Aerospace Robotics Market Share, Size, Trends, Industry Analysis Report, 2026- 2034

REPORT DETAILS

Aerospace Robotics Market Summary

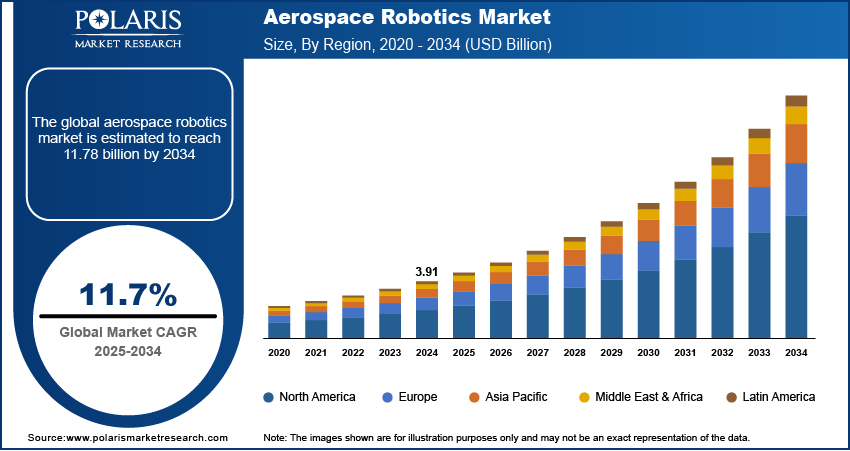

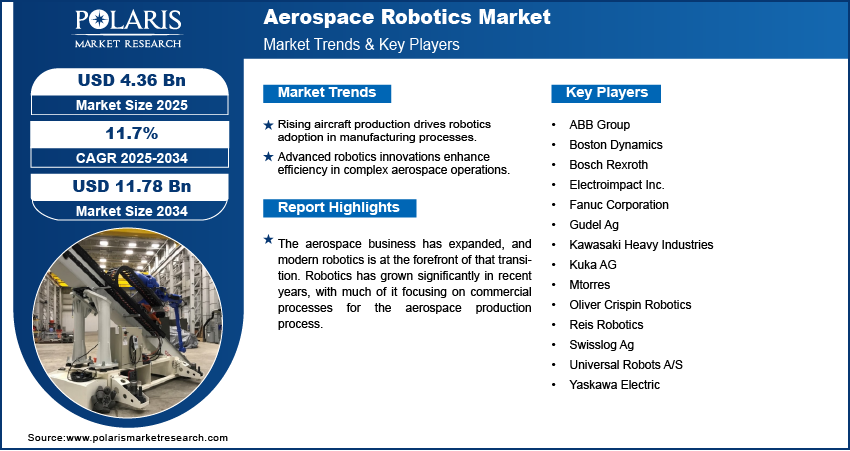

The global aerospace robotics market was valued at USD 4.36 billion in 2025 and is expected to grow at a CAGR of 11.7% during the forecast period. Key factors driving demand includes shortage of skilled labor, capital intensive technology, and increased demand for automation for efficient aircraft manufacturing.

Market Statistics

Key Takeaways

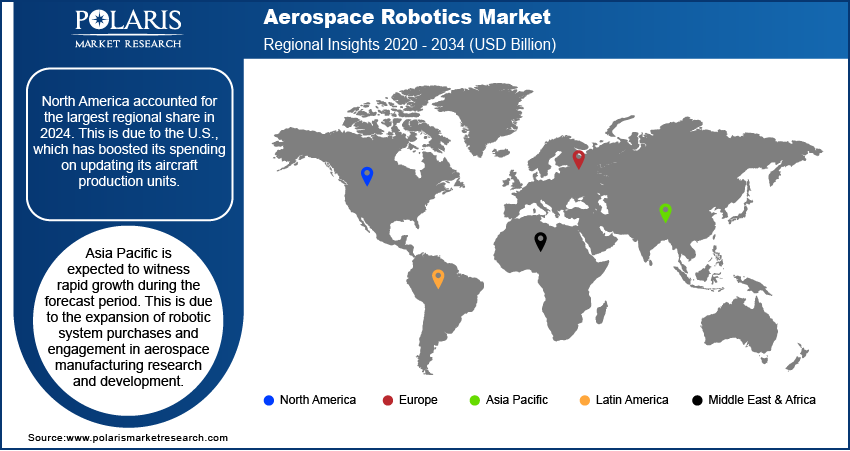

- North America accounted for the largest regional share of 36.0% in 2025. This is due to the U.S., which has boosted its spending on updating its aircraft production units.

- Asia Pacific is expected to witness rapid growth at a CAGR of 14.0% during the forecast period. This is due to the expansion of robotic system purchases and engagement in aerospace manufacturing research and development.

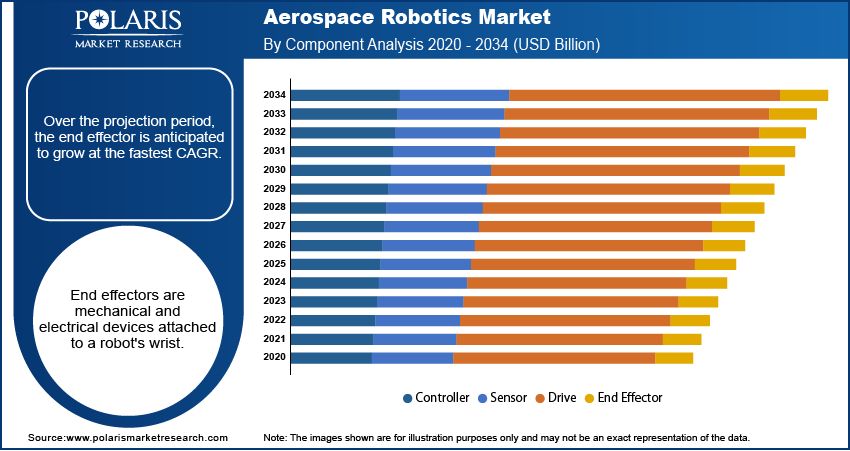

- The end effector is expected to witness rapid growth at a CAGR of 12.9% during the forecast period. This is due to the mechanical and electrical devices attached to a robot's wrist.

- The traditional robot segment dominated the market with 72.0% in 2025. This is due to the increased use of traditional robots in applications such as fastening, welding, drilling, and painting.

- Drilling & Fastening dominated the aerospace robotics market with 25.0% share in 2025 due to its critical role in high-precision aircraft assembly.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising aircraft production rates to accommodate the demand will improve efficiency, accuracy, and scalability in the manufacturing process and facilitates the adoption of robotics directly.

- Innovation continues to focus on increasing the sophistication and agility of robots performing complex aerospace processes, increasing use and supporting commercial development.

- High up-front costs and complexity of integration for robotics systems, particularly for small-manufacturers creates a barrier to adoption.

- The rise in development of collaborative robots (cobots) and AI also enable new possibilities for automating complex assembly and processes.

AI Impact on Aerospace Robotics Market

- Robots equipped with AI-based vision systems demonstrate micro-assembly and inspection functionality with greater accuracy than humans, particularly with very complex components for aircraft, and increased defect rates.

- AI algorithms and visual sensors are expected to be used to review robot sensor data to analyze probable failures prior to their occurrence to reduce unplanned downtime and maintain production standards on critical assembly lines.

- AI provides analytical systems that allow the robot to change its behaviors in real-time workflows to accept variability in parts or jobs, thus increasing interoperability on the production floor.

- AI is expected to schedule and coordinate multiple robots effectively for scheduled workflow, and workflow improvements for efficiency in large-volume aerospace manufacturing.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

What is Aerospace Robotics?

Aerospace robotics refers to the application of robotic systems, automation technologies, and intelligent machines. Robotics systems are used across aircraft manufacturing, spacecraft operations, inspection, maintenance, assembly, painting, welding, and defense activities. Advanced robotic solutions are used to enhance precision, productivity, safety, and operational efficiency. They also help reduce labor costs, avoid human errors, and support high-performance manufacturing and operational processes.

The aerospace business has expanded, and modern robotics is at the forefront of that transition. Robotics has grown significantly in recent years, with much of it focusing on commercial processes for the aerospace production process.

The increased demand for automation for efficient aircraft manufacture has driven the market growth. Furthermore, rising labor costs around the world contribute to market expansion. However, the shortage of experienced professionals and the high cost of robotic device installation are restraining the market's growth.

On the contrary, an increase in IoT (Internet of Things) trends in aircraft manufacturing firms and rapid growth in the global aerospace industry create a lucrative growth opportunity for the market. The COVID-19 pandemic has altered the market's dynamics for the following years, as demand for new aircraft has decreased since the coronavirus outbreak.

Aircraft OEMs focus on variables such as nations' governments planning to revamp supply chain management while considering the epidemic to combat the pandemic. To minimize the consequences of the pandemic on commercial aviation, aircraft manufacturers are looking forward to optimizing their overall operations and focusing on inventory management.

Machine operators must adhere to social distancing and other safety standards when working in the industrial industry. This has also shifted the market for aerospace robotics in a positive direction, as the companies' key concern is worker safety. As a result, demand for the employment of robots in the production process will rise, as robots are the ideal substitutes for shop floor workers.

Difference Between Aerospace Robotics vs Traditional Manufacturing

| Parameter | Aerospace Robotics | Traditional Manufacturing |

| Precision | Delivers highly accurate and repeatable operations with minimal errors | More dependent on manual skills, increasing chances of inconsistencies |

| Labor Dependency | Reduces reliance on manual labor through automation | Requires a larger workforce for assembly, inspection, and production |

| Safety | Enhances worker safety by handling hazardous and complex tasks | Higher exposure of workers to risky environments and repetitive tasks |

| Operational Efficiency | Improves workflow optimization, automation, and resource utilization | Slower processes with higher downtime and manual intervention |

| Production Speed | Enables faster production cycles with continuous operations | Production speed is comparatively lower due to manual processes |

| Quality Consistency | Maintains uniform product quality through automated control systems | Quality may vary depending on workforce expertise and process control |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Industry Dynamics

Increasing Automation in Aircraft Manufacturing

The demand for aerospace robotics is driven by growing automation in aircraft manufacturing. Manufacturers aim for higher accuracy, uniformity and productivity in the multilevel build-up processing. This is due to the extremely tight tolerances for aerospace parts which are perfect for works such as drilling, fastening, welding, painting, inspecting and handling composites with high precision. Robots provide unparalleled predictability and reproducibility, producing identical outputs for each and every task. This effect has a positive impact on the product and process quality, on the machine tool repair rate, and on the general plant safety. For instance, in March 2026, Aerobotix received USD 1.2 million U.S. Air Force SBIR contract to develop a robotic scuff sanding system for F-35s out of Hill Air Force Base. The automation solves skilled labor issues and safety hazards, and it increases uniformity, resulting in a 50% reduction in sanding time. Their utilization also enables faster production runs and more cost-effective use of the tools of production. In addition, automation enables aerospace firms to mitigate skilled labor shortages by mechanizing certain physically exhausting, repetitive tasks. Therefore, as the development of aircraft configuration and manufacturing process is progressive, the requirement of robot solutions with flexibility and accuracy is also increasing.

Rising Aircraft Production and Maintenance Demand

The need for faster and safer manufacturing/servicing operations is growing with increasing aircraft production and demand for maintenance, which is fueling the sales of aerospace robots. According to the International Air Transport Association report, in 2025, commercial airlines transported approximately 5 billion passengers across 38 million flights, with both measures exceeding their 2024 levels, indicating greater aircraft utilization and corresponding inspection, repair, and maintenance workloads. Higher production demands put pressure on aerospace manufacturers to increase throughput without sacrificing quality or regulatory compliance. Robotics allows producers to mechanize other time-consuming processes, like structural assembly, surface treatment, inspection and materials handling. At maintenance bases, robotic systems assist with cleaning, inspection, repair and component-handling operations, among others, and at the same time reduce aircraft ground time. They also increase the safety of workers, by working in confined spaces or at height, or in hazardous conditions. As the size of aircraft fleets grows and the frequency of required maintenance increases, aerospace players are turning to robotics in ever-increasing numbers to boost efficiency and deliver reliable service.

Report Segmentation

The market is primarily segmented based on component, solution, payload, application, and region.

|

|

|

|

|

|

|

|

|

|

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Segmental Analysis

Component Analysis

Over the projection period, the end effector is anticipated to grow at the fastest CAGR of 12.9% during the forecast period. End effectors are mechanical and electrical devices attached to a robot's wrist. An aeronautical robot's end effectors are grippers, welding torches, force-torque sensors, material removal tools, collision sensors, and tool changers. Because it has a variety of gripping techniques and styles, the gripper is the most often utilized end effector in aerospace robots.

Source: Polaris Market Research Analysis

Solution Analysis

The traditional robot segment dominated the market with 72.0% share in 2025 due to the reliability and precision in repetitive and high-stakes manufacturing tasks. These robots are used in applications such as fastening, welding, drilling, and painting, which is essential in aircraft assembly. Their integration into the existing production units offer a low level of risk and a clear ROI as compared to the other technologies. Moreover, the developed supplier base and operator familiarity reduce the need for new training. These advances boost the demand for traditional robots.

Technological Advancements in Aerospace Robotics

| Technology | Role in Aerospace Robotics | Key Benefits |

| AI-Powered Robotics | Uses artificial intelligence for adaptive decision-making, predictive maintenance, and process optimization | Improves automation accuracy, efficiency, and operational intelligence |

| Collaborative Robots (Cobots) | Enables robots to safely work alongside human operators in assembly and inspection tasks | Enhances productivity, flexibility, and workplace safety |

| Internet of Things (IoT) | Connects robotic systems, sensors, and equipment for real-time monitoring and communication | Supports predictive maintenance and operational transparency |

| Cloud Analytics | Processes large volumes of operational and production data through cloud-based platforms | Enables data-driven decision-making and remote system management |

| Machine Vision Systems | Uses cameras and image-processing technologies for inspection, navigation, and defect detection | Increases precision, quality control, and inspection efficiency |

| Autonomous Drones | Performs aerial inspection, surveillance, and maintenance operations in aerospace facilities | Reduces inspection time, labor costs, and safety risks |

| Digital Twin Integration | Creates virtual replicas of robotic systems and aerospace components for simulation and monitoring | Enhances predictive analysis, design optimization, and maintenance planning |

| Robotic Additive Manufacturing | Utilizes robotic systems for automated 3D printing of aerospace components | Reduces material waste, shortens production cycles, and supports lightweight designs |

Source: Polaris Market Research Analysis

Regional Analysis

North America Aerospace Robotics Market Assessment

North America accounted for the largest regional share of 36.0% in 2025. The U.S. has greatly boosted its spending on updating its aircraft production units in recent years. Furthermore, significant manufacturers are driving market expansion in the U.S.

For instance, in October 2021, Reliable Robotics has raised USD 100 million in funding to automate traditional fixed-wing planes to transport freight and eventually passengers and has acquired $100 million in funding. Moreover, the government will invest in sophisticated technology robots to cater to the growing aerospace industry.

Asia Pacific Aerospace Robotics Market Insights

Asia Pacific is expected to witness fastest growth at a CAGR of 14.0% during the forecast period due to China, Japan, and India which are likely to expand robotic system purchases in the Asia Pacific area and engage in aerospace manufacturing research and development. Furthermore, many countries have invested in automated technologies to improve their manufacturing capacities and speed up the manufacturing process.

To improve the productivity of their facilities, Chinese and Indian companies are adopting service robotic technologies from Western nations. On the other hand, many aerospace robotics producers are based in the Asia Pacific.

The formation of governmental and private market robotics initiatives has boosted the demand for robots in regions like North America, Europe, and China. In comparison, the IoT has played a significant impact on developing the robotics industry in Europe and the United States. The global demand for aerospace robotics has risen steadily over the years and continues to do so.

Source: Polaris Market Research Analysis

Competitive Insights

The competitive landscape features vendor strategies focused on boosting capabilities in AI and collaborative systems. The competitive intelligence and strategy indicate that key players are positioning themselves to make targeted investment decisions to develop robotic systems to conduct complex assembly tasks. Addressing latent demand and opportunities in the commercial and defense segments. The main disruption and trend in the industry is flexible automation as a way to combat supply chain challenges. Expert's insight now suggests that vendor assessments prioritize agility and resilience over focus on precision. Moreover, the growth projection is strong due to the increased aircraft production rates, though factors such as economic and geopolitical changes remain part of the consideration.

- Kuka AG

- ABB Group

- Fanuc Corporation

- Yaskawa Electric

- Kawasaki Heavy Industries

- Mtorres

- Oliver Crispin Robotics

- Gudel Ag

- Electroimpact Inc.

- Universal Robots A/S

- Swisslog Ag

- Reis Robotics

- Boston Dynamics

- Bosch Rexroth

Industry Developments:

April 2026: ARC Aerospace and Defense Systems, LLC, partnered with SiMa.ai. The deal was signed to support ARC’s domestic production of next-generation flight computers. Their focus is on autonomous systems and low-cost counter-drone missiles. (Source: sima.ai)

December 2025: Saab and Divergent Technologies revealed a landmark 3D-printed aircraft fuselage section assembled using advanced AI-powered robotic systems. The collaboration delivered what was described as the world’s first software-defined aircraft fuselage, produced without dedicated tooling and using a minimal quantity of printed metal components to maintain structural strength. This innovation marked a significant leap in flexible aerospace manufacturing, with the potential to lower production costs and accelerate design cycles for next-generation airframes. The partners confirmed that the digitally engineered and robotically assembled structure was planned to undergo its first test flight the following year. (Source: saab.com)

March 2025: Drone Forge announced a strategic partnership with Airbus to jointly deploy and integrate the Flexrotor uncrewed aerial system. Formalized through a Letter of Intent, the agreement centered on leveraging the tactical vertical takeoff and landing drone for intelligence, surveillance, and reconnaissance missions across the Asia-Pacific region. The collaboration aimed to commercialize the robotic platform for defense, government, and commercial uses, capitalizing on its autonomous operation in challenging and GPS-denied environments. This partnership marked a key milestone in expanding the reach and capabilities of autonomous aerospace robotics. (Source: airbus.com)

Aerospace Robotics Market Report Scope

| Report Attributes | Details |

| Market size value in 2025 | USD 4.36 Billion |

| Market size value in 2026 | USD 4.86 Billion |

| Revenue forecast in 2034 | USD 11.80 Billion |

| CAGR | 11.7% from 2026 - 2034 |

| Base year | 2025 |

| Historical data | 2021 - 2024 |

| Forecast period | 2026 - 2034 |

| Quantitative units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Segments covered | By Component, By Payload, By Solution, By Application, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies | Kuka AG, ABB Group, Fanuc Corporation, Yaskawa Electric, Kawasaki Heavy Industries, Mtorres, Oliver Crispin Robotics, Gudel Ag, Electroimpact Inc., Universal Robots A/S, Swisslog Ag, Reis Robotics, Boston Dynamics, and Bosch Rexroth. |

Source: Polaris Market Research Analysis

aerospace robotics market FAQ's

• The global market size was valued at USD 4.36 billion in 2025 and is projected to grow to USD 11.80 billion by 2034.

• The global market is projected to register a CAGR of 11.7% during the forecast period.

• North America accounted for the largest regional share of 36.0% in 2025.

• A few market players are Kuka AG, ABB Group, Fanuc Corporation, Yaskawa Electric, Kawasaki Heavy Industries, Mtorres, Oliver Crispin Robotics, Gudel Ag, Electroimpact Inc., Universal Robots A/S, Swisslog Ag, Reis Robotics, Boston Dynamics, and Bosch Rexroth.

• The traditional robot segment dominated the market with 72.0% in 2025. This is due to the increased use of traditional robots in applications such as fastening, welding, drilling, and painting.

• The end effector is expected to witness rapid growth at a CAGR of 12.9% during the forecast period.

Download Sample Report of aerospace robotics market

Please fill out the form to request a customized copy of the research report.