3D Printing Metals Market Size, Share, Trends, Industry Analysis Report: By Form Type (Filament, Powder, and Others), Product, Technology, End User, and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) – Market Forecast, 2025–2034

- Published Date:Jan-2025

- Pages: 119

- Format: PDF

- Report ID: PM1153

- Base Year: 2024

- Historical Data: 2020-2023

3D Printing Metals Market

Metal 3D printing is a manufacturing technique that enables the creation of complex geometries and parts that are difficult or impossible to manufacture using traditional methods. The process entails spreading a thin layer of metal powder over a build platform before scanning the cross-section of the part with a laser to melt the powder into the next layer. Metal 3D printing is popular as it enables the creation of parts that are stronger, lighter, and more complex than those produced using traditional methods. It has the potential to shorten lead times and reduce material waste.

To Understand More About this Research: Request a Free Sample Report

A variety of metals, including titanium, stainless steel, and aluminum, are used to manufacture products using 3D printing. Metals are commonly used in 3D printing for products that need high strength, stability, chemical resistance, and heat resistance. They are used to create prototypes, spare parts, and functional parts for a variety of industries, including aerospace, automobile, defense, medical, and industrial applications. Topology optimization software can optimize the product's initial design by defining load and stiffness constraints, resulting in reduced weight and improved performance.

Titanium is in high demand in the 3D printing market. It is one of the most durable and lightweight metals used in aerospace, defense, dental, and medical applications. Titanium's properties include non-toxicity, high strength, and corrosion resistance. It is used in the aerospace industry for printing airframe and wing structures, compressor blades, and turbine engines due to its high strength-to-weight ratio and high temperature resistance. Stereo lithography (SLA) is becoming widely used in 3D printing. SLA uses an ultraviolet (UV) laser to cure liquid photopolymer resin layer by layer.

3D Printing Metals Market Dynamics

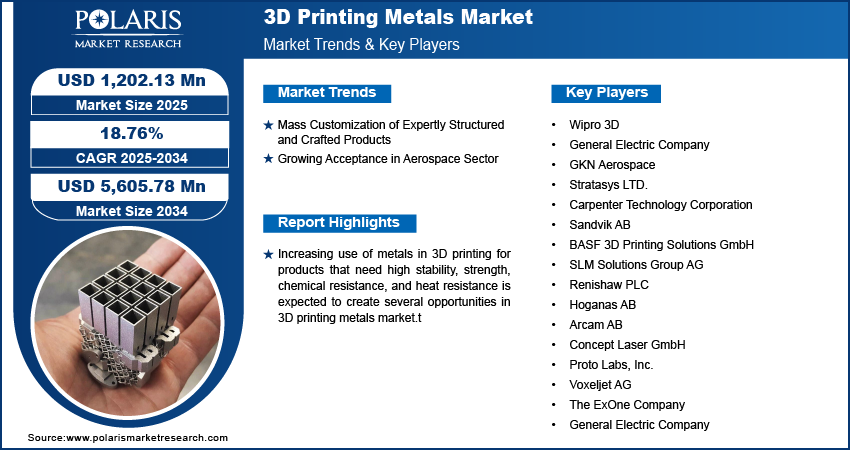

Mass Customization of Expertly Structured and Crafted Products

Customers can now design and develop new paradigms by creating their imaginative designs on a computer and printing them using a printer due to 3D printing, which has simplified the manufacturing process. Mass customization enables customers to have individualized products that are catered to their unique preferences by fusing the ideas of manufacturing and personalization. For instance, in the production of key components for engine parts, turbine blades, and intricate bio-implants, metal 3D printing is used to produce such intricate geometrical components with great performance. Through mass customization, the 3D printing metal technique helps create lightweight, customized products at a low cost. Thus, mass customization of expertly structured and crafted products is boosting the 3D printing metals market growth.

Growing Acceptance in Aerospace Sector

3D printing metals technique is being used in the aerospace sector to create parts with complex geometries that would be hard or impossible to make with conventional techniques. The technique has a number of benefits over conventional manufacturing techniques, especially when it comes to creating intricate and lightweight parts. This includes jet engine components that must be able to tolerate high temperatures and pressures, like fuel nozzles and turbine blades. Therefore, the growing acceptance of 3D printing metals in the aerospace industry is driving the 3D printing metals market demand.

3D Printing Metals Market Segment Insights

3D Printing Metals Market Outlook by Form Type

Based on form type, the 3D printing metals market is segmented into filament, powder, and others. The powder segment dominated the market with the largest revenue share of 96.2% in 2024. There are several key characteristics of metal powder particles that influence the additive build process and the final component's characteristics such as particle size, shape, concentration, and flowability. This includes the raw material's physical and chemical characteristics, which need to be accurately understood and described. These factors are expected to increase the demand for metal powder in the coming years.

3D Printing Metals Market Assessment by End User

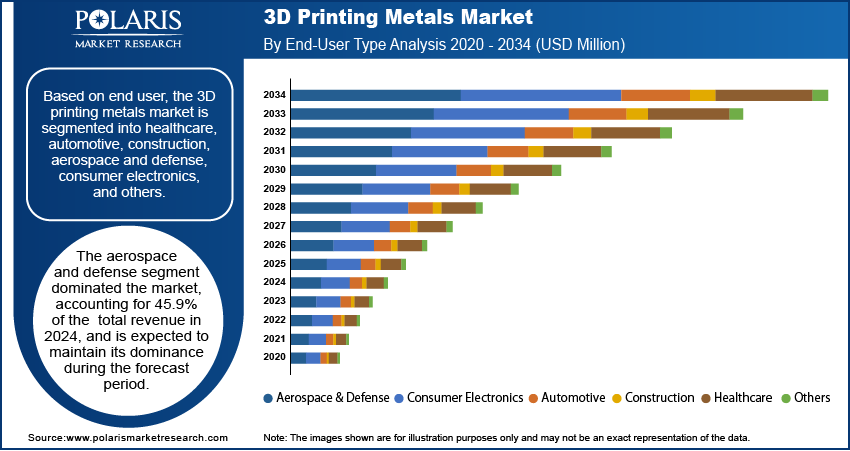

Depending on end user, the 3D printing metals market is segmented into healthcare, automotive, construction, aerospace & defense, consumer electronics, and others. With the largest revenue share of 45.9% in 2024, the aerospace & defense segment dominated the market. Most of the industry participants anticipate that their use of 3D printing will at least double over the next few years, demonstrating the revolutionary impact of 3D printing in the aerospace and defense sector. With more than half of respondents admitting that 3D printing has altered the operational landscape of the industry, this trend has resulted in a fundamental change in how the sector functions.

3D Printing Metals Market Regional Insights

The study offers regional insight into the 3D printing metals market in North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

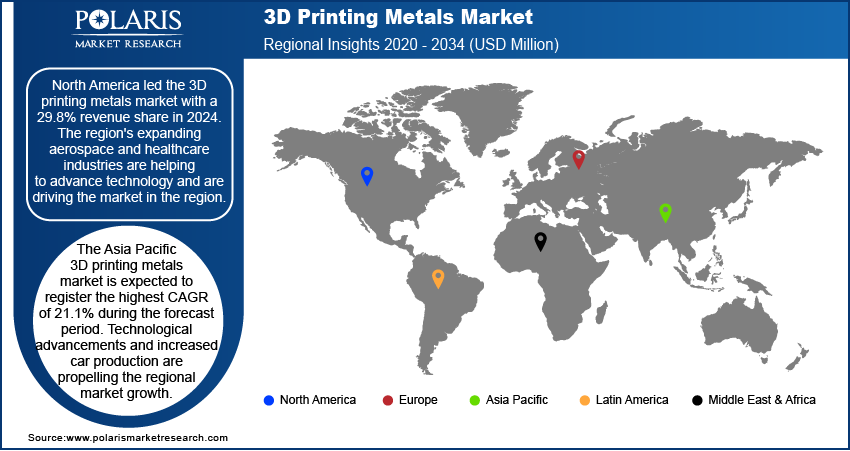

North America led the 3D printing metals market with a 29.8% revenue share in 2024. The region's expanding aerospace and healthcare industries are helping to advance technology. Large automotive factories, rising aerospace and defense investments, and infrastructure advancements are driving the region's need for metal-based 3D printed parts. Furthermore, the use of 3D printing metals has demonstrated considerable growth potential in the North American healthcare and automotive sectors. Due to the large number of manufacturers and end users in the US, the country is expected to hold the largest share of the North America 3D printing metal market revenue in 2024.

The Asia Pacific 3D printing metals market is anticipated to register the highest CAGR of 21.1% during the forecast period. It is anticipated that the increasing use of additive manufacturing by aerospace companies will propel market expansion. Technology breakthroughs and rising car production are driving 3D printing metals market development in the region.

3D Printing Metals Market – Key Players and Competitive Insights

The 3D printing metals market is expected to grow in the coming years as large companies are investing heavily in research and development to increase the range of products they offer. Rivals in the 3D printing metals industry need to offer reasonably priced goods to expand and prosper in a market that is getting more competitive. New and innovative product launches, mergers and acquisitions, contracts, collaboration with other organizations, and higher investments are a few examples of significant market developments. To increase their worldwide reach, market players are also putting a number of initiatives into action strategically. One of the basic business tactics used by manufacturers in the global 3D printing metals industry to benefit customers and grow the market sector is local manufacturing to minimize operating costs. To expand their product lines, the important players in the market are spending a ton of money on research and development.

Wipro 3D; GKN Aerospace; Stratasys LTD.; Carpenter Technology Corporation; Sandvik AB; BASF 3D Printing Solutions GmbH; SLM Solutions Group AG; Renishaw PLC; Hoganas AB; Arcam AB; Concept Laser GmbH; Proto Labs, Inc.; Voxeljet AG; The ExOne Company; and General Electric Company are among the top companies in the 3D printing metals market.

List of Key Players in 3D Printing Metals Market

- Wipro 3D

- General Electric Company

- GKN Aerospace

- Stratasys LTD.

- Carpenter Technology Corporation

- Sandvik AB

- BASF 3D Printing Solutions GmbH

- SLM Solutions Group AG

- Renishaw PLC

- Hoganas AB

- Arcam AB

- Concept Laser GmbH

- Proto Labs, Inc.

- Voxeljet AG

- The ExOne Company

3D Printing Metals Industry Developments

In July 2024, 3D Systems and Precision Resource established a strategic alliance with the goal of advancing metal additive manufacturing and accelerating its use in high-criticality markets.

In November 2023, Materialise and Nikon SLM Solutions announced that they were working together to develop Materialise Build Processors for Nikon SLM Solutions printers. These specifically built Build Processors will be completely integrated into the platform Materialise CO-AM.

3D Printing Metals Market Segmentation

- Powder

- Filament

- Others

By Product Outlook

- Titanium

- Aluminum

- Stainless Steel

- Nickel

- Others

By Technology Outlook

- Directed Energy Deposition

- Sheet Lamination

- Binder Jetting

- Powder Bed Fusion

- Metal Extrusion

- Others

By End User Outlook

- Aerospace & Defense

- Consumer Electronics

- Automotive

- Construction

- Healthcare

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of the Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

3D Printing Metals Market Report Scope

|

Details |

|

|

Market Size Value in 2024 |

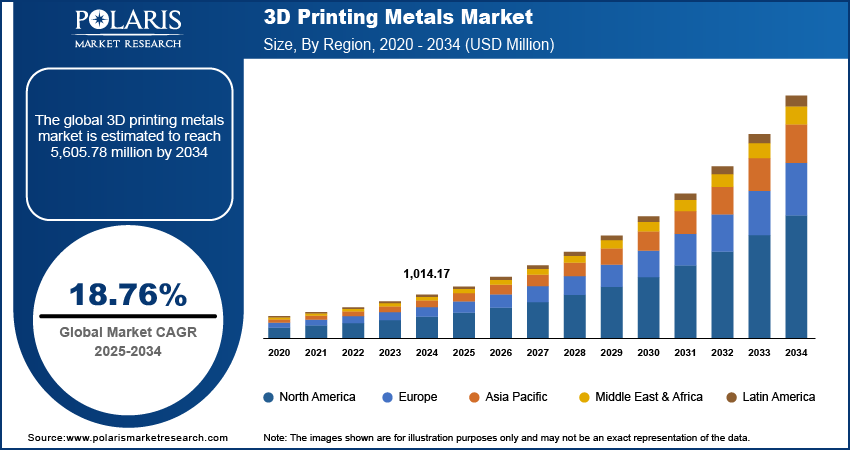

USD 1,014.17 million |

|

Market Size Value in 2025 |

USD 1,202.13 million |

|

Revenue Forecast by 2034 |

USD 5,605.78 million |

|

CAGR |

18.76% from 2025 to 2034 |

|

Base Year |

2024 |

|

Historical Data |

2020–2023 |

|

Forecast Period |

2025–2034 |

|

Quantitative Units |

Revenue in USD and CAGR from 2025 to 2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

|

|

Report Format |

|

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The 3D printing metal market size is expected to grow from USD 1,202.13 million in 2025 to USD 5,605.78 million by 2034.

The market is expected to register a CAGR of 18.76% during the forecast period.

North America held the largest market share in 2024.

Proto Labs, Inc.; Voxeljet AG; The ExOne Company; General Electric Company; GKN Aerospace; Stratasys LTD.; Carpenter Technology Corporation; Sandvik AB; and BASF 3D Printing Solutions GmbH are a few of the key players present in the 3D printing metals market.

The powder segment dominated the market with 96.2% of the total revenue share in 2024.

The aerospace and defense segment dominated the market with the largest revenue share of 45.9% in 2024.

© 2025 Polaris Market Research and Consulting. All rights reserved