologies; Fiamm Energy Technology S.p.A.; GS Yuasa International Ltd.; Leoch International Technology Limited Inc; Moura Accumulators SA; Reem Batteries; Robert Bosch LLC; Stryten Energy; The Furukawa Battery Co., Ltd.; and Tianneng Rechargeable Battery Manufacturers.

Amara Raja Energy & Mobility Limited, formerly known as Amara Raja Batteries Limited, is an Indian multinational conglomerate headquartered in Tirupati.

Amara Raja Energy & Mobility Limited was the first company to manufacture Valve Regulated Lead-Acid (VRLA) batteries in India and is the largest manufacturer of VRLA batteries. The company supplies automotive batteries to several original equipment manufacturers (OEMs), including Maruti Suzuki, Hyundai Motors, Ford India, Tata Motors, Mahindra & Mahindra, Honda Cars India, Renault Nissan, Honda Motorcycles & Scooters India, Royal Enfield, and Bajaj Auto.

Exide Technologies is a global provider of stored energy solutions, manufacturing and distributing batteries and related equipment. Founded in 1888 as the Electric Storage Battery Company, the company develops its offerings through various battery technologies, including absorbent glass mats, enhanced cycling mats, gel, flooded, and VRLA (Valve Regulated Lead-Acid) batteries. Exide Technologies serves both OEMs and the aftermarket in the automotive sector. Their automotive batteries are used for SLI applications across two-wheelers, three-wheelers, and four-wheelers, including cars, jeeps, buses, and trucks. The company has manufacturing facilities in North America, Europe, and South Asia.

List of Key Companies in Automotive Lead-Acid Battery Market

- Amara Raja Energy & Mobility Limited

- C&D Technologies, Inc.

- Camel Group Co., Ltd.

- Century Batteries

- Clarios

- Crown Battery

- CSB Energy Technology Co., Ltd.

- East Penn Manufacturing Company

- EnerSys

- Exide Technologies

- Fiamm Energy Technology S.p.A.

- GS Yuasa International Ltd.

- Leoch International Technology Limited, Inc

- Moura Accumulators SA

- Reem Batteries

- Robert Bosch LLC

- Stryten Energy

- The Furukawa Battery Co., Ltd.

- Tianneng Rechargeable Battery Manufacturers

Automotive Lead-Acid Battery Industry Developments

July 2024: Exide, a company that manufactures batteries and accessories for a variety of applications, including automotive, power, telecommunications, and others, introduced lead-acid battery based on advanced Absorbent Glass Mat (AGM) technology for starting, light, and ignition (SLI) applications.

April 2024: GS Yuasa Corporation, a Japan-based company that manufactures and sells batteries, power systems, and other electrical equipment, announced the sales launch for the ECO.R HV auxiliary VRLA battery series for Toyota hybrid vehicles.

Automotive Lead-Acid Battery Market Segmentation

By Type Outlook (Revenue, USD Billion, 2020–2034)

- Flooded Batteries

- VRLA Batteries

By Product Outlook (Revenue, USD Billion, 2020–2034)

- SLI Batteries

- Micro Hybrid Batteries

- Auxiliary Batteries

By Vehicle Type Outlook (Revenue, USD Billion, 2020–2034)

- Passenger Cars

- Light and Heavy Commercial Vehicles

By End User Outlook (Revenue, USD Billion, 2020–2034)

- OEM

- Aftermarket

By Regional Outlook (Revenue, USD Billion, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Automotive Lead-Acid Battery Market Report Scope

|

Report Attributes |

Details |

|

Market Size Value in 2024 |

USD 28.86 Billion |

|

Revenue Forecast in 2025 |

USD 29.66 Billion |

|

Revenue Forecast by 2034 |

USD 38.63 Billion |

|

CAGR |

3.0% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global automotive lead-acid battery market size was valued at USD 28.86 billion in 2024 and is projected to grow to USD 38.63 billion by 2034.

The global market is projected to register a CAGR of 3.0% during the forecast period.

Asia Pacific held the largest share of the global market in 2024.

A few of the key players in the market are Amara Raja Energy & Mobility Limited; C&D Technologies, Inc.; Camel Group Co., Ltd.; Century Batteries; Clarios; Crown Battery; CSB Energy Technology Co., Ltd.; East Penn Manufacturing Company; EnerSys; Exide Industries Ltd.; Exide Technologies; Fiamm Energy Technology S.p.A.; GS Yuasa International Ltd.; Leoch International Technology Limited Inc; Moura Accumulators SA; Reem Batteries; Robert Bosch LLC; Stryten Energy; The Furukawa Battery Co., Ltd.; and Tianneng Rechargeable Battery Manufacturers.

The flooded batteries segment dominated the automotive lead-acid battery market revenue share in 2024.

© 2025 Polaris Market Research and Consulting. All rights reserved